Swan Private Insight Update #18

This report was originally sent to Swan Private clients on December 9th, 2022. Swan Private guides corporations and high net worth individuals globally toward building generational wealth with Bitcoin.

Will a fixed supply money lead us, as some warn, to economic catastrophe?

Firstly, why is this question important, especially to Bitcoiners?

To become a proponent of Bitcoin, one must believe that:

Sound money (particularly non-state, immutable, fixed supply, digital, censorship-resistant, self-custodial, peer-to-peer money) will bring about a better economy and society than expansionary money and credit;

Bitcoin is built and designed such that it is capable of continually functioning as sound money.

This report was originally sent to Swan Private clients on December 9th, 2022. Swan Private guides corporations and high net worth individuals globally toward building generational wealth with Bitcoin.

To believe item number 2, one must have at least a basic understanding of cryptography, computer science, and game theory. But most people don’t spend any time even considering item number 2, because they believe the economic dogma of our time, which tells us that a fixed supply money leads to economic catastrophe. From my nearly 13 years at Goldman Sachs, I can tell you firsthand that the vast majority of people who work in legacy finance believe strongly in this dogma.

This means that even if Bitcoin is built and designed to be exactly what it claims to be (non-state, immutable, fixed supply, digital, censorship-resistant, self-custodial, peer-to-peer money), AND even if every company/platform/app/device that supports the Bitcoin ecosystem is built to perfection, this economic dogma of our time tells us that none of that matters because sound money is something to be feared.

If someone believes that sound money leads to economic catastrophe, they will never listen to a word a Bitcoiner has to say about distributed ledgers, proof-of-work consensus, nodes, miners, mempools, hashes, nonces, SHA256, private keys, seed phrases, signing devices, UTXOs, or layer two scaling solutions. They believe that the economic catastrophe brought about by sound money will lead to worse outcomes for individuals, families, and our systems of government, education, food, healthcare, science, architecture, etc. They will not be on board with the idea that Bitcoin fixes anything.

Therefore, Bitcoiners are faced with a critical task: communicating, in clear language, why the current mainstream thinking on sound money is flawed. It is an imperative task which must be tackled to pave the way for mainstream Bitcoin adoption.

Let’s describe the beliefs held by proponents of expansionary money and credit:

We must have expansionary money and circulation credit to achieve more economic growth.

Fixed supply money leads to prices declining over time, which leads to hoarding money, which means lack of spending/investment, which means high unemployment and economic recessions.

It is unjust that someone could see their purchasing power maintained or increased over time for “doing nothing” other than holding money.

We need an expansion of money and circulation credit to redistribute resources from the haves to the have-nots.

We need an expansion of money and circulation credit to “stimulate” our economy during times of recession.

We’ll need to start by addressing a few critical questions:

What is economic growth?

What is money?

What is credit? Particularly, what is commodity credit vs circulation credit?

Economic growth is the increased and/or more efficient production of real goods and services in the economy. Humans use capital to accomplish this. Capital is anything and everything that allows us to more easily produce goods and services. Key components of capital include human knowledge, skill, manual labor, innovation, machines, natural resources, specialization, and free trade. I would argue that property rights and a morally principled society are also forms of capital, which allow for better economic growth.

If you’re interested in a deeper discussion on what constitutes capital, my colleague Steven Lubka wrote a fantastic article on the topic titled Capital Misallocation: Bitcoin Fixes This. For now, the point is that capital includes anything and everything that allows us to more easily produce goods and services.

Money, when functioning properly, is simply a tool that facilitates multi-party trade which would otherwise be complex or impossible. Trade allows us to specialize and produce things more effectively.

Money allows us to overcome what is known in economics as the “coincidence of wants” problem. Imagine you are a dentist, and you are in need of a new pair of shoes. Without money, you would need to find not just a shoemaker, but a shoemaker who is also in need of a teeth cleaning. Good luck with that! Without money, commerce would grind to a snail’s pace. Without money, trade would be limited to barter (direct exchange), and humans would likely only produce the things they need in life themselves. This is the opposite of specialization, and it would significantly hamper our ability to innovate and produce things more effectively.

Money allows you to sell your dentist services to a massively larger pool of people. The impacts of this cannot be overstated. To be clear, prior to the existence of money, in order to receive something of value for your dentist services, you had to find a shoemaker who needed a teeth cleaning. With the existence of money, your dentist services can be exchanged for real value with anyone who is in need of a teeth cleaning who has produced a surplus of their own, which they can exchange with you (in the form of money). You can then use that money to exchange with anyone else who is willing to exchange a surplus that they have produced. This is why money, as a tool, is an absolute necessity for achieving human progress in the material world (i.e. economic growth).

Money allows us to become wildly better and faster at trade and specialization, which allows us to produce things far more efficiently, bring down costs in real terms, and invent things that our ancestors couldn’t even think of. The idea that money allows for increased trade and specialization is profound. It means that many professions and industries we take for granted today would not even exist if it were not for our ability to use money.

Credit is a contractual agreement between two parties where one party exchanges something of value today, and the other party commits to provide their side of the exchange in the future. The terms credit, debt, or loan ultimately describe the same thing.

Based on the above descriptions, it should be very clear that money is inherently different from credit. If you own a proper form of money, there is nothing else required for the money to have value. If you own a credit instrument, the value of that instrument is contingent upon repayment from the borrower.

We also must distinguish between “commodity credit” vs. “circulation credit”. This is easiest to explain in the context of a gold standard, i.e. gold serves as the base layer of money in an economy.

Commodity credit would be a loan of 100 ounces of gold from one entity to another. Clearly, only one entity can access the 100 ounces of gold at a time. Once the lender loans the gold to the borrower, the lender no longer has access to the gold because gold is a bearer instrument and can only be in the possession of one entity at a time. Therefore, lending commodity credit does not create additional monetary units in the system.

Circulation credit would be when a bank is securing 100 ounces of gold in its vaults for its clients and the bank makes a loan of 90 ounces of gold, but they don’t lend the physical gold itself! Instead, the bank issues a paper (or digital) claim to a borrower that says the borrower now has 90 ounces of gold. But at the same time, the bank tells its customers who deposited the 100 ounces of gold that they have persistent access to all their gold. As a result, there are now effectively 190 ounces of gold (and claims to gold) in the system. The critical takeaway is that circulation credit is treated as money and therefore results in an expansion of the monetary units in a system.

Now let’s respond point-by-point to the beliefs held by proponents of expansionary money and circulation credit.

We need expansionary money and circulation credit to achieve more economic growth.

If that sentence reads as immediately absurd, you most likely don’t have a degree in economics, and for that you should be thankful! You likely have a knack for engineering or the hard sciences which enables you to quickly spot a flaw in logic and design. You might be thinking: how on earth could the creation of new monetary units (whether they be metal, paper, or digital) lead to real-world economic growth? It would be akin to thinking that if we declare one foot now contains 20 inches, we will be able to build more houses. Unfortunately, modern economics has done so much damage to our ability to think clearly. Many people are firmly attached to the idea that more money and circulation credit is required for economic growth. The reason for this article is to help people unlearn the flawed ideas which have permeated the world of economics, finance, academia, central banking, and politics for the past 100 or so years.

One way of highlighting the flaw in this idea is to understand that projects and investments are not actually funded with “money” (which is simply an abstract tool that facilitates multi-party trade) in the same way that houses are not actually built with inches. Projects and investments are funded with real-world resources, the same way that houses are built with real-world resources. Investment must come from the saving/surplus of real-world resources, regardless of the existence of circulation credit. This is not something we can change no matter what economic theory we subscribe to. Importantly, projects and investments might appear to be funded from circulation credit when a bank issues an out-of-thin-air loan to a borrower, but that appearance is merely an illusion. Let’s say a borrower gets an out-of-thin-air loan from a bank, and they use the loan to buy machinery to create a business. The very fact that the machinery was in existence and available for purchase is savings/surplus. In order for anyone to have something to offer in exchange to someone else, by definition, that something is their savings/surplus.

So if the creation of more money and circulation credit does not actually make more real-world resources available for investment or consumption, what exactly are the effects of creating more of it? The immediate result is a dilution of the value (aka confiscation of wealth) of all pre-existing money holders, i.e. savers. This is true because money is an abstract asset which is not directly consumed. For assets of this nature, their value can only be understood in reference to the total supply.

Let’s consider assets which are directly consumed. These types of assets are clearly not subject to this same dynamic. If you own a five thousand square foot house on five acres with a swimming pool, and someone builds a new house somewhere in the world, which is ten thousand square feet on ten acres with a bigger pool, has your asset changed? To be clear, the question being asked is: if more houses and pools are created, has something changed about what you already own? No. The only reason this would start to matter is if you want to sell your house, but in that case your house is no longer an asset you directly consume. The only other reason it might matter is for signaling/social media purposes. But let’s put aside that shallow human tendency which we are all better off ignoring.

If you own ten thousand shares of equity in a company and the company subsequently doubles the amount of shares outstanding, has the value of your asset changed? Yes. This is because your asset’s value is a direct function of the percentage of the total supply. This is why the act of issuing new shares in a common enterprise is so heavily scrutinized — because the current shareholders know that their ownership is being diluted. The process basically goes like this: a stakeholder of the company (could be the board, an executive, a large shareholder) makes the case that the company needs more funds to execute their business strategy. The other shareholders say “WHOA HOLD ON, you better have a damn good business strategy because if you create a bunch of new shares and your strategy doesn’t make the company more valuable, then you’re just reducing the value of my property by transferring my value to these new shareholders.” Again, this dynamic applies to ownership of shares in a common enterprise because you don’t directly consume your shares. It does not apply to assets that you consume directly whether that be homes, food, cars, phones, clothes, etc.

What’s fascinating is that people in traditional finance understand the concept of ownership dilution of abstract assets when it comes to shares of stock. But they somehow don’t understand this when it comes to money! Regardless, the principle holds true — the value of the money you hold can only be understood in reference to the denominator (total supply) of the money. It’s that simple. When new money is created, either by direct creation of new monetary units, or the creation of new circulation credit, all pre-existing money holders see their value diluted as a result.

Proponents of expansionary money and circulation credit will say that as long as those who received the new money/credit use it successfully to create more goods and services, then they have added wealth and created new value for society, so we end up better off than otherwise. Plus when the debt is paid back, the money supply is reduced back to what it was before the debt was issued. What’s there to complain about, right?! In reality, this presents both ethical and intellectual issues.

As discussed, the immediate result of creating new money and circulation credit is a dilution of the value (aka confiscation of wealth) of all pre-existing money holders. If a bank creates a loan out of thin air and gives it to a presumably legitimate entrepreneur, that entrepreneur will immediately use the loan to purchase real world goods and services to help him build his business. Where did that purchasing power come from? The entrepreneur did not produce and save resources in order to fund his purchasing power, and nor did the bank who simply created the loan out of thin air! The purchasing power was extracted from the real savers in society — those who produced a surplus of real value — some of whom didn’t qualify for a loan of thin-air money, but also might have wanted to build a business, but are now priced out from using the money they had saved.

Even if I have a really good business idea and I end up creating economic growth, does that make it morally acceptable for me to extract value from other people — who had no say in the matter — to fund my idea? And let’s keep in mind that if I’m wrong and my business idea does not succeed, this could cause the failure of the fractional reserve entity who lent me the funds, which would lead to one of two things happening: 1) Depositors of the fractional reserve entity, i.e. pre-existing money holders, cannot withdraw their funds because the funds are simply gone as a result of the bad investment, or 2) A central bank comes in as a “lender of last resort” and makes the fractional reserve entity whole by creating new monetary units out of thin air — a bail-out. In scenario 1, it’s obvious why this results in a bad outcome for pre-existing money holders. In scenario 2, pre-existing money holders also lose because their wealth is confiscated via monetary debasement, as a result of the fact that money is an abstract asset whose value can only be understood in relation to its total supply. Personally, I cannot see how one could claim this is a morally acceptable arrangement. The resources are extracted from others in society to fund the loan. The risk of loss is transferred — unknowingly and involuntarily — to the depositors and/or to society at large.

Said another way, let’s say I counterfeit $1 million in my basement. I then use those funds to create a business. My business is successful, such that I generate well over $1 million of earnings after the first year. Then, out of those earnings, I make the choice to destroy $1 million (to offset the $1 million which I know that I created out of thin air). Would this be morally defensible? It would not be. No one else in society was consulted when I created the $1 million from thin air which I then used to purchase real-world resources to build my business. And the risk of my business being a failure was borne by society at large. So even if my business is a success and I destroy all of the money that I previously counterfeited, the question remains: where did I get the purchasing power to buy all the things to start my business?

In other words, heads I win, tails you lose.

Intellectually, the proponents of expansionary money and circulation credit might argue that we’re all better off if the entrepreneur created valuable goods and services and paid back his loan, and let’s just ignore that the purchasing power was actually funded by extracting resources — unknowingly and involuntarily — from society’s savers. However this ignores the defective incentive structure produced by a system of expansionary money and circulation credit, which leads to poor decision-making and economic destruction. In practice, we often don’t see well-intentioned entrepreneurs borrowing money to build great businesses and then returning the money. What we see are opportunists often taking advantage of access to this money to buy up already existing resources for their enrichment. We also see ordinary people borrowing excessively because they must in order to keep up with the opportunists. We all get caught up in the race of getting our hands on the expanding supply of money issued out of thin air — if we can. If we can’t then we are left behind. Lastly, ask yourself the question: who will more carefully and responsibly build sustainable projects/investments of real value? Will it be those who received the funds directly from either their own real savings or the voluntary contribution of real savings of others? Or will it be those who received the funds via cheap and easy credit which was issued out of thin air?

There is an additional method by which the creation of money and circulation credit affects economic growth. It results in a distortion of the price signal, which is a critical component for directing economic activity and creating economic growth. A distortion of the price signal will almost certainly result in artificially exacerbated booms and busts, i.e. worse economic growth, or perhaps outright economic destruction. During the boom period, where circulation credit is expanding, we often do not see real growth, but the illusion of growth. If a borrower of an out-of-thin-air loan uses the funds to purchase machinery, the seller of machinery is given the signal that a new savings/surplus was produced in society which led to this new purchasing power for the machinery — recall that trade is simply the exchanging of savings/surplus. But in reality, there was not a new savings/surplus generated, because the loan was issued out of thin air. This dynamic causes confusion throughout the economy. Business owners are given inaccurate signals telling them that more savings/surplus exist in the world. This causes them to position their businesses for a world which does not actually exist. This leads to bad business decisions and eventually economic recessions when these bad decisions are revealed. Consider homes as another example of the illusion of growth. Just because the price of homes, or the GDP, is going up, does not mean that their value is. Consider a three bedroom home that sleeps and provides shelter for a family of four. Its real utility stays exactly the same whether it’s priced at $100,000 or $1,000,000. The price of this home, in our debt-based economy, fluctuates largely because access to thin-air money is expanded or contracted by the monetary system we currently use, which generally increases the money supply and makes houses available to those who can access credit.

But the economy is not getting more valuable and serving more people when the prices of assets as measured in inflationary money increases. It merely means that those with access to the new money/credit can access more of the resources of the economy.

Let’s describe how projects and investments can instead be funded in an ethically and intellectually acceptable way.

In a world of commodity money and commodity credit, the system only allows for certain types of investment funding, by definition. Commodity money typically means that no one has the ability to create new monetary units out of thin air. Commodity credit means that you are simply choosing to lend your commodity money which you previously earned and saved. And during the loan period, no one considers the loan itself to be a form of money. Therefore the money supply is not increased, and investments are funded directly, honestly, and voluntarily by real savings.

In a world of circulation credit, I do believe there could be a way for it to exist in an intellectually and morally acceptable way. The fractional reserve entity would need to be transparent regarding exactly what they were doing with customer deposits. The risk of loss would have to be placed on only those who voluntarily opted in to holding their money with the fractional reserve entity. There could be no government/central bank coercion for market participants to treat circulation credit from different issuers the same way. There could be no government/central bank bailouts which simply socialize the inevitable losses of a fractional reserve system. I personally believe that circulation credit would be small or non-existent in a truly free market, especially one where Bitcoin exists as an immutable, fixed supply, digital, censorship-resistant, self-custodial, peer-to-peer money. Leaving one’s money with a fractional reserve entity who issues circulation credit would be seen as disproportionately risky in comparison to its possible loss by rational holders of money.

To state the obvious, our current monetary system does not even remotely resemble either of the above two scenarios.

To summarize, economic growth is the increased/easier production of real goods and services. Money is an abstract tool that facilitates multi-party trade. Creating money or circulation credit does not bring about more real-world resources which are required to fund new investments. It is more likely that the creation of money and circulation credit leads to economic destruction as it distorts the price signal, and interferes with the incentive to invest resources carefully. Even if the new money and circulation credit does lead to real economic growth, it’s a morally unjust arrangement, because 1) it is involuntarily funded by real savers, 2) the risk of loss is involuntarily placed on real savers, and 3) it often relies on government intervention to prevent fractional reserve entities from collapsing.

Fixed supply money leads to prices declining over time, which leads to hoarding money, which means lack of spending/investment, which means high unemployment and economic recessions.

It is certainly correct that a fixed supply of money would lead to prices declining over time, assuming that our society becomes better at producing goods and services. But would declining prices lead to “hoarding money”? And if so, would this cause mass unemployment and recessions?

The idea that declining prices leads to money hoarding is based on the idea that if people start to believe that prices will decline over time, they will defer their purchases because why would you buy something today when you can buy it a year from now at a lower price?!

Firstly, this ignores the reality that people prefer to have goods and services today vs one year from now. Further, if this line of thinking were true, there would have been a grand total of zero TVs or laptops sold in the past 20 years. By this logic, everyone would be perpetually waiting for TVs and laptops to get cheaper (and better quality) and the point of purchase would somehow never arrive. For more examples that show how absurdly wrong the idea is that falling prices would lead to hoarding money and lack of spending, consider parents faced with the decision of buying their children anything. It could be new shoes, clothes, healthy food, piano lessons, a week at summer camp, a bike, etc. Can you imagine a parent saying “I’m sorry honey, we’re not sending you to summer camp this year because we expect it to be 2% cheaper next summer”? Or how about “Sorry bud, I know you want those new shoes for the school year, but we won’t buy them for you because we expect them to be 5% cheaper next year. So we’ll buy them next year, unless we expect them to be cheaper the following year, in which case you’ll get them. uhh… never.”

There is also the obvious reality of life that humans will purchase food, transportation, and shelter (among many other basic necessities) regardless of what their expectations are for future price declines.

Sound money and declining prices do not lead to hoarding money, but rather to more thoughtful spending. The inverse of sound money — expansionary money and circulation credit — often results in prices increasing over time, which leads to frivolous, thoughtless spending as we realize our money will be worth significantly less in future years.

It is unjust that someone could see their purchasing power maintained or increased over time for “doing nothing” other than holding money.

This claim ignores how someone was able to hold money in the first place. Holding money requires that Alice produced something of value to others who were willing to compensate Alice with money. How did Alice find herself able to produce something of value? This can be done in many ways, but let’s say that Alice works for a company. How did she get there? Alice listened to her parents, she took her education seriously, she learned a skill, she marketed herself to productive companies, she competed for a job, she excelled at her job, and the company paid her for her work. And beyond that, in order to find herself holding money, Alice also must consume less than she earns. Those who support expansionary money and circulation credit gloss over the tremendous effort and achievement required to earn and save money. Instead, they want to add yet another task for Alice: she must become an investor in her free time. She must invest her hard earned money if she wants to even have a chance at maintaining her purchasing power.

Importantly, deferred consumption is how capital and wealth accumulates in the first place! If everyone consumed in equal proportions to what they produced, there would be no available resources which could be used to grow our material wealth in aggregate.

Deferred consumption is net positive for everyone in society, therefore we should absolutely incentivize people to defer consumption by offering a money which has the potential to appreciate and reward their positive choice. We want people to save because it provides more available capital to be used by entrepreneurs.

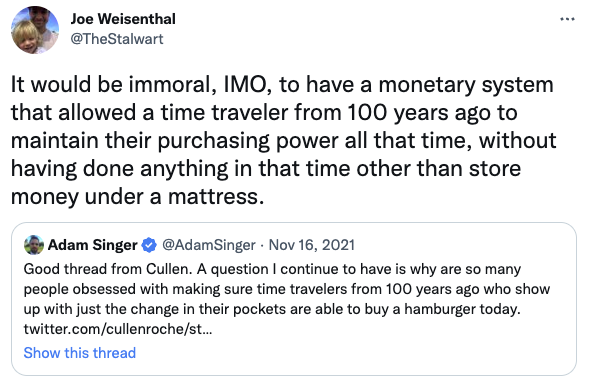

Joe Weisenthal is a perfect example of someone who holds the view that Alice must become not just a producer and a saver, but also an investor. Per his tweet below, he clearly states that he believes people should be required to do more than simply hold money in order to maintain their purchasing power.

Let’s take a moment to appreciate how rich it is that someone who works for Bloomberg and has constant access to the world’s most sophisticated financial data believes we should have a monetary system which requires people to become successful allocators of financial assets to protect their hard-earned purchasing power. Side note, for anyone who claims that Alice doesn’t need to invest the money herself, but rather she can pick a professional to invest her money for her, that logic does not work. This would require that Alice has the ability to pick a successful investment manager amongst all the available options, which also requires her to become a successful allocator of financial assets. Picking a successful investment manager is no easier than picking a successful investment directly.

The claims of people like Joe Weisenthal also fail to acknowledge a difference between saving and investing. Saving is storing wealth for purchasing a share of civilization’s future productivity. Investing is trying to grow the actual productivity of civilization, and it comes with the risk of complete loss.

Yes, successful investing should generate greater returns than savings due to the risk and work that goes into it. However, that does not mean that savings should generate negative returns. After all, saving money was historically and correctly seen as a prudent and responsible thing to do.

People who hold Joe’s belief also neglect the fact that one’s money can only grow in purchasing power if we have sound money and an increase in the production of goods and services in society. Someone has to produce the goods and services. The person who holds money already did their job. As discussed earlier, in order to find oneself in a position where they hold and save money, they had to first produce something of value and consume less than they earned. They were a net contributor to society’s material wealth.

Importantly, if we do not have sound money, we’re left with a system which results in continual debasement of our money, i.e. an extraction of purchasing power over time from those who hold money. Borrowers and recipients of the newly created money and circulation credit are rewarded at the expense of producers and savers.

We need an expansion of money and circulation credit to redistribute resources within society from the haves to the have-nots.

A discussion of redistribution often becomes quite subjective. And this topic is not meant to be the focus of this article.

With that said, the point here is that some may claim it is theoretically possible to use the monetary system to redistribute wealth from the haves to the have-nots. I understand there is a part of our human nature that wants to see wealth redistributed in this way. But the reality is that redistribution via the monetary system would be centralized, coercive, economically destructive, and prone to capture by bad actors. It leads to far more harm than good.

History has shown us time and time again that centralized actions with collectivist motivations have the best chance of succeeding when they are enacted within very small groups of humans. Alternatively, centralized actions with collectivist motivations often go horribly wrong when attempted on large groups of humans.

Today’s monetary system is a real time example of this. It has become clear to many that today’s system actually redistributes wealth to the haves and from the have-nots. Owners of financial assets see their wealth grow substantially almost every year, while those who simply work and earn a salary find they cannot save and cannot keep up with increasing prices and continued currency debasement.

“We can use the monetary system to fairly redistribute wealth” is another version of “we just haven’t tried real communism yet.”

We need an expansion of money and circulation credit to “stimulate” our economy during times of recession.

This is ultimately a claim that giving centralized entities (including banks and politicians) control of society’s resources will somehow end recessions faster than otherwise. As discussed earlier, the creation of money and circulation credit out of thin air does not change the amount of resources that exist, but simply changes who controls them. The argument ultimately boils down to “Trust me bro, if we let the banks and politicians control our resources, we’ll get out of this recession faster.” If that were the case, shouldn’t we always leave them with control of society’s resources, not just during recessions? Note that leading Modern-Monetary Theory economist Stephanie Kelton asks the same question, and her resounding answer is that we should.

Furthermore, the last two decades have indicated that emergency bailouts from governments and central banks have created bubbles in alternating industries. First tech, then housing, then sovereign debt. Each “stimulation” of the economy ends up transferring the bubble to a new asset class and increasing the leverage in the system.

By choosing increased leverage over natural economic contractions, the system becomes more volatile and fragile. A highly comparable analogy is forest fires. If you never allow forests to burn, you end up creating mega fires. If you never allow economies to contract naturally you end with increased leverage, volatility, and fragility.

One additional critique of sound money involves claiming that our current system is so dependent on expansionary money and circulation credit that it would be an incredibly messy transition to a world of sound money. This is another topic altogether. I am not making the claim that it would be beneficial for us to move to a world of sound money in a matter of days, with all short-term negative consequences being damned. But managing the transition is a secondary point which can only be discussed after there is agreement about which system we should be transitioning towards. The answer is clearly that sound money is the only intellectually and ethically defensible system. Once that becomes understood, we can discuss how the transition can and should occur.

Money is an abstract tool we use to facilitate multi-party indirect exchange. This allows us to experience significantly better production of goods and services than otherwise possible, including the creation of entirely new products and industries. The creation of new money/credit does not lead to more real-world abundance any more than a declaration of there being more than 12 inches in one foot would lead to more houses being built.

The creation of new money and circulation credit is most likely to lead to economic destruction due to its distortion of the price signal, and the defective incentive structures that it creates.

It’s possible that new money or circulation credit is created and given to people who ultimately use it to produce more real-world wealth. However, this does not change the fact that the creation of the money and circulation credit was funded by the confiscation of wealth of pre-existing money holders (i.e. savers) who did not have a say in the matter, and were made to bear the risk of something going wrong without being informed of the risk or being compensated for it.

There is no getting away from the fact that any purchasing power/consumption/ spending/investment must be preceded by production and savings. This is true at a level of physical reality — you cannot consume that which has not been produced. It is either funded directly and honestly by savers who voluntarily contribute their savings, or it is funded indirectly and dishonestly by confiscation from savers via the creation of money and circulation credit.

People do not hoard money simply because prices decline over time. And even if you felt that someone’s lack of spending should be deemed “hoarding money, ” in order to have any money to “hoard” in the first place, it means they already produced a surplus.

Seeing some sort of redistribution in society might feel like a worthy goal to many people, but doing this in a centrally planned and coercive manner via the monetary system keeps resulting in tremendous negative consequences, both economically and societally.

With all this said, we can next turn our attention to an honest exploration of how real-world conditions would likely play out in a fixed supply money system, including how they would drastically differ from our current system — a topic for a future article I hope to write.

Buy automatically every day, week, or month, starting with as little as $10.

John is the Managing Director of Private Client Services at Swan Bitcoin. He previously spent 13 years on Wall Street, where he was a Portfolio Manager and Insitutional Investor at Goldman Sachs.

If you’d like to learn more about the Bitcoin network and protocol function, you can download Inventing Bitcoin by Yan Pritzker for FREE!

News

More NewsThoughts on Bitcoin from the Swan team and friends.

Is Bitcoin safe for generational wealth? Learn why custody, inheritance planning, and patience matter more than price when building lasting family wealth with Bitcoin.

Bitcoin estate planning is the most under-addressed risk in HNW portfolios. Why holders and their CPAs, attorneys, and trustees keep missing it, and how to close the gap.

Audio narration