The Battle for Monetary Independence

A 50-day campaign to advance freedom and sovereignty through Bitcoin adoption

This article examines the relationship between a monetary asset being a store of value vs. being a medium of exchange.

Specifically, it focuses on the scaling method of the Bitcoin network as its main example. It also takes a broad look at the history of trade-offs in the cryptocurrency space to see why a layered approach makes the most sense.

The primary goal of this article is to examine how Bitcoin has evolved as a medium of exchange and, more broadly, to analyze the order in which new monetary assets can be accepted as a store of value and a medium of exchange.

As a big part of that, I’ll include an analysis of the Lightning network, a small but fast-growing payments layer interwoven into the Bitcoin network.

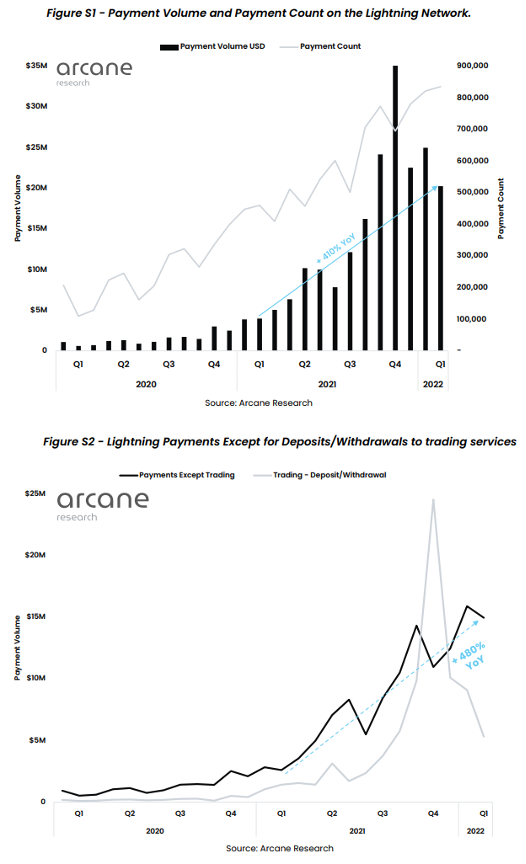

Arcane Research, The State of Lightning Volume 2

This article is long, so I’ll summarize the main points up front here, and then spend the rest of the article diving into the details.

A truly decentralized and permissionless payment network requires its own underlying self-custodial digital bearer asset. If instead it runs on top of the fiat currency system or relies on external custodial arrangements at its foundation, then it is neither decentralized nor permissionless.

In order to create a truly new digital bearer asset that is useful for payments in the long run, it must also be an attractive store of value, so that a meaningful percentage of the population begins to persistently hold it as some percentage of their liquid net worth and be willing to accept it for goods and services.

In other words, in order to create a decentralized version of Visa, beneath that you must first create a decentralized version of Fedwire, and along with that you must first create a decentralized version of digital gold. It’s hard to envision any other path succeeding.

Bitcoin started with a smart design from the beginning. It created an underlying digital gold and settlement network, with a credible degree of decentralization, auditability, scarcity, and immutability that no other network currently rivals. On top of that foundation, Lightning as a payment network is being developed, and has reached a critical mass of liquidity and usability.

Many cryptocurrencies that followed in Bitcoin’s wake put the cart before the horse. They optimized for throughput and speed on their base layer, at the cost of weaker decentralization, auditability, scarcity, and/or immutability of the underlying bearer asset. As such, they failed to gain structural adoption as money and rendered their high throughput irrelevant, especially since they were brought into exist in the shadow of Bitcoin’s larger network effect.

Volatility is inevitable along the path of monetization. A new money cannot go from zero to trillions without upward volatility by definition, and with upward volatility comes speculators, leverage, and periods of downward volatility. The first couple decades of monetization for the network as it undergoes open price discovery to reach the bulk of its total addressable market, should be different than the “steady state” of the network after it reaches the bulk of its total addressable market, assuming it is successful in doing so.

Taxes on cryptocurrency transactions, as well as the lower supply inflation rate of bitcoins compared to fiat currencies, results in Gresham’s law being applicable here. Most people in developed countries have an incentive to spend their fiat and hoard their bitcoin like an investment, at least in this stage of the monetization process. The exception is for the subset of people who specifically need Bitcoin/Lightning’s permissionless nature for one reason or another, or for whom the majority of their liquid net worth is in it.

People in developing countries, with higher inflation and weaker payment and banking systems in general, have more of a natural incentive to use Lightning as a medium of exchange earlier on its monetization process. Indeed, adoption rates are rather promising in many of those regions. This isn’t surprising, considering that more people in developing countries have smart phones than bank accounts, in aggregate.

An overview of how the Lightning network works in a basic sense, and why channel-based transaction systems make more sense than broadcast transaction systems for individual payments.

A look at other use-cases for the Lightning network, including its usage as a fast settlement system to move dollars and other fiat currencies around globally, through the core bitcoin liquidity of the network.

A response to various criticisms of the Lightning network, including an explanation of why comparing its small size to various larger DeFi projects is a category error, and an analysis of its scaling potential.

Concluding thoughts on the regulatory and enforcement hurdles governments face now that open-source peer-to-peer payments technology exists.

Humans in tiny groups don’t need money; they can organize resources among themselves manually.

However, groups that reach the Dunbar number or larger usually start identifying and using some form of money, which gives them a more liquid, divisible, friction-minimized, and widely-accepted accounting unit for storing and exchanging value with people they don’t know.

What makes good money?

And how does new money get adopted by users?

I cataloged the history of this question from multiple points of view in my article, "What is Money, Anyway?"

The short answer from thousands of years of history across multiple continents is that commodity money that is adopted organically needs to have a reasonably high stock-to-flow ratio and needs sufficient divisibility, portability, durability, fungibility, and verifiability while being desirable to hold for some reason.

When different commodity monies come in contact with each other, often due to contact between cultures with varying levels of technology, the money that is harder to produce (i.e., able to maintain a persistently higher stock-to-flow ratio even in the face of improving human technology) wins out. Money in a society generally consolidates towards one or two, rather than many of them coexisting indefinitely. Precious metals, specifically gold, won the commodity money competition over thousands of years.

Ledger-only systems, referring to paper and bank currency systems with flexible money supplies that are backed by nothing and have no cost to produce, have been tried several times in history. Each of those fiat currencies inevitably failed over a long enough timeline. The temptation by central policymakers to produce more, especially in times of crisis, is always there. To assume that such a system can last forever without a breakdown or reset of some sort is to assume that there will be an unbroken chain of competent and selfless centralized operators of that monetary system.

Buy automatically every day, week, or month, starting with as little as $10.

However, with the development of telecommunications technology and global bank ledgers, fiat currencies eventually offered an actual improvement in long-range transaction and verification speeds compared to precious metals, which along with the taxation or sometimes outright banning of precious metals and other monies, is part of what lead to their widespread adoption for the first time in history.

Precious metals as bearer assets were not divisible or portable enough to keep up with global commerce at the speed of telecommunications channels. They thus had to be abstracted with pegs, claims, and counterparty risk. Due to this speed mismatch and subsequent abstraction, policymakers dropped precious metals away from the process altogether, other than keeping them as opaque sovereign reserves. They created a ledger-only system around the world that is currently in its sixth decade of operation.

The dollar has a lower stock-to-flow ratio than gold but does have a higher average stock-to-flow ratio than most other commodities and has the property that it can be sent around the world relatively quickly, while most of its scarcer competition (e.g., gold) is both slow and taxed. The dollar is not something you particularly want to store value in for decades. Still, it clearly has its use cases in terms of payments and near-term savings due to how the global financial system has been engineered.

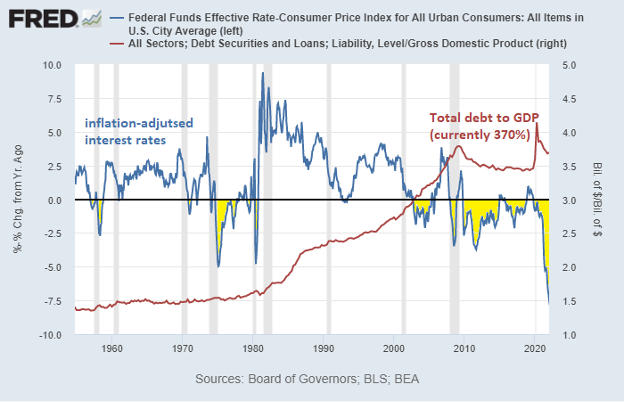

I do, however, think that this fiat system that has been in place since the 1970s is becoming more unstable and will end up undergoing longer-run devaluation and realignment to clear excess debt out of the system. That process has already been in place for over a decade in the U.S., and I expect it to continue both here and elsewhere in the world:

St. Louis Fed

And when we look globally, there are dozens of countries with current or recent inflation rates over 25% and/or that have had currency resets or hyperinflations within our lifetimes.

The Bitcoin network introduces faster payment and settlement speeds than fiat currencies. Still, its units also have a higher stock-to-flow ratio than gold. They can be used as self-custodial and peer-to-peer through the decentralized network.

However, it’s new and volatile, poorly understood, and certainly not without risk, so bitcoins often get criticized for being too volatile to be used as a medium of exchange. And outside of niche circumstances, bitcoins are only lightly used as a medium of exchange in their current early stage of monetization.

Several cryptocurrencies market themselves as faster competitors to the Bitcoin network and thus better-suited as a medium of exchange. Putting aside smart contract platforms and proof-of-stake coins for the moment, we can do a cursory look through some of the notable proof-of-work monies that have sprung up in the wake of the Bitcoin network.

It’s natural for the market to explore multiple wrong answers to see in practice what the right answers are. Part of what allows me to analyze these concepts is the historical track record of why and how various projects failed to accrue value.

Litecoin was invented in 2011 based on the design of Bitcoin but with a few changes regarding how it is mined and how long its block times are, and marketed as “silver to Bitcoin’s gold.” Specifically, it uses faster 2.5-minute block times compared to Bitcoin’s 10-minute block times. It hit big highs in 2013 and then hit much bigger highs in 2017, at which point the creator sold his position at the top of the market. In 2021 during the altcoin season, Litecoin roughly matched those 2017 highs but wasn’t able to gain traction to go up multiples from those highs. After a long stretch of being in the top ten coins by market capitalization, it’s starting to stagnate and fall down the market cap rankings of cryptocurrencies and is no longer in the top ten.

As one of the oldest coins that continue to operate as designed, Litecoin’s price chart, denominated in Bitcoin, is a quintessential example of how most coins persistently degrade over time in Bitcoin-denominated terms after experiencing their initial price spike:

Dogecoin, created as a joke in 2013 based on the design of Litecoin, managed to hit notably higher highs in 2017 and then had a massive meme spike in 2021 thanks to pumping by Elon Musk, followed by a 90%+ crash. It has 1 minute block times and no supply cap. Numerous other dog-themed meme coins have come along in its wake, each having a brief spike before crashing. These joke coins tricked many retail investors into buying them at the top. Unfortunately, Several crypto exchanges marketed them aggressively to retail investors right at the top to make a quick buck. They, therefore, contributed to a bubble that sucked a lot of people in for major capital losses.

Monero, created in 2014 as a privacy-themed coin, has yet to decisively surpass its 2017 highs and has fallen very deep in the cryptocurrency market capitalization rankings. Monero uses some interesting privacy mechanisms but relies on indirect proofs to audit the supply, which means there’s a nonzero chance of an undetected inflation bug at any given time. Monero has 2-minute block times, and the way it is designed does not currently allow for a Lightning-like payment channel network to exist on top of it. I would like to see more privacy development within the Bitcoin ecosystem to make privacy techniques more automatic and easier to use.

Bitcoin’s hard forks, like Bitcoin Cash “BCH” and Bitcoin Satoshi Vision “BSV” have fared worse. Some went away, while others, such as these two, survived in a weakened state. They have in common that they increase block sizes so that more transactions can be packaged into each block. Both of them have gone down significantly in bitcoin-denominated terms. Bitcoin Cash, which was forked from the primary Bitcoin network in 2017, has yet to be able to touch its 2017 highs in dollar terms. Bitcoin Satoshi Vision forked from Bitcoin Cash in 2018, has been in a choppy sideways pattern since inception, is below the price it split at, and has been the subject of 51% attacks due to its low hash rate. If about 1% of Bitcoin miners want to make a 51% attack on either of these chains, they can do so since Bitcoin’s hash rate is orders of magnitude higher, and they all share the same hashing algorithm.

The main problem with having faster block times and/or larger block sizes is that if the network is heavily used, the bandwidth and storage requirements for running a full node become rather high, which makes it hard for the typical user to run a full node to audit the network. By extension, that makes the network rules less credible and immutable since the number of full nodes is tiny. Going too fast can also create problems with stability.

When we look at the adoption pattern of the Bitcoin network and some of its failed forks and competitors, we can quickly see a basic problem that many of these forks/competitors encountered and why they failed. They tried to make a broad medium of exchange out of something that was not a store of value and without the government’s power of fiat. And this was in addition to the fact that they had the big problem of existing in the shadow of Bitcoin’s far more dominant network effect.

They even went to sacrifice their decentralization, immutability, and audibility (a big piece of what could potentially make something like bitcoins a store of value) to advance their goal of being a medium of exchange. This path, however, leads to failure and irrelevance.

In other words, to invent a successful decentralized peer-to-peer Visa-type network (fast transaction layer), one must first invent an underlying decentralized peer-to-peer Fedwire-type network (settlement layer), along with a reason why the underlying unit should be held for the long-term compared to other assets (digital gold).

The fascinating thing about watching the Cambrian explosion of new private monies or “cryptocurrencies” since 2009, based on Satoshi Nakamoto’s creation of the Bitcoin network, is that it represents a new test for economic theories on what makes good money vs. what does not.

Everybody has a theory on what makes some monies better than others, but the market decides in the long arc of time. Even for government-controlled currencies, the international market decides between them. Any cryptocurrency can have success in the intermediate term. Still, the real test is which ones, if any, can stick around and gain structural adoption over many years and decades through bull and bear markets alike.

So far, the Bitcoin network has gotten through four huge bull/bear cycles (2011, 2013, 2017, 2021 bull cycles) while gaining value and users in an exponentially compounding way. Each bull cycle reached a scale significantly larger than the prior bull cycle in terms of market capitalization and the number of users.

Now, it is legal tender in a few regions of the world, and several large institutions hold it on their balance sheets in various ways.

Simple “bubbles” don’t survive through several 70%+ drawdowns over a period lasting thirteen years and counting; it looks more like Metcalfe’s Law of network adoption at this point. That doesn’t mean it is without risks. Still, it should be studied and understood rather than dismissed to see what it is about this network that allows it to keep growing through resistance.

YCharts

And most notably, bitcoin did this without any central organization promoting it. The inventor disappeared by 2011, and then even his follow-up lead developer and several other early developers left in the ensuing years due to various technical disputes involving the block size. It has been a rather decentralized, open-source, self-sustaining network of rolling participation ever.

Out of the other thousands of cryptocurrencies, the vast majority fail to successfully get through one cycle. They have a big bubble spike during a bull market, then crash, and never recover those bubble highs again. Founders, insiders, and others who bought super early can have spectacular gains on the back of the investors who came in late. Still, their coins don’t lead to structural adoption and growth. Only a small handful of them have made it through two or three cycles of higher dollar-denominated network value.

For the Bitcoin network, usage as a niche censorship-resistant medium of exchange came first, followed by its being used as a broader store of value, which became a much larger use case. From there, the more it is used as a store of value and the better its scaling solutions become, the more it can be widely used as a mass medium of exchange.

Let’s consider adoption patterns. Suppose you owned some bitcoins and other cryptos sometime in the 2011-2017 range when all of those various blockchain monies and forks were in the heat of their competition against the Bitcoin network as a medium of exchange and being marketed as such.

Before the launch of the Lightning network, if you were a person with easy access to banking and payment services and were not de-platformed from anything in particular, why would you spend Bitcoins on anything?

If the number of dollars keeps increasing yearly, but Bitcoins have a hard supply cap of 21 million coins, why would you want to give your Bitcoins to others?

Unless you’ve been holding Bitcoin so long that it has become a meaningful share of your net worth, or you actively work in the industry and potentially even get paid in Bitcoin, you probably wouldn’t.

This problem is then magnified by the fact that Bitcoins have ten-minute average confirmation times, Bitcoin cash coins have ten-minute average confirmation times, and even Litecoins and Dogecoins, which are meant to be faster, have 2.5-minute and 1 minute average confirmation times, respectively, which is still too slow for convenient in-person transactions. The process is longer if you want to wait for several confirmation times to reduce the probability that the transaction will be reversed. These are crappy things to buy coffee in that form. It’s like trying to buy coffee with a wire transfer. No thanks. That’s what Mastercard is for.

There are circumstances where the Bitcoin network’s base layer payment options are ideal as a medium of exchange, but to try to force it in a situation where it could be better, doesn’t make sense. As I described in my "What is Money, Anyway?" article, Bitcoin base layer payments are tank-like censorship-resistant. Owning Bitcoin represents the stored-up ability to make censorship-resistant global payments in the future and/or to portably bring wealth worldwide, even by just memorizing twelve words or holding a private key somewhere on your physical person or in your digital files.

This transaction problem is further compounded by the fact that every cryptocurrency transaction is a taxable event. Governments don’t want other monies to compete with theirs if they can help it, so they view your Bitcoins as commodities, and if you exchange them for something, you’ve now locked in a taxable capital gain. Assuming you don’t want to break tax laws, you need to keep track of every bitcoin/crypto transaction you do for tax season.

Furthermore, the number of people with any meaningful amount of their net worth in Bitcoin or other coins still needs to be higher. What is the immediate incentive for a merchant to accept Bitcoin or other coins unless they serve a niche industry where the percentage of Bitcoin or crypto users in their customer base is higher than normal?

I’ve described this merchant acceptance problem in prior research pieces when discussing the credit card oligopoly. Four meaningful card networks in the U.S. extend globally: Visa, Mastercard, American Express, and Discover. These have been around for decades. Merchants accept them as payment because that’s what all of their customers have in their wallets. Customers have them in their wallets because merchants widely accept them. These networks' flywheels were bootstrapped decades ago.

Creating a fifth credit card in the U.S. would be nearly impossible. You’d have to convince merchants to accept it despite users not yet having it, and you’d have to convince users to get one even though merchants don’t accept it yet. It’s hard to bootstrap from nothing and compete with existing network effects.

Bitcoins and various cryptocurrencies encountered the same problem. Some places accepted them as a novelty, and some people wanted to spend them here or there, but for the most part, the topic of cryptocurrencies as everyday payments was a dud during that whole 2011-2017 era, just like trying to launch a fifth credit card would be, except slower and more taxable.

The primary users of Bitcoin for the medium of exchange purposes in those early years were people who were de-platformed in various ways. Cypherpunks were naturally attracted to Bitcoin’s censorship-resistant payments. Wikileaks turned to accepting bitcoins when they were de-platformed from PayPal in 2010. A subset of early users bought drugs on the internet with bitcoins until those centralized marketplaces were shut down. Human rights advocates began using Bitcoin in authoritarian regimes with low banking access or vulnerability to arbitrary bank freezes. These use cases weren’t for efficiency but for peer-to-peer censorship resistance.

For mass medium of exchange usage, meaning far beyond niche censorship-resistant use cases, new money likely needs to become a store of value first if it is to arise organically rather than through government decree. And the payment experience needs to compete with various near-instant fiat payment methods. Many people need to have a lot of money and start asking merchants, “Why don’t you accept this yet?”

As it gets big enough or becomes perceived as offering better payment solutions than legacy systems, several jurisdictions can even remove the per-transaction tax on it.

Since store-of-value usage precedes mass medium of exchange usage, the fatal flaw of Litecoin, Dogecoin, Bitcoin Cash, Bitcoin Satoshi Vision, and most of these types of attempts at medium of exchange cryptocurrencies is that they put the cart before the horse.

As previously described, these types of projects wanted to sacrifice some degree of stability, decentralization, immutability, or auditability to optimize themselves as a higher-throughput medium of exchange, even though only some people were using them as a store of value yet, with negligible adoption. They were just building fintech payments companies with tiny teams of people and expecting to compete with Visa, despite having a worse user experience, slower speeds, and way less transaction throughput.

And yet, if we steelman their position, it’s somewhat understandable why some of them tried to do that: Satoshi Nakamoto described his original design as a peer-to-peer e-cash system, and what exactly “cash” is can have a few different meanings. In 2010, Satoshi briefly wrote about how the network could gradually scale in terms of block size over time, even though he also put the block size limit into the code. After he left, however, some people wanted to scale too much and too early without broad consensus to do such a contentious hard fork. By jamming hard forks through and going in their own direction away from the Bitcoin network, users of these other protocols had to go through the difficult experience of seeing how powerful the widely-distributed network of node users had become and how pushing unwanted updates to them is impossible.

I think too many people in those early years interpreted “e-cash” to mean quick-and-easy payments for everyday goods using the base layer when a better way to think of cash today is as a private censorship-resistant final settlement transaction method. Physical cash, after all, is not necessarily the easiest payment type or a medium of exchange that we need to use for everything, but it’s the most private and the hardest to prevent from occurring.

Therefore, when we think of “e-cash,” we likely shouldn’t think of it as optimizing for speed and efficiency right on the base layer for every transaction that we do, but rather we should think of it as optimizing for those same things that physical cash is great for private and censorship-resistant final settlement payments that can be used when it makes sense to do so.

Plus, bitcoin was already well-optimized for early adopters who wanted to use it as a private medium of exchange online at the time. Some of them viewed privacy as a fundamental human right. They were aware of oppressive regimes where this type of technology could be useful to protect people. Others were dealing with real-world constraints of other means of payment, such as Roya Mahboob, who used it to pay women and girls in Afghanistan, where female bank account access is more restricted. Bitcoin was also used very early by people using online black markets, in a similar way that criminals were early adopters of pagers as a technology (which doesn’t make the technology itself bad).

There were various niches of people where Bitcoin was an ideal medium of exchange from the beginning, and Bitcoin scaled well enough for those niches. Satoshi picked his variables very carefully to ensure that cypherpunks like him had a working anonymous censorship-resistant peer-to-peer medium of online exchange. So, it was and still is a very useful e-cash.

These types of people could and would wait 30 minutes for an online transaction to process with a few confirmations. They could and would run their own node. They could and would use private techniques to acquire and dispose of their coins. This was a utility network with a mild monetary premium. It offered money that a relatively small group of people at the time would desire to use and was recognized for its value by users and speculators. Like almost every commodity adopted as money, it had utility first. It gained a monetary premium second as a result of that utility. The utility was that it provided access to a tank-like medium of exchange network that could exchange value globally without centralized intermediaries to stop it and with a better combination of monetary immutability, censorship-resistance, and liquidity than the countless imitators that followed in its wake.

After enough time had passed, this fluctuating monetary premium of bitcoin’s price attracted speculators and investors that had no intention of using it for a medium of exchange any time soon, similar to why many people buy gold. A subset of Austrian economists, for example, began recognizing bitcoins as being interesting monetary goods; specifically, the finitude of the coin supply at 21 million stood out to some of them. When it became more broadly understood how immutable the Bitcoin network’s ruleset was and how its security, liquidity, and decentralization dwarfed any other proof-of-work cryptocurrencies, many people began considering it hard money. Several human rights activists began to recognize it as an ideal anti-authoritarian technology for its censorship-resistant aspects and use it as such.

The mistake of the Litecoin bulls and the Bitcoin Cash bulls and so forth was that they wanted to scale too early to a bigger group of people before there was a market for it, and even at the cost of weaker decentralization. Bitcoin’s base layer is enough for tens of millions of people to use it occasionally when its specific properties are ideal.

The Bitcoin network on the base layer is like the 60-ton armored tank of payment and savings systems: holding and transferring value globally in a censorship-resistant manner. A tank is ideal if you need to get from point A to point B through hostile terrain and blast through anything in your path. It’s not ideal for commuting to work. Trying to force base-layer Bitcoin transactions to be used as a daily of medium of exchange by the general public is like trying to make commuting in tanks catch on. It’s not going to because that’s not what it’s designed for. And to try to make it scale to everyone for all payments on that base layer makes it lose most of the properties that make it useful for what it does best. It would take over a terabyte of data storage per day to create a base layer system capable of supporting tens of thousands of transactions per second.

The earliest analysis of the Bitcoin network, by Hal Finney and others, predicted that the network would likely evolve towards a layered approach.

There are over 100 million people in the world who are estimated to own Bitcoin as of this past year. That’s 1-2% of the global population, depending on the exact number since the number is reliant on exchange data, surveys, and other opaque assessments. In some countries, however, the adoption percentage is in the low double digits.

However, most of that is pretty shallow. We can quantify adoption by both breadth and depth. Breadth would refer to how many people have a nonzero amount of Bitcoin. Depth refers to how much of their liquid money they have in Bitcoin.

What I mean by this, for example, is that someone having $264.34 USD worth of bitcoin sitting in a semi-dormant crypto exchange account is not “adopting” bitcoin to any economically significant degree.

As a thought experiment, imagine a world where people hold bitcoins and/or dollars as liquid money.

And furthermore, let’s assume (bear with me) that bitcoin continues to increase in dollar price over the long run, albeit with plenty of volatility along the way, as a result of bitcoin’s much lower rate of new unit creation compared to the rate of new dollar creation, and more people learning about Bitcoin and wanting to hold a nonzero amount of it. If someone buys a bit of Bitcoin, even without further purchases, it will become a somewhat bigger share of their liquid money over many years if this thesis is correct.

Now, only 1% of people own Bitcoin, and 99% do not. And suppose that those that own Bitcoin have just 3% of their liquid money in it on average. Total Bitcoin adoption is, therefore, 0.03% compared to 99.97% cash in that system. Bitcoin adoption in that context is negligible. There’s little reason for merchants to accept it other than out of novelty or if they specifically cater to cypherpunks.

If 10% of people own Bitcoin and have an average of 5% of their liquid money in it, then that is 0.5% total adoption compared to 99.5% cash. Still a rounding error, but nonetheless a niche market with millions of people.

If 30% of people own Bitcoin and have 10% of their liquid money in it, then that is 3% total adoption compared to 97% cash. That’s a vocal minority, representing a lot of niche purchasing power.

If 50% of people own Bitcoin and have 20% of their liquid money in it, then that is 10% of total adoption compared to 90% cash. That is a huge market.

If 70% of people own Bitcoin and have 30% of their liquid money in it, then that is 21% of total adoption compared to 79% cash. That’s enormous.

For many people to want to spend Bitcoin, it’s more likely that they would have bought some long ago and perhaps kept buying, took the time to learn how to custody it themselves rather than hold it on an exchange, and after years of price appreciation it’s a decent chunk of their liquid monetary value. They either want to sell some for cash to buy something, or even easier, just buy something with it directly.

Of course, in reality, it is bumpier than that. Some early adopters in this scenario will reach very high levels of net worth in Bitcoin, and they become a wealthy cohort to cater to by niche merchants early on. So mass merchant adoption might take a while, but of course, there would be early merchants that want to cater to that early group or that sell products that many Bitcoin holders would specifically want to buy.

If the numbers in the example above seem extreme (“How could Bitcoin possibly reach a 20%+ share of the dollar market?”), then re-run them for a developing country instead.

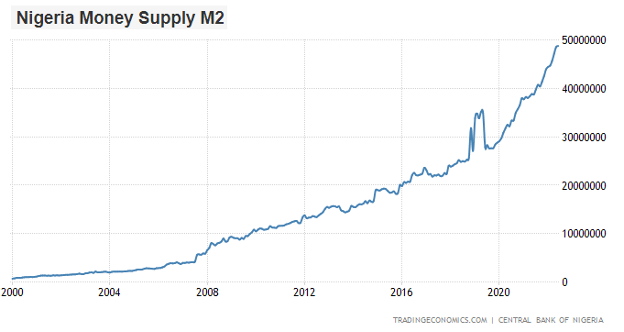

Replace the US with Nigeria, and the dollar with the Naira, in the above example. Nigeria has among the highest Bitcoin adoption levels in the world, even though their government has cut off the fiat bank onramps to Bitcoin/crypto exchanges to protect the Naira.

When a currency looks like this, people can and will try to find others to use, even through resistance:

Developing countries with higher average inflation and weaker payment systems are where bitcoins, via the Lightning network, can scale quickly as a medium of exchange. Because for many of them, it could indeed solve an everyday payments problem pretty early on in its monetization process.

That’s why there is often a huge mismatch in perceptions about Bitcoin between privileged commentators and actual users.

To the extent that the Bitcoin network continues monetizing and growing, it’s not because it eats the U.S. dollar or the Swiss franc first. It’s eating periphery currencies with high inflation, weak property rights, and/or bad payment systems first, and then it moves inward from there. Bitcoin is already bigger than the broad money supply of any developing countries and is accepted at more points around the world than many developing country currencies (generally only accepted within their issuing country or at a small number of specific exchange points internationally). Bitcoin merchant acceptance doesn’t have the density of any specific currency within that currency’s issuing country, but it has a wider international reach than most currencies.

The bigger the Bitcoin network gets, and over a longer period, the more rational it becomes for merchants to accept it. The more merchants that accept it, the stronger the network becomes because then Bitcoins don’t need to be converted back into fiat currency on one of a handful of centralized bank-connected exchanges for people who want to use them. In this sense, wide merchant acceptance is a form of censorship resistance. When thinking about this, think of merchants in developing countries more-so than just merchants in developed countries.

And over time, several companies have been created that allow a merchant to easily accept it and then either hold the Bitcoins or exchange them for fiat currency immediately so they don’t deal with the Bitcoins directly. The technical friction for accepting bitcoins as payment keeps decreasing.

Gresham’s law is the principle that “Bad money drives out good.”

If people have a good money and a bad money, they would rather spend the bad money and keep the good money. Ironically, the bad money tends to circulate with high velocity while the good money is hoarded with low velocity.

This trend revealed itself multiple times under bimetallic standards. When gold and silver were fixed relative to each other by government decree, but this “fix” was slightly off the global supply/demand ratio balance, which could change over time. One of the metals would start to disappear from circulation.

For example:

The United States began with a bimetallic standard in which the dollar was defined in terms of both gold or silver at weights and fineness such that gold and silver were set in value to each other at a ratio of 15 to 1. Because world markets valued them at a 15½ to 1 ratio, much of the gold left the country and silver was the de facto standard. In 1834, the gold content of the dollar was reduced to make the ratio 16 to 1. As a result, silver left the country and gold became the de facto standard.

Congressional Research Service, 2011

There are a couple processes for how that happens.

The first process is simply that the better (undervalued) money gets hoarded, so it stays in the country but gets removed from everyday circulation. People will not usually part with what they perceive as being undervalued.

The second process is that international entities can observe this and arbitrage it. For example, if the global ratio of gold to silver is 15.5 to 1, Americans have it fixed by government decree at 15 to 1 (slightly undervaluing gold vs. silver). A European entity can keep selling silver to the Americans and buying gold from the Americans. As years or decades pass, there will be a lot less gold in the United States and a significant amount of silver instead.

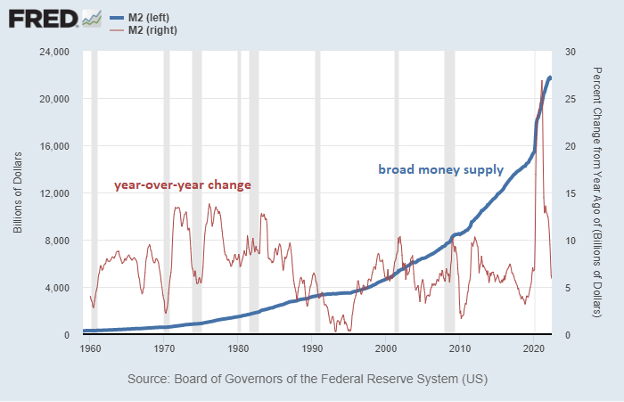

The U.S. broad money supply has grown at more than a 7% annualized rate since 1970. Most developed countries have a similar rate to that, and emerging markets tend to have a much higher rate on average.

St. Louis Fed

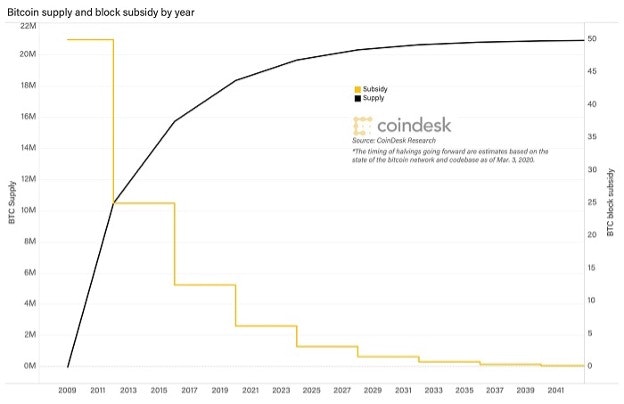

Meanwhile, the Bitcoin supply is growing at less than 1.8% per year, which will fall to below 0.9% in a couple years and to around 0.4% four years after that. The Bitcoin network is programmed to asymptotically approach 21 million Bitcoins in total by halving its supply inflation rate every four years until it has 0% supply inflation. And unlike most other blockchain monies, the wide node network helps ensure that no centralizing force can change this distribution pattern. It has the dominant network effect among proof-of-work blockchain monies, which makes it more protected against 51% censorship or transaction-reversal attacks.

Coindesk

It’s natural for people to want to hoard something like gold or Bitcoin and spend their dollars, pounds, yen, euros, yuan, pesos, naira, and rupees. Money that depreciates in value tends to circulate. In contrast, scarce money that tends to appreciate in value gets hoarded with much lower spending velocity.

This becomes especially true if a jurisdiction treats the harder money like property and taxes each transaction, which most jurisdictions do. If you try to use things like gold or Bitcoins as medium of exchange, each transaction is a taxable event compared to your initial cost basis when you originally bought that asset. The incentive, therefore, is to hoard the taxable gold or the taxable bitcoin, with their lower levels of supply inflation, and spend the non-taxable fiat currency on consumption, unless someone strongly desires Bitcoin’s censorship-resistant payments properties.

For example, bitcoins have been used as a medium of exchange by girls in Afghanistan, by Russian political opposition when their bank accounts get frozen, by Nigerian merchants and protesters, by people getting capital out of China, by people getting their money out of Venezuela, Iran, Palestine, and elsewhere, by under-banked people in El Salvador, and more. It’s also used in developed markets for natively-online services, such as Substack or buying VPNs, and many others. And yes, in the early years, people bought drugs online and occasionally for things like ransomware attacks.

I’ve met a number of these human rights advocates in person. One of the most powerful moments was hearing Ire Aderinokun, co-founder of Nigeria’s Feminist Coalition, speak in Norway’s parliament building earlier this year about how when they protested police violence in Nigeria, they had their bank accounts frozen and resorted to using bitcoins instead, for their self-custodial and censorship-resistant properties. I was familiar with that story from the news, but it’s always more interesting and clear to hear first-hand accounts of it from them in person.

In this sense, although Gresham’s Law initially applied to fixed exchange rates, it applies more broadly any time there is transactional friction of some sort, including a tax. The weaker, lower-friction currency will be spent first unless there is a strong practical reason to do otherwise, meaning a use-case that specifically needs Bitcoin’s unique properties.

So, a self-custodied store of value and payment system like the Bitcoin network is great for many people, but its exact usage pattern depends on context. It’ll tend to be adopted as a medium of exchange by people who need it a lot more quickly than people who don’t really need it.

An asset cannot monetize without volatility. By definition, an asset can’t go from being worth zero to having a market capitalization of a million dollars, to a billion dollars, to a trillion dollars, to several trillions of dollars, without upward volatility. That upward price move due to user adoption is volatile.

With that being the case, any upward volatility of this magnitude will attract speculators, leverage, and surges of demand. These speculators eventually get caught up and forced to sell for one reason or another, resulting in periods of sharp downward volatility.

When Bitcoin was held by 0.001% of people, it was extremely volatile and risky since the future was very unknowable, and a few individuals could massively affect the price with buy/sell decisions. When it became held by 0.1% of people, its volatility and risk decreased somewhat but remained high. Now that it’s likely owned in some way by over 1% of people, the risk and volatility keep reducing over time. However, they still are both at a significant level. If it gets to a stage where it is held by 10% or more people, then the volatility and risk would be further reduced.

So, early adopters mainly buy it because they analyze the qualities and consider it a useful network to access. They’re willing to accept the volatility for the long-run potential upside and self-custodial peer-to-peer access it provides. As more people come in, the asset becomes increasingly monetized.

Some ask, “What happens once the network runs out of new buyers?

Doesn’t that make it a Ponzi scheme?”

I addressed the Ponzi scheme comparison in this article and showed why it didn’t fit the characteristics of one. But more broadly, one must ask, “At what point would someone want to permanently exchange their self-custodial scarce money (Bitcoin) that has a 1.8% annual supply inflation rate that is exponentially shrinking for a soft money (fiat currency) that typically has a 7% annual supply inflation rate or higher?”

For many people, the answer is never, as long as the Bitcoin network is still working.

Instead, they want to hold and accumulate bitcoins until enough merchants accept them. At this point, they could spend some of them, especially if there is enough critical mass for them to become legal tender in more jurisdictions by that point. To the extent that they earn more income in the future, they’d prefer to continue to save at least some of that income in something with a fixed supply rather than other things like fiat currency that have an unlimited supply and are growing by new supply far more quickly.

In other words, if successful, the network becomes a self-sustaining global economy of people wanting to save in it, spend it, earn more of it, save more of it, and then spend it. Like, well… Money.

That’s why this meme has been one of the longest-running ones in the ecosystem:

When understood that way, risk analysis regarding the Bitcoin network should focus on questions like, “What events could potentially derail its monetization process?

What events could make the majority of users want or need to sell their Bitcoin, stop viewing it as good long-term savings, and instead hold something else?

What threats could censor the network, disable it, or otherwise disrupt its ability to serve as a tank-like medium of exchange and self-custodial portable savings?”

Those are the right questions to ask, in my view.

With the invention of Bitcoin, Satoshi Nakamoto put together several existing technologies and added some of his own touches to make a rather profound innovation.

For one, the network serves as a decentralized transfer agent and registrar. Proof-of-work miners process transactions (without relying on circular logic like proof-of-stake systems), and the network of nodes enforce the network rules. The result of this is the ability to quickly and globally transfer value without the permission of any centralized third party, as long as no individual entity or coordinating group of entities can persistently control the majority of mining capacity on the network and use that majority to censor it.

Secondly, due to the large number of validating nodes run by individual users, the network offers a credibly immutable set of 21 million units (each divisible into 100 million sub-units commonly referred to as “sats”) because there is no central authority that can change the number of coins on the network. Unlike most forms of software, updates cannot be “pushed” to users by developers; they can only be accepted voluntarily. The result of this is a rather interesting (albeit currently volatile) type of money.

It’s often said that a blockchain is basically just an inefficient database. Users, in this sense, are willing to accept inefficiency to ensure decentralization. They have to broadcast every change to the network and keep track of broadcasts from elsewhere in the network.

A blockchain, especially the truly decentralized variety, is a database that is small and tight enough that thousands of entities around the world can store it on their local devices and constantly update it peer-to-peer using an established set of rules. Each node provides validation to ensure that a new block is following the rules of the protocol, and they will only accept and propagate a new block to other nodes if the new block follows the rules. A large number of user-run nodes helps ensure that the ruleset is immutable. In contrast, if there are only a handful of nodes, it only takes a small quorum of people to rewrite the network rules.

Plus, the easier a node runs, the more auditable the network is for a regular user. More specifically, nodes simply give each user financial self-sovereignty to privately verify their transactions rather than rely on any trusted third party.

A fully-centralized database has fewer limitations because it doesn’t need to be small and tight. A large service provider can have an utterly massive database in a server farm. That can make things run very efficiently, but unlike with a blockchain, outside entities can’t directly audit it for content and changes and have no way to stop the owners of that centralized database from doing whatever they want with it.

So, every blockchain network that claims to improve something compared to the Bitcoin network on its base layer makes multiple trade-offs to do so.

To increase the number of transactions that can occur over a span of time on the base layer, either the block size or the block speed needs to be increased. However, this increases the bandwidth and storage requirements of running a node and often puts it out of the reach of a normal person. And in particular, if the requirements to run a node grow faster than the rate of technological growth in terms of bandwidth and storage, it leads to a shrinking node-set over time, which centralizes the network. Trying to scale the network to perform as many transactions as Visa just turns the network into Visa, a centralized entity.

To increase privacy, some degree of auditability needs to be sacrificed. One of the key things about the Bitcoin network is that any node can tell you the exact Bitcoin supply and has the entire history of transactions and the full state of the ledger. That’s not possible to the same degree in a privacy-based system. In addition, if a privacy-based system doesn’t have a serious network effect, privacy is not necessarily as perfect as advertised because the anonymity set is very small and is, therefore, somewhat trackable. Privacy is largely a function of liquidity, and if liquidity is lacking in various privacy-focused ecosystems, then their privacy potential is limited.

To increase code expressivity (e.g., executing complex smart contracts right on the base layer), a network must also increase the bandwidth and storage requirements of full nodes, making running a full node harder and thus centralizing the network over time, as previously described. In addition, it increases the complexity and number of possible attack surfaces. Lastly, it makes the network a means to an end rather than an end in and of itself, which means that many users will go towards whatever smart contract blockchains are cheapest.

Replacing proof-of-work with proof-of-stake requires accepting a circular validation process. In a proof-of-stake system, the coin holders are determined by the state of the ledger and the state of the ledger is determined by the coin holders, a perpetual motion machine based on circular logic, which doesn’t have high fault tolerance. It is nearly costless to make infinite copies of the blockchain with different transaction histories. If the network goes offline, there is no way other than governance decisions and centralized checkpoints to determine which ledger is the “real” one. It would be like a corporation serving as its own transfer agent and registrar for its shares, which is inherently circular. A proof-of-work system uses energy as that external arbiter of truth, which makes it non-circular and a true timechain rather than merely a blockchain.

Bitcoin has been largely successful due to its widely-distributed node network and the concept of “monetary self-sovereignty.” Anyone with an old laptop or Raspberry Pi and a basic internet connection can run a node and verify the whole system from Genesis. Decades from now, that will still be the case. The requirements to run a node increase more slowly than the technological increases in bandwidth and storage, which means that a node gets easier and more accessible to run over time. As a result, Bitcoin is inherently designed to get more decentralized over time, in contrast to most other cryptocurrencies that inherently get more centralized over time.

If developers want to change something about the Bitcoin network, their changes cannot be forced onto users' nodes. The ruleset of Bitcoin is determined by the network of existing nodes. In practice, any changes to the Bitcoin network must be backward-compatible upgrades, which node-users can voluntarily upgrade into over time if they want to while still being compatible with older nodes. Any attempted upgrades that are not backward compatible with the existing node network are merely hard forks- they create separate new coins like Bitcoin Cash that lack a network effect and lack serious security.

Trying to do a hard fork from the Bitcoin network is like copying all of the data from Wikipedia (it’s actually not that much) and hosting it on your own website, and then getting very little traffic because you don’t have the millions of backlinks that point to the real Wikipedia, or the volunteer army of people that constantly update the real Wikipedia. Your split version of Wikipedia would be inherently worse than the real one from the moment you copy it.

If nodes had much more requirements to run, then only large entities could run a node, and the set of nodes would be much smaller. A consortium of miners, exchanges, custodians, and other large entities could agree to make changes to the network. And if that’s the case, then immutability and decentralization are lost for the network. In particular, the 21 million finite supply could be changed, and the censorship-resistant properties would be threatened.

What gives Bitcoin its “hardness” as money is the immutability of its ruleset, enforced by the vast node network of individual users. There’s basically only a way to make backward-incompatible changes if there is a unanimous consensus to do so (e.g., for something like the eventual 2038 problem). Some soft-fork upgrades like Segwit and Taproot make incremental improvements, are backward compatible, and node users can voluntarily upgrade over time if they want to use those new features.

This software’s self-sovereignty and monetary immutability have been lost on other cryptocurrency designers. Based on some of his actions and writings, even Satoshi Nakamoto himself may have yet to fully grasp the near-immutability of his own network. Instead, it’s a property of the network that may have emerged and become realized over time, during and especially after he departs from the project. It’s certainly something I had to experience and research several times before I understood it.

Adam Back, whose 1990s development regarding proof-of-work was cited by Satoshi Nakamoto in the Bitcoin white paper, had this to say about it:

There’s something unusual about Bitcoin. So, in 2013 I spent about 4 months of my spare time trying to find any way to appreciably improve Bitcoin, you know across scalability, decentralization, privacy, fungibility, making it easier for people to mine on small devices, a bunch of metrics that I considered to be metrics of improvement. And so I looked at lots of different changing parameters, changing design, changing network, changing cryptography, and you know I came up with lots of different ideas, some of which have been proposed by other people since. But, basically to my surprise, it seemed that almost anything you did that arguably improved it in one way, made it worse in multiple other ways. It made it more complicated, used more bandwidth, made some other aspect of the system objectively worse. And so I came to think about it that Bitcoin kind of exists in a narrow pocket of design space. You know, the design space of all possible designs is an enormous search space, right, and counterintuitively it seems you can’t significantly improve it. And bear in mind I come from a background where I have a PhD in distributed systems, and spent most of my career working on large scale internet systems for startups and big companies, security protocols, and that sort of thing, so I feel like I have a reasonable chance if anybody does of incrementally improving something of this nature. And basically I gave it a shot and concluded, “Wow there is literally, basically nothing. Literally everything you do makes it worse.” Which was not what I was expecting.

CEO of Blockstream

So if every improvement makes an unacceptable trade-off, how can it get bigger? With only a few tens of millions of payments possible per month, how can Bitcoin potentially scale to a billion users?

The answer is layers. Every successful financial system uses a layered approach, with each layer optimal for a certain purpose.

If one layer is attempting to be used for all purposes, it makes too many sacrifices to be useful for almost anything in the long run. But if each layer of the system is optimized according to certain variables to serve a specific purpose (throughput, security, speed, privacy, etc.), then the full network stack can optimize for multiple use cases simultaneously without making unacceptable trade-offs.

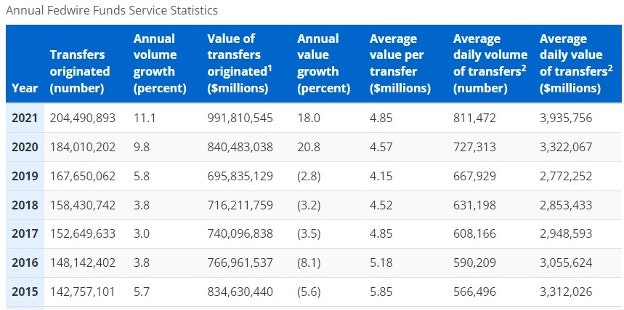

For example, in the U.S., we have Fedwire as a gross settlement system between banks. It currently does under 20 million transactions per month (~200 million per year) but settles over $80 trillion in value per month (nearly $1 quadrillion per year) because the average transaction size is massive. Each of these settlements represents a batch of many smaller payment transactions.

FRB Services

We, as consumers, don’t directly use that system. Instead, we use payment methods like credit cards, debit cards, PayPal, electronic checks, and so forth, and our banks record those transactions on their ledger and then settle with each other later. Each Fedwire transaction represents a batch of tons of smaller transactions from higher layers.

In other words, there is the underlying core settlement system and layers on top of it for more throughput, capable of settling billions of transactions per month.

Bitcoin’s ecosystem has evolved similarly, except in an open and peer-to-peer manner.

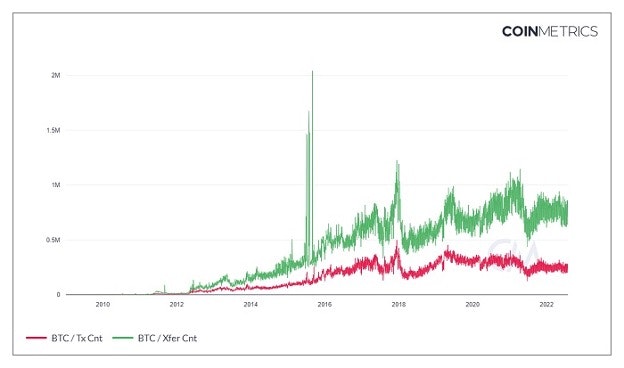

Bitcoin’s base layer can process up to 400,000 transactions per day. However, each transaction can have multiple outputs, resulting in up to 1 million or more individual payments per day. That’s a few tens of millions of payments per month, or a few hundred million payments per year, around the same ballpark that Fedwire currently handles.

Coin Metrics

From there, layers can be built on top of it to give it more throughput or capabilities.

For example, the Liquid Network is a federation of dozens of entities that wraps bitcoins in tokens called L-BTC. From that point, L-BTC is faster to move around, has somewhat better privacy, and can support smart contracts, including various other types of security tokens that run on top of it. A large number of L-BTC transactions can therefore be contained within two BTC transactions (one to peg in and one to peg out). The trade-off is that the user has to trust the federation, which is more decentralized than trusting a single entity but less decentralized than trusting Bitcoin’s raw base layer. The majority of Liquid’s functionary federation entities would need to collude against the system to violate user trust.

As another example and the focus of the rest of this article, the Lightning Network is a series of 2-of-2 multi-signature smart contracts that run on top of the Bitcoin base layer. These channels are peer-to-peer or peer-hub-peer and can support many transactions over time for each base layer transaction. The trade-off is that the channel must be kept online to protect the funds and receive payments. Additionally, the network has taken a few years to build up to usable levels of channel liquidity.

And from there, custodians can operate in layers above that for people that want them. Exchanges, payment apps, banks, chaumian mints, and so forth can all provide services to users willing to trust them with a portion of their funds. This can scale Bitcoin usage to any arbitrary level, including connecting with the Lightning Network. Each node on the Lightning Network doesn’t necessarily need to be one person; it could be a custodian with thousands or millions of users.

In that sense, each user interacts with the network in the layer (s) that makes the most sense for their specific needs.

The Lightning Network consists of a series of smart contract channels that run on top of the Bitcoin base layer.

And if you think about it, individual consumer payments make a lot more sense with channels, rather than being broadcast to everyone. If we do an in-person physical cash transaction, it’s directly peer-to-peer. We don’t shout our transaction to the whole world. Lightning replicates that cash concept on top of the Bitcoin base layer.

The result is a much faster, more scalable, cheaper, and more private global payment system, albeit with some trade-offs and limitations compared to directly using base-layer transactions.

Channel-based payments for the Bitcoin network have been explored since the early innings of the network. The white paper on the Lightning Network was written in 2015, and its first implementations came out in early 2018. Developers purposely restricted their channel size early on to grow cautiously and test things out safely in those early years (specifically to avoid the common problem of user funds being exploited, which we often see in DeFi).

The network has been functioning and growing ever since. By late 2020 the network reached a level of liquidity, usability, and critical mass that became quite interesting to me from a macroeconomic perspective.

Using a broadcast network to buy coffee on your way to work daily is a terrible idea. A blockchain is meant to be an immutable public ledger. Do I really need to broadcast my coffee transactions to tens of thousands of nodes around the world to be held in a distributed database for the foreseeable future?

What if I want to buy something more personally or politically sensitive than coffee? Shouldn’t I use peer-to-peer payment channels for that instead?

Imagine, for example, if every email sent on the internet had to be copied to everybody’s server and stored there rather than just to the recipient. That would be grossly inefficient. And yet, that’s how various high-throughput blockchains try to work regarding money.

Instead, I can open a channel on top of the broadcast network, pay for things that only me and the merchant know about (subject to some privacy caveats that will be mentioned later), and then close the channel with no immutable public record of those individual payments having occurred.

Any network that tries to scale transaction throughput on the broadcast-oriented base layer by radically increasing the block size and/or block speed makes no sense. The node requirements become absurdly high, which turns the network into a centralized Visa-like enterprise-scale database with just a handful of massive nodes. Changes can be made to the fundamental rules of the system at any time with the agreement of a handful of major node-running enterprises, and thus all future aspects of the system, including the supply of coins or who to censor the transactions for, becomes changeable. Privacy becomes very hard; various entities could track your net worth and payment history, which is bad enough in a benign environment and terrible in an authoritarian environment where half the world lives.

Additionally, a channel transaction will generally be faster than a broadcast transaction since it inherently requires propagation time to go through a broadcast network, even among the blockchains with the fastest block times.

That’s why every blockchain that attempts to scale transaction throughput too much on the base layer is inherently flawed. Bitcoin Cash, Bitcoin Satoshi Vision, Litecoin, Dogecoin, and other coins like this all sacrifice too much and become too centralized to do something that needs to make more technical sense in terms of scalability or privacy. In the long arc of time, they offer nothing of value.

The only way scaling makes sense and avoids sacrificing decentralization is to use a layered approach. Users can then pick their own solution, the layer (s) that make sense for them, depending on their specific needs.

Want to transfer a sizable amount of value permissionlessly or hold coins for a long time in self-custodial cold storage with the highest-possible security and immutability?

Use the Bitcoin network base layer.

Want to make a lot of instants, cheap, private, permissionless payments using a self-custodial solution, albeit with occasional on-chain transactions to open or close a channel?

Use the Lightning Network self-custodially. Various technologies, including Blockstream’s Greenlight and mobile applications, make this increasingly easy to do by abstracting most of the technical details away from the user while still having the user retain their own private keys. Or if they want to be hands-on, they can be.

Want to make super easy permissioned payments for free and potentially get other perks but at the expense of giving up custody?

Use a custodial service like Cash App, which uses the other two layers. And maybe in the future, there will be more private custodian solutions in the Bitcoin network ecosystem, like federated chaumian mints that use blind signatures. Federated custody options will potentially be more available, which spreads out custodial risk.

Each layer builds upon the lower layer without reducing the qualities of that lower layer. A broadcast network on the base layer, a channel network on the middle layer, and a custodian ecosystem on the upper layer gives each type of user whatever they are looking for. If growing pains become apparent, other scaling technologies may come into play in the future to further increase the number of people that can interact self-custodially with the system.

Bitcoin uniquely came into existence and is purposely hard to change, making it a decentralized digital commodity rather than a centralized digital equity. Instead of trying to create something separate, developers can build on top of it.

Suppose you and your friends are spending a long evening at a bar.

Rather than get your payment method for every round of drinks, it’s preferable to open a tab with the bartender and settle it at the end of the night. If the bartender doesn’t know you, you can offer your credit card information ahead of time so they can charge it later that night.

In a manner of speaking, you and the bartender open a payment channel with each other. There is a moment of friction when setting up the tab and a second moment of conflict when closing the tab. Still, between those moments, there is no payment friction for individual rounds of drinks because you just need to tell the bartender, “Another round of drinks, please” and it happens.

That’s how the Lightning Network works, conceptually. I can open a channel with someone else with a base layer Bitcoin transaction. This channel is a 2-of-2 multi-signature channel, meaning we both have to agree on it. It’s designed so that we can unilaterally close the channel if we need or want to (although we should do a cooperative close). While the channel is open, we can transact any number of times, as long as we have sufficient liquidity in the channel, until one or both of us want to close the channel with another base layer bitcoin transaction.

Unlike a bar tab, however, a Lightning channel is not based on trust or debt. Payments within the channel are updated instantly, and the ongoing tab can be enforced by either party closing the channel and reconciling with the base layer, with each side receiving its current balance. There is no debt, no promise to pay later, from one person to another. It’s like instantly transmitting money to the bartender’s account through the channel whenever you ask for another round of drinks.

Let’s take this a step further. Alice has a tab with the bartender at a bar, and another person, Bob, also has a tab open with the same bartender. If Bob wants to buy Alice a drink, he can tell the bartender to give Alice a drink and put it on his tab. Alternatively, if Bob forgot his wallet and needed money to get home, Alice can tell the bartender to give Bob $30 and put it on her tab. Alice can pay Bob through the bartender, even though Alice and Bob know nothing about each other and have no payment channels open with each other.

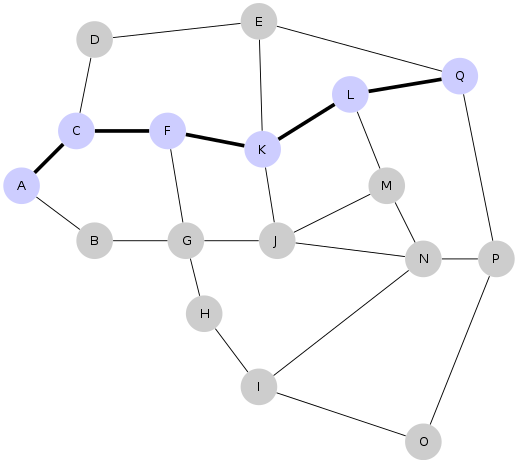

The Lightning network does that, too, but without debt or trust. The following is an example diagram.

If user A wants to send a payment to user Q, she can do it by routing the payment from A to C to F to K to L to Q. Each node in the middle might charge a tiny routing fee, like a fraction of a penny since it’s easy to automate.

She doesn’t need to set up a channel directly with user Q.

Kierish, via Wikipedia

Because it uses onion routing technology, the nodes in the middle don’t necessarily know where the payment originated from or where it is going to its final destination. Node K is told “route this payment from F to L” without being told more than it needs to know.

The end result of this network of channels is that one base layer transaction gives you access to a large number of individual payments to various separate entities. Thus the Bitcoin network can be scaled rather significantly.

Imagine a global system with a massive number of interconnected nodes. Anyone can enter the network with a new node and start creating channels. Alternatively, many custodial services also give account holders access to the network through their nodes and channels.

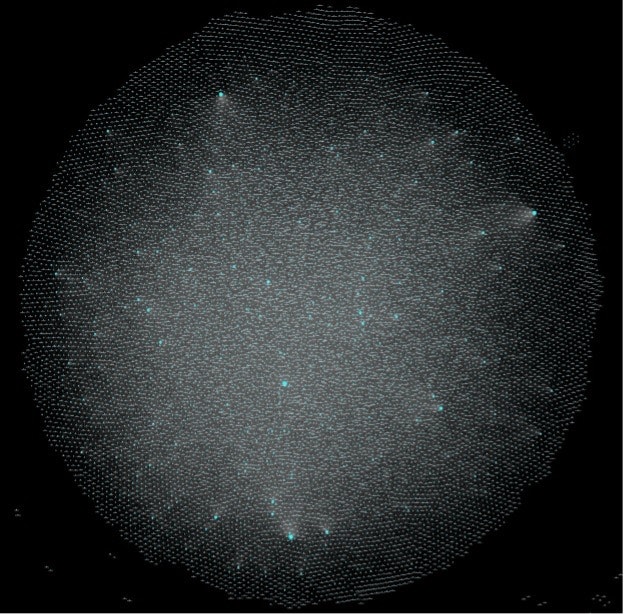

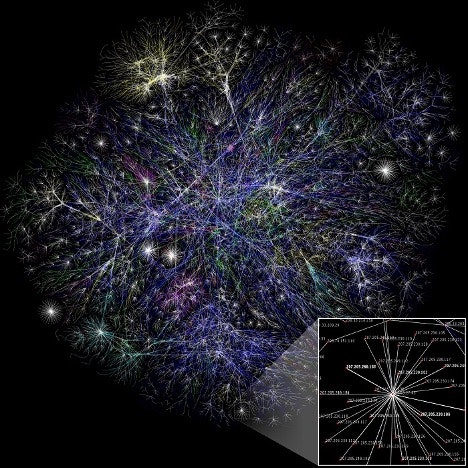

Here’s a visualization of the public Lightning network at the moment. It’s a growing network of interconnected nodes connected by payment channels, with those bigger dots representing exceptionally well-connected nodes:

LnRouter

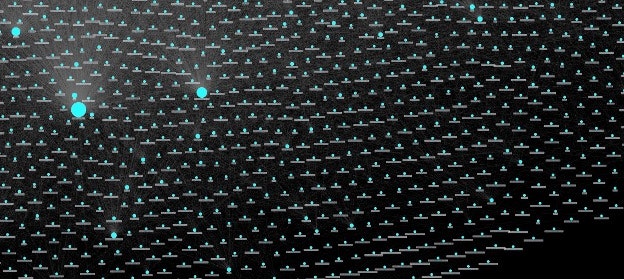

And here’s a zoomed-in shot of the bottom left area to show a random sample of the shape of connections that is typical throughout the network:

Since the network is pretty efficient, transaction fees are often the equivalent of a penny or less.

There is no hard limit to how big the network can get over time and how many transactions per second the network can handle other than the fact that opening and closing channels result in base-layer transactions. The Lightning Network, if it gets to the size of having millions of open channels in the future, can theoretically handle an almost unlimited number of peer-to-peer transactions per second. Still, there’s an upper limit of tens of millions of new channels that could be opened per year (depending on what percentage of base layer transactions are channel openings).

Although it has some constraints, especially in this early development phase, this type of network makes a lot of sense from a payments perspective. Peer-to-peer channels are better than broadcast networks for small individual transactions. They’re fast, cheap, and relatively private.

Plus, the network can do micropayments much smaller than what Visa and Mastercard can do. With Lightning, you can send payments worth a fraction of a penny. This opens up new use cases that aren’t possible with credit cards, such as machine-to-machine payments, the streaming of micro-payments, or the usage of micro-payments as a spam-prevention technique.

All of this is global and permissionless. Users can do it without asking the permission of a bank or other central entity. To prevent it, governments need to actively tell their citizens that it’s illegal to use certain types of free, open-source software and then figure out how to actually enforce that.

Liquidity is the biggest limitation of a network that relies on individual routing channels.

If there are only hundreds of participants, it could be pretty hard to find a route that connects any two arbitrary nodes and has enough liquidity on each channel in the path to pass the payment through. A lot of attempted payment routes will fail. The funds won’t be lost, but the transaction will fail to initiate. The network will be limited, and the user experience will be poor.

Once there are tens of thousands, hundreds of thousands, or millions of participants, and with larger average channel balances, routing a payment from any arbitrary point to any other arbitrary point on the network becomes exponentially easier and more reliable. There is a very large number of possible paths between most points on the network.

In the Lightning Network, the larger the payment you want to send, the harder it will be to find a set of channel paths that collectively have enough liquidity to handle that payment. For example, it’s pretty easy to send the equivalent of $25 between two points on the network because your software merely needs to find a set of interconnected nodes that end up each with at least $25 worth of liquidity in the direction you want. However, sending the equivalent of $2,500 to many destinations is harder because there are fewer channels with that much liquidity. Instead, your payment may need to be sent in parallel through multiple paths. So there must be many possible paths between your node and the target node. Additionally, the target node may simply not have enough total inbound liquidity to receive a payment of that size.

The more channels exist, and the bigger the channels are, the more reliable it becomes to route larger payments.

Due to this dynamic, the Lightning Network isn’t a light switch that could just be turned on and work perfectly from day one. Over the years, it had to be painstakingly built, channel by channel. The early users were high-conviction developers and early adopters working their way through a difficult-to-use network, and only after they spent years working on it did it become relevant for a typical user who just wants cheap and fast payments. Initially, they limited channel sizes and payment sizes for user safety. Think of them as slowly hacking raw paths through the jungle with machetes so that one-day roads may be built for civilization.

Furthermore, tools had to be built along the way to make it easier for node operators to manage liquidity optimally. Those have gotten better, but it’s still a work in progress.

Many critics said the network would not work, and once it was implemented, many people for the first couple of years said it was a dud. Most of them, however, needed to understand how it grows. The Lightning Network is like one of those giant freight trains with miles of cars behind it; it takes a ton of work to get up to speed from a standstill, but then it’s practically unstoppable once it gets going with tremendous momentum.

Pixabay

As the Lightning Network becomes more usable, the companies building implementations or applications for it can raise more capital from interested investors. For example, Lightning Labs raised a $70 million series B round in 2022 to continue building the Lightning Network infrastructure. Zebedee raised $35 million (including from game giant Square Enix) to continue building solutions for games to incorporate Lightning micro-payments. There have been hundreds of millions in total capital raised over the past few years for wallets, apps, infrastructure, and more.

Then, entities with a large number of users can connect to it. Bitfinex and River Financial integrated Lightning for their users in 2019. Bull Bitcoin and Okcoin integrated Lightning for their users in 2021. Cash App and Kraken integrated Lightning for their users in 2022. Tens of millions of people now technically have access to the Lightning network if they want it. A lot of merchant software accepts it now too.

By January 2021, I noticed that the network was starting to reach a critical mass of liquidity and usability. Lightning was becoming truly usable, meaning that payment routing was becoming more reliable. The initial capacity of the network was bootstrap liquidity and wasn’t efficiently allocated. For a while, the network looked from the outside like it wasn’t growing when that liquidity was slowly spreading out to become more usable and efficient. And then, boom, liquidity, and payments started to take off, and some excellent mobile apps came to market.

Look Into Bitcoin

No company controls the Lightning network. It’s an open-source set of participants.

The basic foundation of the network is an agreed-upon minimal protocol, which makers of Lightning node software adhere to if they want to operate with each other and the network as a whole. These standards are like basic email standards or basic internet standards for various applications to communicate with.

Lightning node software is referred to as a Lightning implementation. Lightning Labs, Blockstream, and Block Inc are the businesses responsible for the three biggest Lightning implementations or implementation tool sets that various developers use.

If you want to be hands-on, you can choose which implementation to use, customize an implementation, or even build your own implementation from scratch. No gatekeeper stops anyone from building their own lightning implementation and using it to interface with the rest of the network; it’s an open protocol.

From there, many companies can incorporate these Lightning implementations into easy-to-use apps. An end-user won’t directly use a Lightning implementation; they will use a mobile app that allows them to connect with the network and obscure most of the technical details from them, including the details of the Lightning implementation under the hood.

Some apps can be custodial, meaning you trust a company with your money. Cash App and Strike are examples of this. This comes with specific amounts of regulatory compliance in various jurisdictions.

Other apps can be self-custodial, meaning you have complete control over your coins. They are just using their open-source software and connecting with highly-liquid nodes. Muun and Breez are examples of this.

When the initial network implementations were launched, few merchants accepted Lightning payments.

Over time, it became easier. BTCPay Server and OpenNode, for example, allow merchants to easily accept Lightning payments.

When El Salvador made bitcoin legal tender, large companies like McDonald’s and Starbucks could quickly integrate Lightning payments using third-party software.

NCR Corporation and other point-of-sale companies have expressed interest in becoming interoperable with the Lightning network. Square is a large point-of-sale software and equipment provider for small and medium-sized businesses, and its parent company Block Inc is one of the most pro-Bitcoin companies. Their Cash App already integrates with Lightning, and they have multiple Bitcoin-focused development units.

Over the next several years, it will be increasingly common to have Lightning as a payment method. Some merchants will convert to dollars immediately upon sale (which is easily implemented by many point-of-sale software providers). At the same time, some will choose to directly accept Bitcoins over the network and keep them.

For a couple years now, interest has increased in using the Lightning Network to transfer dollars or other currencies.

The idea is that Bitcoin is an increasingly liquid asset that trades in most large currencies. Someone can exchange dollars for Bitcoin, send Bitcoin over the Lightning Network to another custodian in some other country, and then exchange it back into dollars, all within a couple seconds. This allows someone to use Lightning’s payments aspect separately from Bitcoin, the volatile asset.

This can be done with other currencies as well. Someone can exchange pound sterling for Bitcoin, send the Bitcoin over the Lightning network, and then exchange that Bitcoin for euros within seconds.