Swan Private Insight Update #30

This report was originally sent to Swan Private clients on December 8th, 2023. Swan Private guides corporations and high net worth individuals globally toward building generational wealth with Bitcoin.

This report was originally sent to Swan Private clients on December 8th, 2023. Swan Private guides corporations and high net worth individuals globally toward building generational wealth with Bitcoin.

It is well known to Bitcoiners and any student of monetary history that precious metals like gold and silver were once the base layer of the monetary system and that this is no longer the case. Bitcoiners and the school of Austrian Economics have offered explanations as to why monetary history played out this way for gold and silver — namely, that settling trade in precious metals is slow, expensive, and complicated. In other words, precious metals severely lack portability.

In this article, we’ll explore the long, multi-step process that gold went through, leading to its eventual removal as the base layer of the monetary system. And we’ll evaluate whether Bitcoin is subject to those same threats.

The reason why this topic is so important is that many people hold that the ultimate goal of Bitcoin is not just to become what gold is today, i.e., a store of value financial asset, but to be a neutral base layer of a new monetary system which allows billions of users worldwide to hold & transact in a trust-minimized manner that is not reliant on custodians, central banks, or governments.

Can Bitcoin achieve this lofty goal? Will it ultimately meet gold’s fate? Or is some other in-between outcome more likely?

It’s generally accepted that usage of Bitcoin on-chain can only scale so much without risking the fundamental principles that keep it decentralized. Even if Bitcoin’s block size were to be increased in the future, it wouldn’t be able to increase to the point where billions of users are able to transact on the base layer for everyday transactions while also keeping mining and auditing (node-running) sufficiently decentralized.

Therefore, the current view is that transaction fees on the base chain will soon price out many transactions (e.g., the fee to transact may be larger than the desired transaction value). Additional layers on top of Bitcoin are therefore required for more users to hold and transact Bitcoin.

The most well-known piece of this scaling strategy is the Lightning Network. However, it’s generally understood that even Bitcoin + Lightning does not get us to a place where billions of users are able to use Bitcoin for everyday transactions.

There are a few recent articles which provide excellent context for this discussion:

Thoughts on scaling and consensus changes (2023) — JamesOb

Scaling considerations including an honest take on why one might be skeptical about scaling in layers.

Putting the B (for Billions) in BTC — Anthony Towns

A look at all the possible ways that blockchains can theoretically scale and a deeper look at the Bitcoin scaling strategies currently being discussed and built.

Banks Without Bankers — Eric Yakes, Axiom

An in-depth look at scaling strategies, including Fedimint, Cashu, Bitcoin Free banks, and Ark.

Lightning Is Doomed — Shinobi, Bitcoin Magazine

A reality check on the limitations of Lightning Network and what that means in terms of its long-term viability. No, it’s not doomed, but it probably won’t be used the way you expected it to be.

In one of the articles listed above, the author (Shinobi) points this out from the Lightning white paper:

This is where other solutions come into play, such as federated chaumian mints, sidechains, Ark, and future soft-fork-enabled covenants. And yes, some people will keep their Bitcoin in third-party custody.

Additionally, Peter McCormack, host of the What Bitcoin Did podcast, sent out a relevant (and timely) tweet as we were writing this article.

The following quote is from one of the above articles, and hopefully, it gives a sense of why there is some trepidation about scaling in layers:

When reading a draft of this post, my wife got kind of depressed right around here. Her macabre question, basically, is: “If everyone just winds up interacting with sidechains and not Real Bitcoin, hasn’t the whole thing failed? At every point, you’re dealing with some token that isn’t really Bitcoin.”

And it begs this further question: if, at every point, most people are dealing with some token that isn’t really Bitcoin, will Bitcoin eventually succumb to what gold did? (i.e., capture by governments and banks and eventual removal as the base layer of the monetary system.) Bitcoin’s on-chain monetary properties are better than gold’s, but is that enough to prevent it from failing as gold did?

What if you add in the benefits of Lightning and additional scaling strategies?

Now let’s take a look at an extremely condensed summary of monetary history.

In a world where everyone conducts commerce by directly exchanging physical precious metals, the services provided by banks would not provide much value, and therefore banks would not hold nor transfer much of society’s monetary wealth. Therefore, if a government wants to capture and manipulate the monetary system as a whole, direct physical theft on a grand scale is required.

As an economic system evolves and more trade occurs, market participants find it advantageous to keep precious metals with custodians who can reliably protect them. And further, if you can use your receipt for custodied gold instead of actually settling trade by directly exchanging precious metal, the convenience is greatly improved. Gold’s lack of portability results in these undeniable benefits of centralized custody. However, this is also the first step in gold’s downfall.

Centralized custody results in a situation where one entity holds the gold for many customers, and eventually, the custodian realizes that they have the opportunity to “do something” with a large portion of the deposited assets, such as making loans and charging interest.

The idea here is that the custodian can successfully earn extra money as long as not all customers want to access their assets at the same time. This is known as fractional reserve banking. (Maybe the custodian is transparent with its depositors about how they are handling the deposited funds; maybe they aren’t. Maybe the custodian shares some of the interest with its depositors; maybe they don’t. These are interesting topics to explore, but they are not the focus of this piece.) The point here is that fractional reserve banking is the second step in gold’s downfall, and it’s only possible after centralized custody.

Bitcoiners and Austrian economists believe that fractional reserve banking is an inherently unstable system, prone to booms and busts, which makes sense given that the system quite literally is designed to expand the money supply through lending and contract the money supply when loans are paid back or defaulted on. This monetary expansion and contraction distorts price signals, which confuses market participants into believing there is more demand for their products/services than there truly is in reality. This produces the illusion of an economic boom, but it is eventually uncovered as being not based in reality, and this uncovering process eventually turns into a bust.

When the bust (and the associated societal pain of a bust) becomes apparent, politicians often step in to provide a “solution.”

If the politicians are unable to identify fractional reserve banking as the root cause for the boom/bust cycle, or if they are being persuaded by the banking industry that fractional reserve banking must continue to go on, their solution will leave fractional reserve banking as it is. Instead, they might introduce a system such as “central banking.” It might even be driven by fairly benign motivations to start, such as “Look, we’ve seen many financial crises causing banks to collapse and citizens to lose their life savings. We’ll introduce a central bank that can be the lender of last resort to prevent a bank from collapsing. This will prevent future financial crises.”

In reality, the central bank ends up perpetuating and exacerbating the fractional reserve game. It intervenes so that busts are not allowed to occur because busts would cause the fractional reserve “broad money” to default and disappear, leading the money supply to collapse down toward the base money. Or, as Allen Farrington succinctly put it:

Instead of allowing this natural process to take place — of broad money collapsing down to base money — the boom/bust cycle continues on forever, with the booms getting bigger and the busts getting bigger. Eventually, the broad money grows to the extent that it becomes apparent that it’s impossible for all of the broad money to be convertible back into the base money. Historically, this meant that it became apparent that there were too many paper dollars circulating vs real ounces of gold or silver, even though the dollar was clearly defined as being convertible into a specific amount of gold or silver.

The inevitable result of this is a government “solution” that involves the removal of precious metals as the base layer of the monetary system. The dollar becomes a unit without its base layer anchor. You officially enter the fiat era. It just took one surprise televised announcement by President Nixon to say the dollar was “temporarily” no longer redeemable for gold to snuff out the final illusion that gold was the base money supporting the dollar and the world’s economy.

Looking at the rough historical timeline in the United States, fractional reserve banking was happening through the 1800s, then central banking began in 1913, and gold was removed as the base layer in 1971. To summarize, gold’s removal as the monetary base layer happened gradually, except for the very last step, which was very sudden. At its root, though, the costs of moving (portability) and securing (custody) gold were its vulnerabilities that eventually led to few entities personally moving or securing gold.

A critical question you can always ask yourself as you think about the root causes for how our monetary system evolved is as follows: If precious metals could have been held/sent/verified easily & cheaply, how many market participants would have said, “I don’t want the gold or silver; give me government-authorized fractional reserve bank credit money instead.”?

There is an argument to be made that even just the combination of on-chain Bitcoin + third-party custodians has a better shot at preventing capture than gold + third-party custodians. I think it’s best to demonstrate this in the form of a scenario and a question:

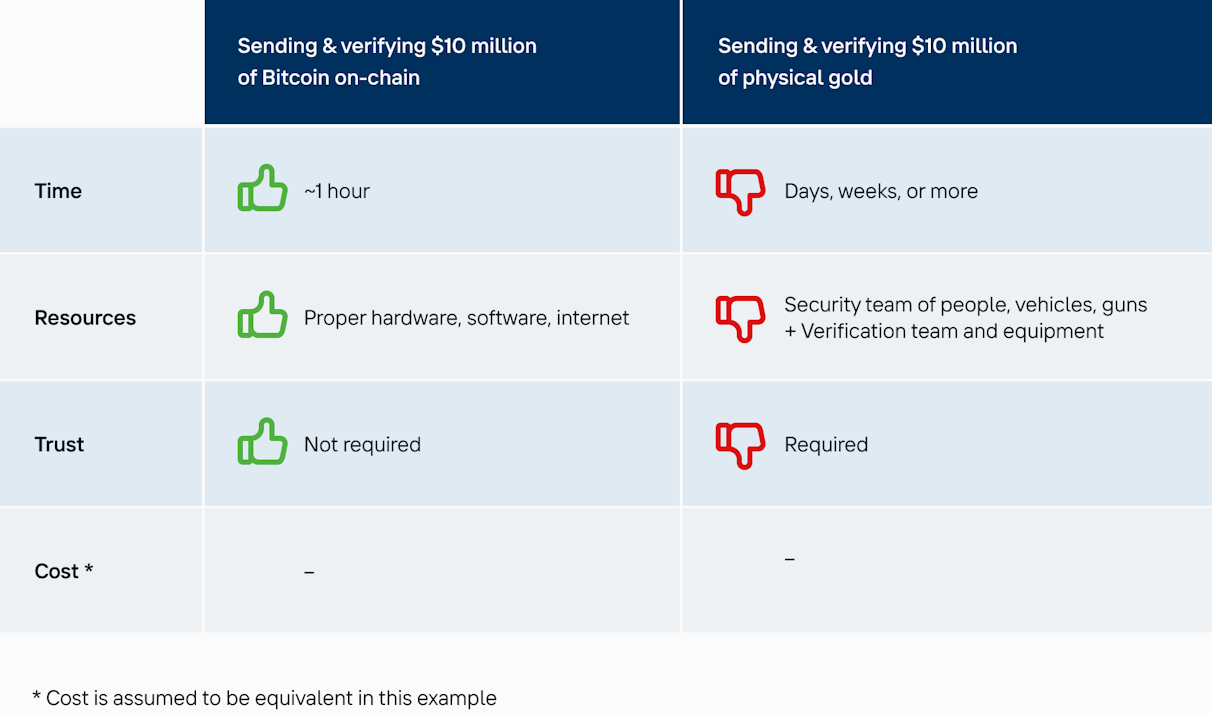

You have to send a payment of $10 million in today’s dollars to a person in another country. Assume the cost to complete the transaction is $50k either by doing an on-chain Bitcoin transactions or by sending physical gold. Which do you choose?

Even though we assumed that the monetary cost was exactly the same, the on-chain Bitcoin transaction is more attractive than gold because sending physical gold involves far more time, effort, trust, and resources. To send the gold, you need a trustworthy security team, and you need to wait days or weeks for the transaction to complete. Even verifying that the transaction was completed is no easy task.

Alternatively, to send the Bitcoin, you need the proper hardware, the proper software, an internet connection, and about one hour of time for the final settlement of the transaction, with no doubt verifying that it was indeed completed. Bitcoin is clearly the better choice in terms of time, effort, trust, and resources.

The takeaway here is that this advantage of on-chain Bitcoin makes it a gigantic improvement over a gold-based monetary system, even if Bitcoin on-chain transactions become far more expensive than the few dollars they cost today, and we don’t implement any other scaling solutions.

Put another way, a person who owned a lot of gold in the late 1800s was still highly incentivized to keep their gold stored with a custodian in a bank vault. Simply having a lot of gold does not make you immune to the fact that you need a team of people, armored vehicles, and a lot of time in order to move a significant amount from one place to another. The same is not true for someone who owns a lot of Bitcoin. Taking self-custody and sending Bitcoin on-chain is fairly easy and achievable as long as you aren’t priced out by the on-chain fees. Again, this represents a huge improvement vs the limitations and frictions of gold.

Without getting into the nitty-gritty of how the Lightning Network functions, you can think of it as the settlement network, which will be one day be used by federated chaumian mints or Bitcoin banks, especially when on-chain fees are significantly higher than they are today. One could argue that if we’re depending on a settlement network between mints and banks, have we actually created anything better than the existing fiat banking system?

Aren’t we just trusting the mints and banks not to rug-pull us again?

There are two critical differences to highlight here:

Becoming one of these mints or banks will not be a process that is gate-kept by the government and banking regulators.

If there is a discrepancy between participants in this settlement network, they have the ability to go to the base chain for adjudication without requiring significant time, effort, trust, and resources.

Neither of the above two things can be said about the banking industry historically or today. Elaborating on these two points is worthy of a future article of its own. But for now, hopefully, it’s clear that these two points hold true for Bitcoin + Lightning but do not hold true for the legacy system.

As mentioned earlier, scaling solutions such as federated chaumian mints become important when you realize that, in a future high on-chain fee environment, Bitcoin on-chain + Lightning is not sufficient to provide billions of users the ability to each hold & transact Bitcoin directly.

To be clear, each of the scaling strategies mentioned in this section’s header are quite different from one another. And it’s worth noting that covenants appear to be the best chance at providing as many users as possible to have a nearly self-sovereign experience with Bitcoin. There is significant debate in the Bitcoin community about how and when to enhance covenants on Bitcoin.

See this discussion between Stephan Livera and Brandon Black for an in-depth discussion on covenants:

It would take several more pages to describe each of these scaling strategies. Instead we’ll focus on federated chaumian mints and the benefits they offer the Bitcoin system as a whole. A mint would accept Bitcoin deposits from its users and, in exchange, give them Bitcoin-denominated eCash tokens in an eCash wallet. Deposits and withdrawals to the eCash wallet would be made using the Lightning Network. If users in the same mint are paying one another, funds stay within the mint, they can be moved at a very low cost, and there is no need to involve Lightning. If they pay someone outside the mint, the Lightning Network would be used to settle balances between mints.

If they pay someone outside the mint, the Lightning Network would be used to settle balances between mints.

Mints can be designed in such a way that the mint does not know the identity, account balances, or transaction histories of each eCash wallet. Similar to point (1) raised above for the Lightning Network, there will not be a massive barrier to entry if one wants to become such a mint who provides these services to their community. Yes, there is some barrier to entry, including the time and capital it takes to operate the mint. However, this would be far smaller than the time, capital, and regulatory blessings needed to launch and operate a bank in the legacy system.

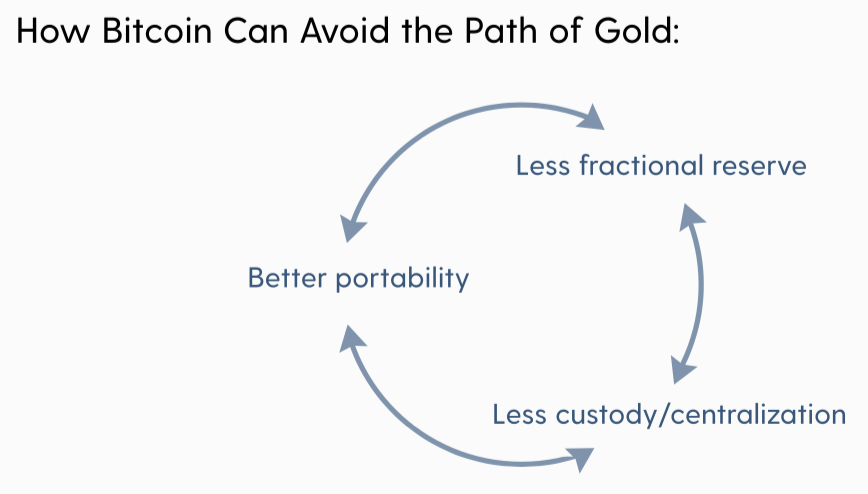

Although this stacked system of on-chain, Lightning, and layer three solutions may look like it shares the same concerns as precious metals — that of people surrendering custody of the base layer asset — there is actually a huge difference. That difference is that at each layer, Bitcoin supports way more participants (i.e., competitors) than gold could. Already today, millions of people self-custody Bitcoin, and that number continues to grow with pretty much each block added.

And Lightning, too, can add millions of native users a year. Yet, Lightning plus on-chain Bitcoin already provides all the functionality of fully integrated, highly secure, interconnected banks. If there are millions of bank equivalents, able to interoperate without the portability and security constraints of gold, and customers of those “banks” can easily choose several of these and switch between them, we have overcome the centralizing forces that gold’s portability constraints led to and, thus, avoided gold’s fate.

If the current approach to scaling Bitcoin in layers is carried out, will it afford all users full self-sovereignty with no need to trust any third party and no risk of ever being rugged? No. Does it, however, offer a path for users to interact with Bitcoin in a trust-minimized manner while keeping the system as a whole decentralized and not resistant prone to capture? I think yes.

Even if no more scaling solutions are added, Bitcoin can remain far more decentralized and “uncapturable” than gold ever was or can be. This is simply because both securing and sending Bitcoin involves significantly less time, effort, trust, and resources.

Think about it this way: Even if only 1 million entities can use Bitcoin and everybody else has to rely on this million to provide the scale of transactions they need, that’s still profoundly more competition and choice than is needed to keep those million providers mostly honest. At 7 billion people in the world (and throw in another billion to serve all the corporations), each on-chain entity would only need to serve 8,000 customers — and that’s an easy scale to achieve. So it’s likely that each person would be able to spread their business around many such providers and not risk a total loss if one of them were to become insolvent or fail in some other way.

It may not be perfect, and I’m not calling for complacency or that we halt the pursuit of scaling solutions, but even the current status quo already doesn’t result in a collapse of Bitcoin and replacement of it with some vastly inferior substitute as happened with gold.

Bitcoin’s solution to gold’s two biggest vulnerabilities is already sufficient to prevent it from suffering the same fate gold did. And the scaling solutions being discussed and built today are cause for even more optimism that Bitcoin can achieve its ultimate goal — to be a neutral base layer of a new monetary system which allows billions of users worldwide to hold & transact in a trust-minimized manner not reliant on custodians, central banks, or governments.

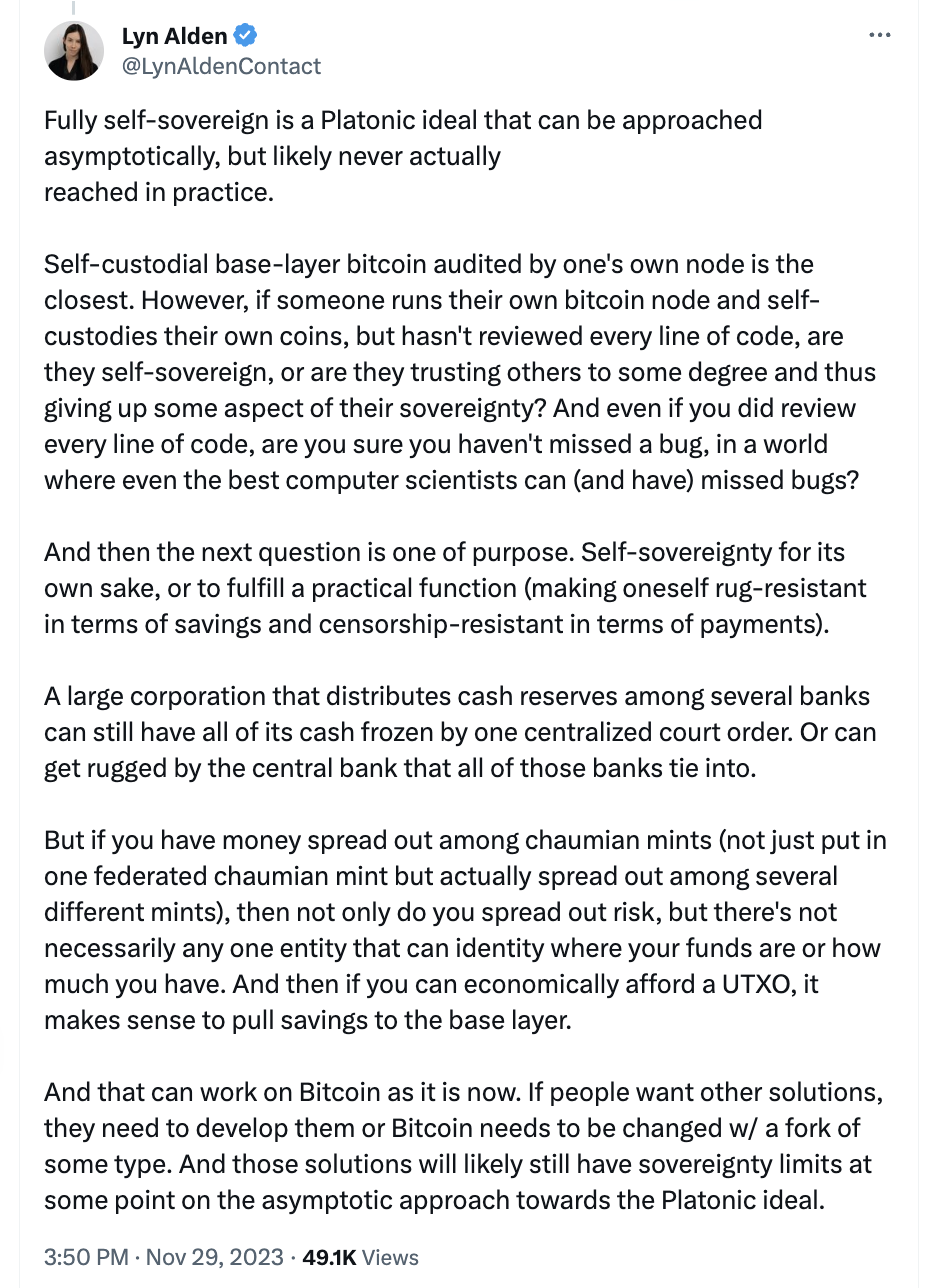

A final resource for readers to explore is this particular tweet from Lyn Alden in the thread started by Peter McCormack. I would encourage readers to check out that thread in its entirety. But this particular tweet does a great job summarizing several of the ideas discussed in this article.

Hold your IRA with the most trusted name in Bitcoin.

John is the Managing Director of Private Client Services at Swan Bitcoin. He previously spent 13 years on Wall Street, where he was a Portfolio Manager and Insitutional Investor at Goldman Sachs.

If you’d like to learn more about the Bitcoin network and protocol function, you can download Inventing Bitcoin by Yan Pritzker for FREE!

Thoughts on Bitcoin from the Swan team and friends.

After the Coldcard exploit, everyone is asking the same question: is my Bitcoin custody setup safe? Swan’s CTO opens up the hardware behind Swan Vault and answers it.

Some Coldcard hardware wallets were compromised due to false randomess. Learn which type of Coldcard users were affected and what custody alternatives exist.

A 50-day campaign to advance freedom and sovereignty through Bitcoin adoption