Lyn Alden’s Broken Money

Broken Money explores the history of money through the lens of technology. Politics can affect things temporarily and locally, but technology is what drives things forward globally and permanently.

Broken Money explores the history of money through the lens of technology. Politics can affect things temporarily and locally, but technology is what drives things forward globally and permanently.

From papyrus-based bills of exchange to double-entry booking and paper banknotes, the main purpose of banking was to enable transactions to move more quickly and frequently than the transportation and verification of physical gold would allow. Banking also allowed for the usage of more extensive credit systems, by allowing a third party (a money changer or a bank) to serve as a trusted intermediary between two non-trusting entities (buyers and sellers, or creditors and debtors).

In other words, banking allowed for transactions (commerce) and settlements (money) to be separated. Transactions for individual goods and services could occur more frequently, existing for a period of time in a state of credit, until they were settled with precious metals in less frequent occurrences and in larger amounts. However, while this process of batching multiple transactions into fewer and larger settlements increased transaction efficiency and reduced the risk of theft, it couldn’t overcome a fundamental constraint: the speed of information.

For thousands of years, transactions and settlements had the same maximum speed limit: the speed of foot, horses, and ships. Peoples’ ability to do transactions, and the bearer assets they transacted with (mainly gold and silver in advanced regions), had no inherent difference in terms of travel speed, although the transactions themselves were more efficient in practice. All of it was limited by the speed of physical human travel.

Even the invention of banking couldn’t get around this basic limitation. The paper bills of exchange and banknotes, while easier and safer to transport than gold, still couldn’t move faster than foot, horses, and ships. Ledger-based account systems, while convenient, still couldn’t send information over long distances any faster than the existing modes of physical travel.

However, with the invention of the telegraph, and then the telephone, the speed of transactions increased to nearly the speed of light. The first working telegraph was invented in the 1830s. Engineers then spent much of the 1840s and 1850s figuring out how to run cables over long distances, including under large bodies of water, during which time they were able to connect the various financial centers of Europe together, including London and Paris. After some failed attempts, the first long-lasting transatlantic telegraph cables were put in place in the 1860s, and the global banking system quickly became more interconnected in the decades that followed.

From that point, people could transact across the world by updating each other’s bank ledgers over telecommunication systems nearly at the speed of light. Banks and central banks had full control over that process. Meanwhile, gold and silver as bearer assets still moved slowly, and thus had to be increasingly abstracted to keep up.

Prior to the invention and usage of telecommunication systems, gold and silver were already frequently abstracted with paper claims due to divisibility limitations or security concerns or convenience or the desire to earn interest as described in prior chapters, but once telecommunication technology was invented, their slow speed made it even more necessary to abstract them to keep up. All around the world, people and institutions increasingly relied on interconnected bank accounts rather than coinage. And with currency units abstracted from the underlying metal, it turned currency units into an inherently political topic between creditor groups and debtor groups.

In his 1875 book Money and the Mechanism of Exchange, which was published less than 25 years after the telegraph connection between the United Kingdom and France, and less than a decade after the completion of the transatlantic telegraph connection, the English economist and logician William Stanley Jevons described in detail the increasing centralization of the global financial system. He discussed the inherent challenges of physical coinage and bullion, including their various imperfections, inefficiencies, and the complexities of authentication, and how increasingly centralized financial centers were becoming more and more efficient at performing abstract transactions so that gold and silver diminished in their day-to-day roles.

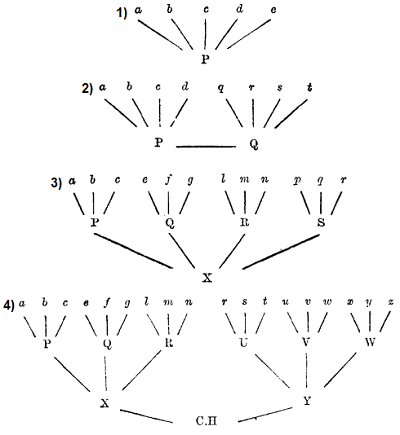

In that book, Jevons provided four separate diagrams (now in the public domain) shown together below to walk the reader step-by-step through an increasingly connected set of hypothetical banks and how this centralization was occurring over time.

The first diagram showed how account holders of a single bank could send money to each other using the bank as a settlement layer.

The second diagram showed a connection between two such banks, who accept each other’s paper payment instruments so that their accountholders can easily send money to each other across banks as well.

The third diagram showed the introduction of a central bank, which allowed for more efficient settlement between many banks.

The fourth diagram showed a base layer clearing house, either at a national scale or even a global scale centered in a major financial hub like London, to connect all banks.

Throughout the book, Jevons excitedly described the increasing abstraction and efficiency of global commerce, as claims for payment could cancel out against other claims between banks and therefore render gold settlements rare and almost irrelevant. And toward the end of the book in a section called “The World’s Clearing House”, he described London’s increasing role as the centralized ledger administrator for the world. Banks from across the whole world had offices in London to connect with the financial network effects that existed there:

England buys every year from America a great quantity of cotton, corn, pork, and many other articles. America at the same time buys from England iron, linen, silk, and other manufactured goods. It would be obviously absurd that a double current of specie should be passing across the Atlantic Ocean in payment for these goods, when the intervention of a few paper acknowledgments of debt will enable the goods passing in one direction to pay for those going in the opposite direction. The American merchant who has shipped cotton to England can draw a bill upon the consignee to an amount not exceeding the value of the cotton. Selling this bill in New York to a party who has imported iron from England to an equivalent amount, it will be transmitted by post to the English creditor, presented for acceptance to the English debtor, and one payment of cash on maturity will close the whole circle of transactions. Money intervenes twice over, indeed, once when the bill is sold in New York, once when it is finally cancelled in England; but it is evident that payment between two parties in one town is substituted for payment across the whole breadth of the Atlantic. Moreover, the payments may be effected by the use of cheques, or the bills when due may themselves be presented through the Clearing House, and balanced off against other bills and cheques. Thus the use of metallic money seems to be rendered almost superfluous, and, so long as there is no great disturbance in the balance of exports and imports, foreign trade is restored to a system of perfected barter.

[…]

It might seem that in the use of cheques internally, and of bills of exchange in foreign trade, we have reached the climax in the economy of metallic money; but there is yet one further step to make. We found that so long as all the merchants of a town keep their cash with the same banker, they have no need to handle the money at all, but can make payments by transfers in the books of their banker. Let us imagine, then, that merchants all over the world agreed to keep their principal accounts with the bankers of any one great commercial town. All their mutual transactions could then be settled among those bankers. An approximation to such a state of things exists in the tendency to make London the monetary head-quarters of the commercial world, and the general clearing house of international transactions. All that is needed to secure economy of money is centralization of transactions, so that there may be the wider scope for the balancing of claims.

Jevons’ book is remarkable in two ways.

Firstly, it was excellent at describing the increasing role of technology as it relates to money, from ancient times until its publication in 1875, and how the next few decades would likely come together in even more centralized ways.

Secondly, it was prescient at identifying some of the catastrophic problems that such a centralized system could lead to, even though Jevons himself was highly supportive of this centralization for the sake of efficiency and thought that those problems could be managed appropriately.

Specifically, in a series of instances throughout the book, Jevons identified the greater and greater number of claims for gold relative to the amount of actual gold in the system, due to the ease of dealing with claims rather than the metal itself. He cited numbers from his time showing that a mere four to seven percent of claims were held in reserves by the banking system of the United Kingdom, and that even those reserves were themselves fractional claims for gold:

It is requisite, too, that our bankers, financiers, and merchants should regulate their operations with a thorough comprehension of the immense system in which they play a part, and the risks of derangement and failure which they encounter by over-severe competition. No one doubts that alarming symptoms have during recent years presented themselves in the London money market. There is a tendency to frequent severe scarcities of loanable capital, causing sudden variations of the rate of interest almost unknown thirty years ago. I will therefore in the next chapter offer a few remarks intended to show that this is an evil naturally resulting from the excessive economy of the precious metals, which the increasing perfection of our banking system allows to be practised, but which may be carried too far and lead to extreme disaster.

[…]

The metals took the place of other commodities as currency, and delicate considerations began to enter concerning token and standard coins. From metallic representative money, we passed to paper representative money, and finally discovered that, by the cheque and clearing system, metallic money was almost eliminated from the internal exchanges of the country. Pecuniary transactions now present themselves in the form of a room full of accountants, hastily adding up sums of money. But we must never forget that all the figures in the books of a bank represent gold, and every creditor can demand the payment of the metal. In the ordinary state of trade no one cares to embarrass himself with a quantity of precious metal, which is both safer and more available in the vaults of a bank. But in international trade, gold and silver are still the media by which balances of indebtedness must be paid, and serious consequences may arise from any disproportion between the amount of transactions carried on, and the basis of gold upon which they are settled.

[…]

It is quite apparent, therefore, that the tendency is to carry on a greater and greater trade upon an amount of metallic currency which does not grow in anything like the same proportion. The system of banking, too, grows more perfect in the sense of increasing the economy with which money is used. The competition of many great banks, leads them to transact the largest possible business with the smallest reserves which they can venture to retain. Some of these banks pay dividends of from 20 to 25 per cent, which can only be possible by using large deposits in a very fearless manner. Even the reserves consist not so much of actual coins or bank-notes in the vaults, as of money employed at call in the Stock Exchange, or deposited in the Bank of England, which again lends the deposits out to a certain extent.

Now the larger the trade which is carried on, the larger will be the occasional demand for gold to make foreign payments; and if the stock of gold kept in London be growing comparatively smaller and smaller, the greater will be the difficulty in meeting the demand from time to time. Such is, I believe, the whole secret of the growing instability and delicacy of the money market in this country. There is a larger and larger quantity of claims for gold, and comparatively less gold to meet them, so that every now and then there is a natural difficulty in paying claims, and the rate of interest has to be suddenly raised to induce those who have gold to lend it, or to induce those who were demanding it to forego their claims for a time.

[…]

Mr. R. H. Inglis Palgrave, in his important “Notes on Banking, ” published both in the Statistical Journal, for March, 1873 (Vol. xxxvi. p. 106), and as a separate book, has given the results of an inquiry into this subject, and states the amount of coin and Bank of England notes, held by the bankers of the United Kingdom, as not exceeding four or five per cent. of their liabilities, or from one twenty-fifth to one twentieth part. Mr. T. B. Moxon, of Stockport and Manchester, has subsequently made an elaborate inquiry into the same point, and finds that the cash reserve does not exceed about seven per cent. of the deposits and notes payable on demand. He remarks that even of this reserve a large proportion is absolutely indispensable for the daily transactions of the bankers’ business, and could not be parted with. Thus the whole fabric of our vast commerce is found to depend upon the improbability that the merchants and other customers of the banks will ever want, simultaneously and suddenly, so much as one-twentieth part of the gold money which they have a right to receive on demand at any moment during banking hours.

The more and more efficient the global banking system became at netting and clearing imbalances, the less and less it needed metal as a proportion of transactional volumes and saving volumes during the normal course of operation. And consumers happily went along with it as well, due to the greater ease that it provided them with. And yet this increasing efficiency is precisely what allowed it to become so unbacked and unstable at its foundation. The disinclination of most people to want to withdraw and secure the cumbersome physical metals allowed for the extreme proliferation of gold claims relative to the amount of actual gold.

By the early 20th century, thanks to this extreme degree of monetary abstraction and the associated ease of claim creation for World War I approximately four decades after Jevons’ book, the global gold standard collapsed and never recovered. In the decades after that, governments eventually dropped gold and silver backing from their financial systems entirely, and that’s how we eventually got to this world of 160 different inflationary fiat currencies — each with a local monopoly in their respective jurisdiction. The difference in speed between transactional commerce and bearer asset commodity money gave governments and banks a huge opportunity for custodial arbitrage. A centralized and globally interconnected banking system with a monopoly on fast long-distance transfers of value became too powerful and convenient for gold to keep up with, even if gold could still make for better private savings. The introduction of credit cards in the 1950s, e-commerce in the 1990s, and smartphone-based payments in the 2010s further cemented the importance of fast telecommunication-based payments.

This is the only time in history where, on a global scale, a weaker money won out in terms of adoption over a harder money. And it occurred because telecommunication systems introduced speed as a new variable into the competition.

Gold, with its inherently slow speed of transport and authentication, couldn’t compete with the pound, the dollar, and other top fiat currencies with their combination of speed and convenience, despite gold being in scarcer supply. The combination of legal tender laws, taxation authority, and greater speed has allowed fiat currencies to outcompete their slower but scarcer precious metal counterparts all over the world in terms of usage.

This mismatch or gap in speed has been a foundational reason for the greater and greater levels of financialization that the world has seen over the past century and a half. Monetary ledgers became increasingly detached from any sort of natural constraint or scarce units of settlement, because the only scarce monetary alternatives such as gold were too slow to present a complete alternative.

Barry Eichengreen, in his book Globalizing Capital, pointed out that the international central bank gold standard as we know it began in the 1870s. This was right around the time of Jevons’ book quoted above. Prior to that, there were frequent uses of bimetallic standards and free banking systems. In the gold standard framework, central banks in Europe held gold, issued currency against that gold (which was fractionally reserved), and used the combination of telecommunication systems and bank ledger divisibility to create a rather fast-moving and convenient set of globally interconnected ledgers. The United States increasingly joined them as well, formally with the Coinage Act of 1873 and the Gold Standard Act of 1900.

The rise of the credit theory of money in its various forms, also coincided with these technological developments in the second half of the 19th century. As currency claims or IOUs moved around the world at the speed of telecommunication, within a highly efficient globally connected banking system, many monetary theorists began to wonder, “why do we even need these metals?”

In 1905, Georg Friedrich Knapp published The State Theory of Money which described and founded the monetary theory known as Chartalism. This school of thought was a precursor to what is now known as Modern Monetary Theory and argued that money originated with states’ attempts to direct economic activity, and that rather than commodities giving money value, the state gives money value due to the imposition of tax IOUs on the public that only the state’s money can satisfy.

In his influential 1914 essay “The Credit Theory of Money”, Alfred Mitchell-Innes highlighted the writings of Henry Dunning Macleod from the late 1850s to the 1890s as the original formulator of the credit theory, and elaborately made the case that money had nothing to do with metal. I don’t view it as coincidental that these theories by Macleod, Knapp, Mitchell-Innes, and others were developed and rose in prominence as telecommunication-based ledgers increasingly became the norm. As Mitchell-Innes wrote:

The present writer is not the first to enunciate the Credit Theory of money. This distinction belongs to that remarkable economist H. D. Macleod. Many writers have, of course, maintained that certain credit instruments must be included in the term “money”, but Macleod, almost the only economist known to me who has scientifically treated of banking and credit, alone saw that money was to be identified with credit, and these articles are but a more consistent and logical development of his teaching. Macleod wrote in advance of his time and the want of accurate historical knowledge prevented his realizing that credit was more ancient than the earliest use of metal coins. His ideas therefore never entirely clarified themselves, and he was unable to formulate the basic theory that a sale and purchase is the exchange of a commodity for a credit and not for a piece of metal or any other property. In that theory lies the essence of the whole science of money.

But even when we have grasped this truth there remain obscurities which in the present state of our knowledge cannot be entirely eliminated.

What is a monetary unit? What is a dollar?

We do not know. All we do know for certain — and I wish to reiterate and emphasize the fact that on this point the evidence which in these articles I have only been able briefly to indicate, is clear and conclusive — all, I say, that we do know is that the dollar is a measure of the value of all commodities, but is not itself a commodity, nor can it be embodied in any commodity. It is intangible, immaterial, abstract. It is a measure in terms of credit and debt.

Some economists such as Saifedean Ammous have argued that from a monetary perspective, World War I never really ended once it began in 1914. In prior wars throughout history, wars had to be funded with savings or taxes or very slow debasement of coinage. Physical coinage held by citizens could usually only be debased by their government gradually rather than diluted instantaneously, because a government couldn’t just magically change the properties of the coins that were held by households; it could only debase them over time by taxing purer coins, issuing various decrees to try to pull some of those purer coins in, and spending debased coins back out into the economy (and convincing initial recipients to accept them at the same prior value, despite the lesser precious metal content, which would only work for a time and might not even be noticed at first). However, with the widespread holding of centrally issued banknotes and bank deposits that were redeemable for specific amounts of gold, governments could change the redemptive value with the stroke of a pen or eliminate redemption all together.

This gave governments the power to instantaneously devalue a substantial part of their citizens’ savings, literally overnight, and funnel that purchasing power toward war or other government expenditures whenever they determine that the situation calls for it.

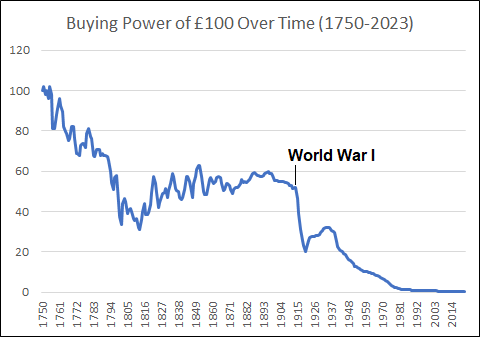

The pound sterling of the United Kingdom is the world’s oldest continuously used currency that is still in use today. In Anglo-Saxon England during the eighth century, the pound sterling was defined as a pound of silver. The definition of a pound back then differed slightly compared to its definition today, and so it was equal to about three-quarters of what we currently define as a pound. Over the next nine centuries, the pound sterling was gradually debased, and lost more than two-thirds of its value by the beginning of the 18th century.

That’s quite a slow debasement rate, equal to less than 0.15% compounded debasement per year on average over the course of centuries, although it tended to occur in small stepwise bursts from time to time. By the 1800s, Britain had switched to a gold standard and maintained it until the early 20th century. It wasn’t until World War I, when the pound sterling was completely decoupled from precious metals, that the pound rapidly devalued and lost almost the entirety of its value within one or two human lifetimes. Today a pound sterling is worth less than two grams of silver.

Even when we include the gradual expansion of the supply of precious metals and the proliferation of credit, the sheer magnitude of currency debasement that happened in the first major war of the telecommunication age, and that continues to occur, is at a whole different level than was previously the norm.

Ian Webster, officialdata.org

The 20th century and the beginning of the 21st century have been defined by a greater role of nation states, financed by their flexible ledgers.

On one hand, this has allowed for centralized and widespread social safety net implementations, but they tend to be popular enough that they could be financed more transparently in some form or another through taxation.

On the other hand, this has allowed for constant warfare and selective bailouts around the world by diluting the savings of others in continuous and non-transparent ways. Corporations can cozy up to governments, and shape legislation that determines where public deficit spending goes, with that spending being opaquely drawn out of peoples’ savings through ongoing debasement.

Although above-ground gold increases in supply by approximately 1.5% per year on average, the broad money supplies of most major countries have grown at an annualized rate of between 6% and 12% since 1960, while the long tail of developing country currencies generally grew at double-digit rates or outright hyperinflated at some point within the period.

As a result, people around the world have repeatedly seen their savings debased, especially in developing countries, and for most of this time they have not had an alternative. Gold can still be stored as a long-term niche asset for savings and jewelry, but due to its slow speed and lack of widespread acceptance in modern times — along with legal tender laws — gold is not a viable alternative to the global fiat currency system for payments, unless heavily abstracted via trusted counterparties. People often must interact with fiat banknotes and centralized banking system deposits on a regular basis if they wish to make and receive payments in our digital and globally connected world.

Many critics of central banking or government monetary policy frame the departure from the gold standard as a moral failing: “If only the government had maintained the gold standard, things would be better, ” summarizes many of their positions. Or to go back further, many will assert, “if only fractional reserve banking had never been used, we’d have a more honest and sustainable financial system.”

However, while I sympathize with those views and I personally would like money to hold its value, I see things differently, and mainly through the lens of technological inevitability based on the gap in speed between transactions and settlements that widened over time. People shifted over to transacting in fast gold claims and didn’t withdraw gold frequently enough to keep the number of claims “honest.” Therefore, the number of claims proliferated far faster than gold, and then gold was abandoned by governments to keep those claims in circulation. And it happened everywhere.

Out of nearly 200 countries in the world as of this writing, none of them use a gold standard. Switzerland was the longest remaining country on a gold standard, having dropped their gold standard in 1999. In most of the world it was gone far earlier during the 20th century.

Something that existed in the past but does not exist anywhere in the present likely has a lack of fitness. The gold standard’s weak incentive structure along with the slow speed of gold itself hasn’t allowed the gold standard to exist in any form in the modern era. It became too easy for every country in the world to discard it, and so they did. And to the extent that people want to hold more scarce forms of illiquid savings than currencies, they now turn to real estate or corporate equities more-so than they turn to gold. Gold’s primary role has been reduced to being a non-correlated portfolio asset among many others, and to serve as a form of macroeconomic disaster insurance due to its ability to be physically possessed by the holder with a high ratio of value to size and weight.

If we were to run this period of human development back a hundred times, I think almost every time we would end up in a similar place in terms of money, due to the path dependence of technological development itself. Once telecommunication systems were invented, bank-controlled ledgers dominated, and this gave nearly unassailable monetary power to the banks and central bankers that ran those ledgers.

In order to move money quickly, people and banks came to rely on their country’s central bank as the underlying ledger, and in an international context, various countries also came to rely on the central bank ledger of the world reserve currency issuer, which was the United Kingdom at the start of the telecommunication age and then shifted over to the United States in the 20th century.

Political decisions affect things locally and temporarily, while technological changes affect things globally and permanently. Every single government, whether authoritarian or democratic, has moved toward a fiat currency system, and has been debasing their unit of account at an accelerated rate. Due to the slow speed of transporting and authenticating gold, full-reserve banks inevitably turned into fractional reserve banks to tap into the arbitrage that this speed gap between gold and bank deposits provided. By making use of the fact that people rarely withdrew their gold, they built inherently unstable systems that work “most of the time” but occasionally required bailouts when they did not.

From there, fractional reserve banks inevitably became centralized by their governments and globally interconnected with telecommunication systems, and then the underlying metals were dropped from the backing by governmental decree when the governments no longer wished to be constrained by them.

Each time, in every jurisdiction, users of the currency went along with the transition and accepted it over the course of decades. Even when fiat currencies fail in a country, people in that country tend to turn to a newly issued fiat currency or use another country’s fiat currency — such as dollars — rather than falling back to gold as a medium of exchange.

Nature’s ledger (gold) has robust parameters for supply and debasement but doesn’t move and get verified fast enough in the telecommunication age. Mankind’s ledger (the dollar) moves and gets verified fast enough but doesn’t have robust parameters for supply and debasement. The only way to fix this speed gap in the long run would be to develop a way for a widely accepted, scarce, monetary bearer asset itself to also be able to settle over long distances at the speed of light. That’s one of the major reasons why the discovery of digital scarcity and the invention of Bitcoin is so significant.

Broken Money is now available on Amazon, and provides a thorough but accessible account of the past, present, and possible future of money. Lyn’s goal is for the reader to walk away with a deep understanding of money and monetary history, both in terms of theoretical foundations and in terms of practical implications.

Broken Money explores the history of money through the lens of technology. Politics can affect things temporarily and locally, but technology is what drives things forward globally and permanently.

Hold your IRA with the most trusted name in Bitcoin.

Lyn is an investment strategist at Lyn Alden Investment Strategy. She holds bachelor’s degree in electrical engineering and a master’s degree in engineering management, with a focus on engineering economics and financial modeling. Lyn has been performing investment research for over fifteen years in various public and private capacities.

News

More NewsThoughts on Bitcoin from the Swan team and friends.

Is Bitcoin safe for generational wealth? Learn why custody, inheritance planning, and patience matter more than price when building lasting family wealth with Bitcoin.

Bitcoin estate planning is the most under-addressed risk in HNW portfolios. Why holders and their CPAs, attorneys, and trustees keep missing it, and how to close the gap.

Learn how Bitcoin wealth management works, from custody and security to inheritance planning and liquidity. Discover how families and businesses use Bitcoin to build and protect long-term wealth.