Swan Bitcoin Market Update #40

This Insight Report was originally sent to Swan Private clients on October 13th, 2023. Swan Private guides corporations and high net worth individuals globally toward building generational wealth with Bitcoin.

In healthcare, a medical professional learns that an elevated resting heart rate is typically not a good sign, often indicating trouble brewing under the surface. It can occur for different reasons including cardiovascular disease, increased stress/anxiety, lack of sleep, smoking, as well as an adverse side-effect of several prescription medications. If left untreated, a high resting heart rate can lead to serious health complications such as heart attack, stroke, and even death.

To put it simply, a high resting heart rate means a person’s heart is working too hard. This puts strain on the rest of the system until something eventually breaks. When I look at the state of the economy today, I see a system with a high resting heart rate.

This Insight Report was originally sent to Swan Private clients on October 13th, 2023. Swan Private guides corporations and high net worth individuals globally toward building generational wealth with Bitcoin.

At a time when the Federal Reserve is desperately trying to crush demand in the economy, it continues to run hot. Annual GDP growth is running above its historical average, inflation remains elevated, consumer spending appears robust, and the labor market remains tight. When combined, these data points give credence to the notion that the economy is strong.

Further evidence of this could be found in the bond market. A strong economy is one plausible reason why bond yields may be climbing. At least that’s what U.S. Treasury Janet Yellen likes to think:

“I see the higher yields as certainly an important reflection of the stronger economy.” — Janet Yellen

But is this spike in yields a sign of a strong economy or an unhealthy one? I would argue that this economy is acting more like a patient with a high resting heart rate who has become addicted to stimulative cheap money, and despite the worrying symptoms, the government continues to prescribe more and more medication to keep the economy upright.

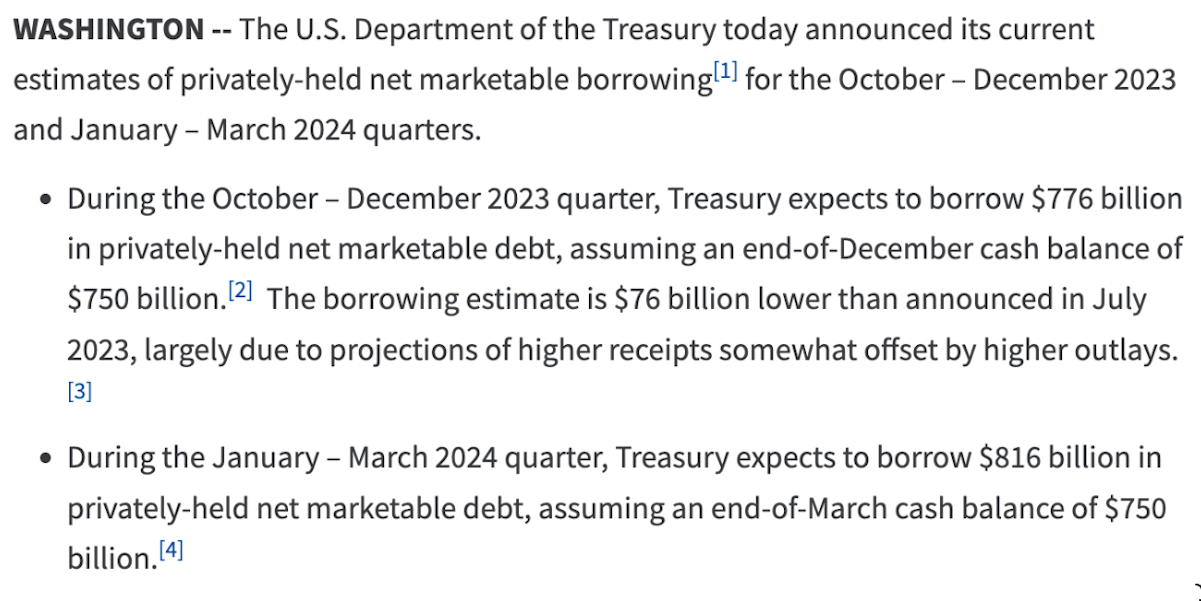

This week, the Treasury announced that it expects to borrow $1.6 trillion in the next 6 months. That puts it on pace to run over a $3 trillion deficit in the next 12 months!

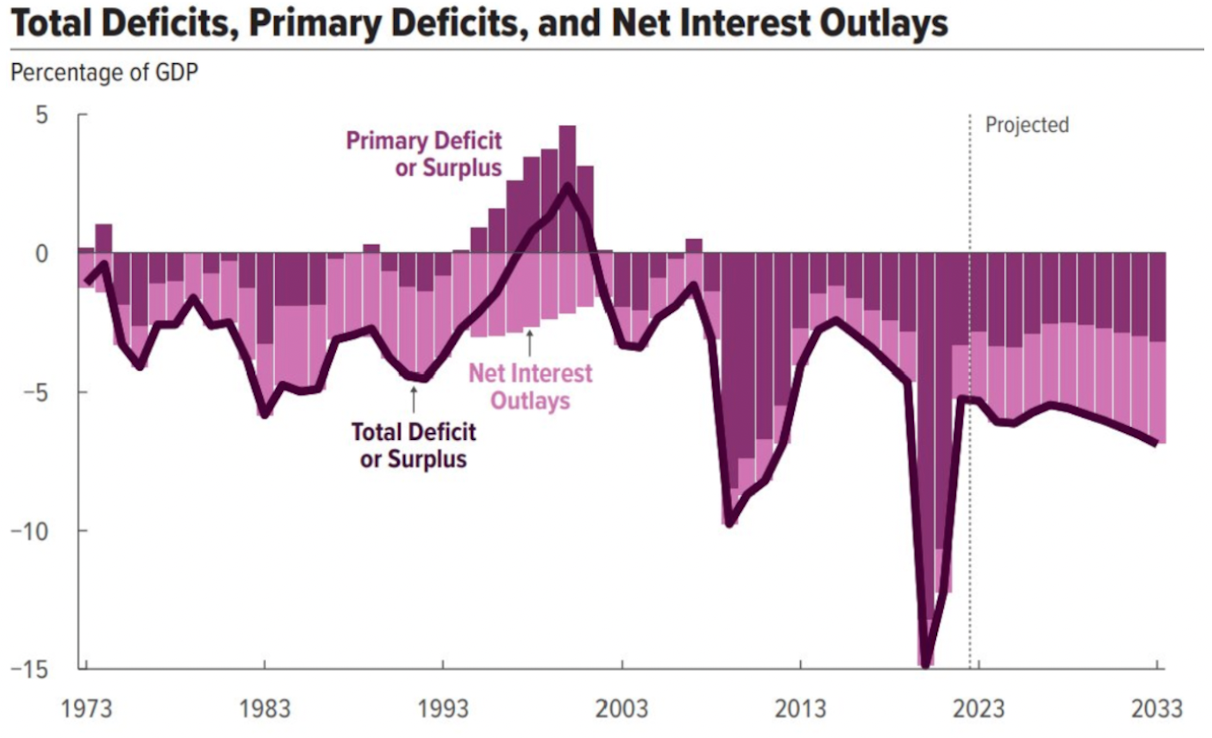

This extreme fiscal spending isn’t expected to stop anytime soon. CBO projections show that deficit spending is expected to be around 5% of GDP and continue to grow for the foreseeable future.

CBO

With deficits running consistently greater than 5%, it is difficult to see inflation coming down to pre-pandemic levels anytime soon.

This may help explain why long-dated bond yields have been rising. Investors might be concluding that a sustained period of elevated inflation makes bonds less attractive and, as such, they are demanding a higher yield for the risks of holding a long-dated Treasury bond.

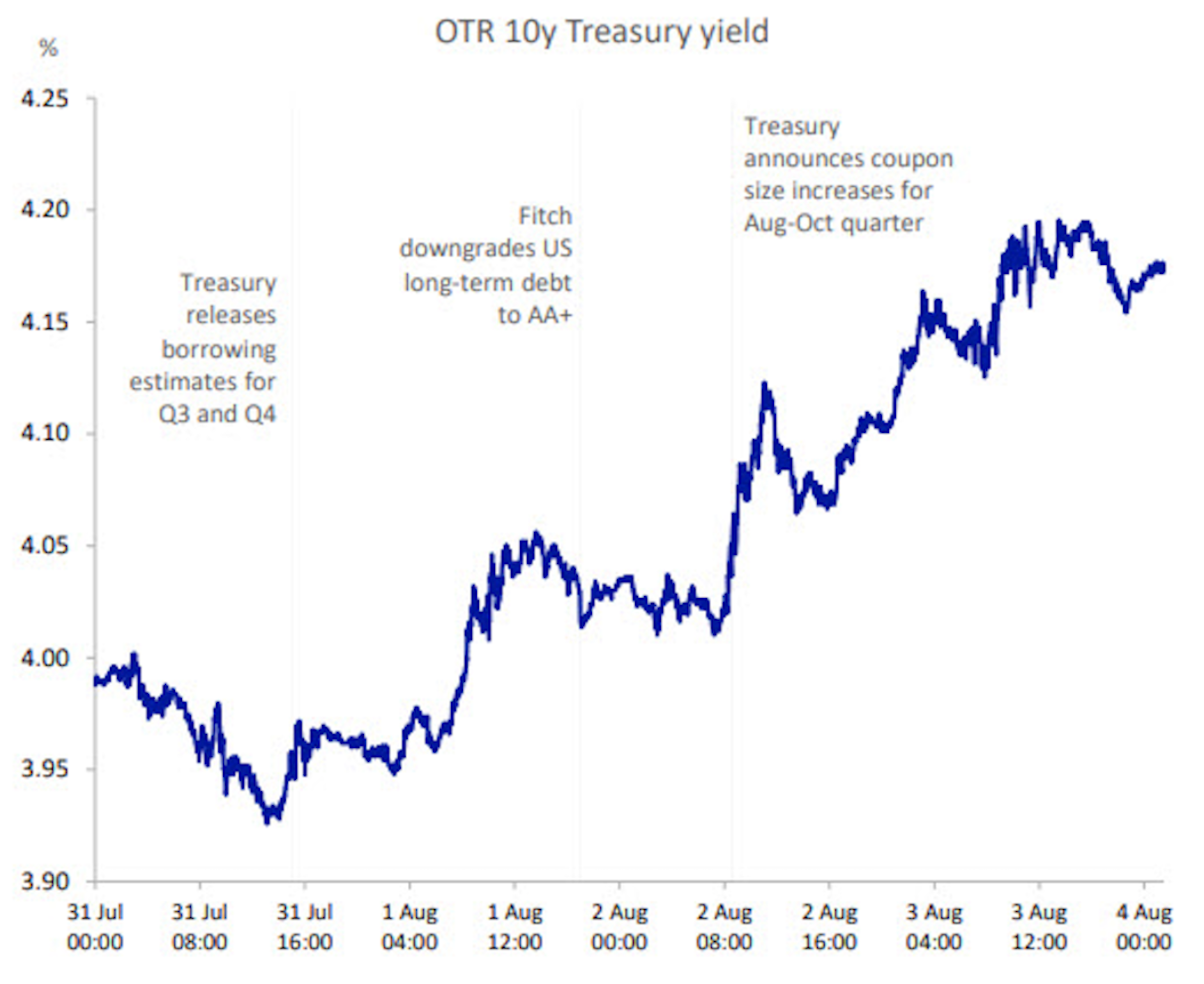

There are now increased concerns that the Treasury will need to continue to flood the bond market with new supply to finance bigger and bigger budget deficits.

This tracks with how we have seen yields move in response to news related to the US’s fiscal picture. Below, you can see how the 10-year Treasury yield has increased when new developments come to light.

TBAC

Market participants are beginning to understand that the Fed is no longer in the driver’s seat here; the Treasury is.

It leads to the question that if bond rates continue to rise as investors demand a higher yield for holding long-term Treasury bonds due to fears of elevated inflation and ongoing large fiscal deficits, how will bonds provide the portfolio diversification they once did?

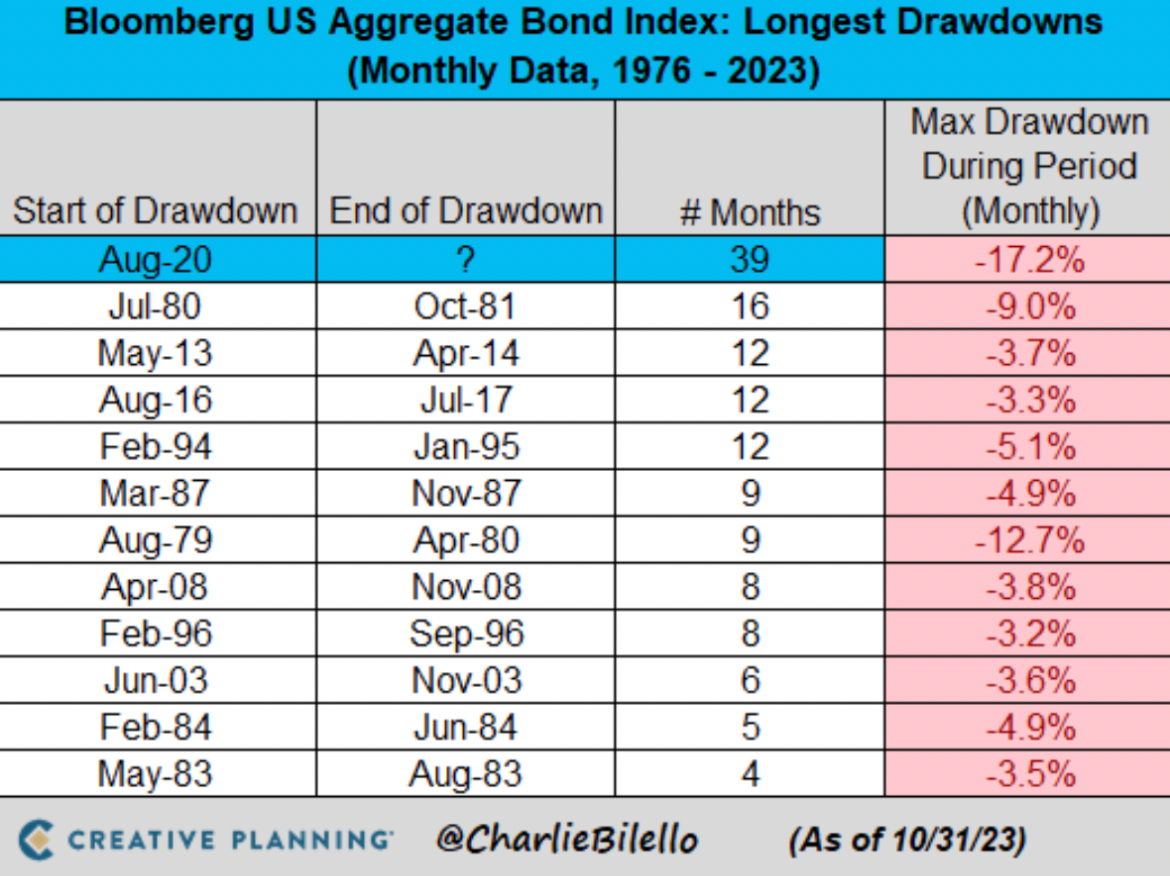

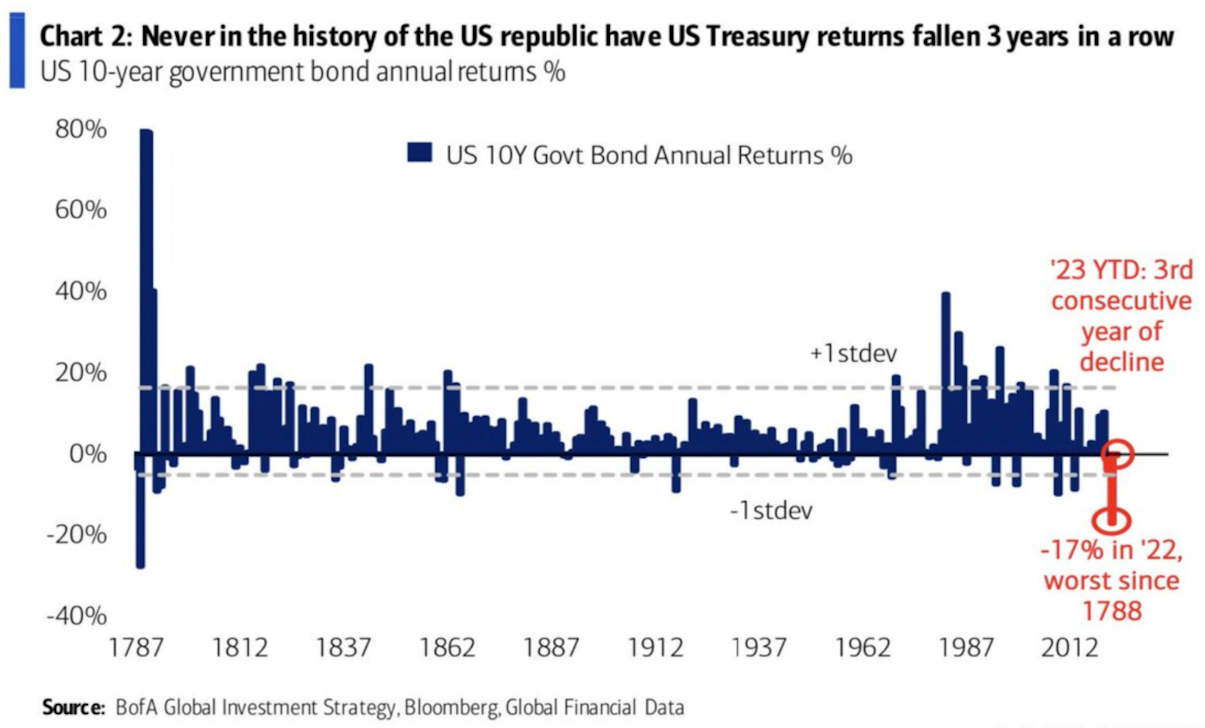

In this period of rising interest rates and multi-decade high inflation, bonds are currently experiencing the longest and steepest bear market in the last 40 years.

Treasury bonds are on pace to have their third consecutive losing year for the first time in history.

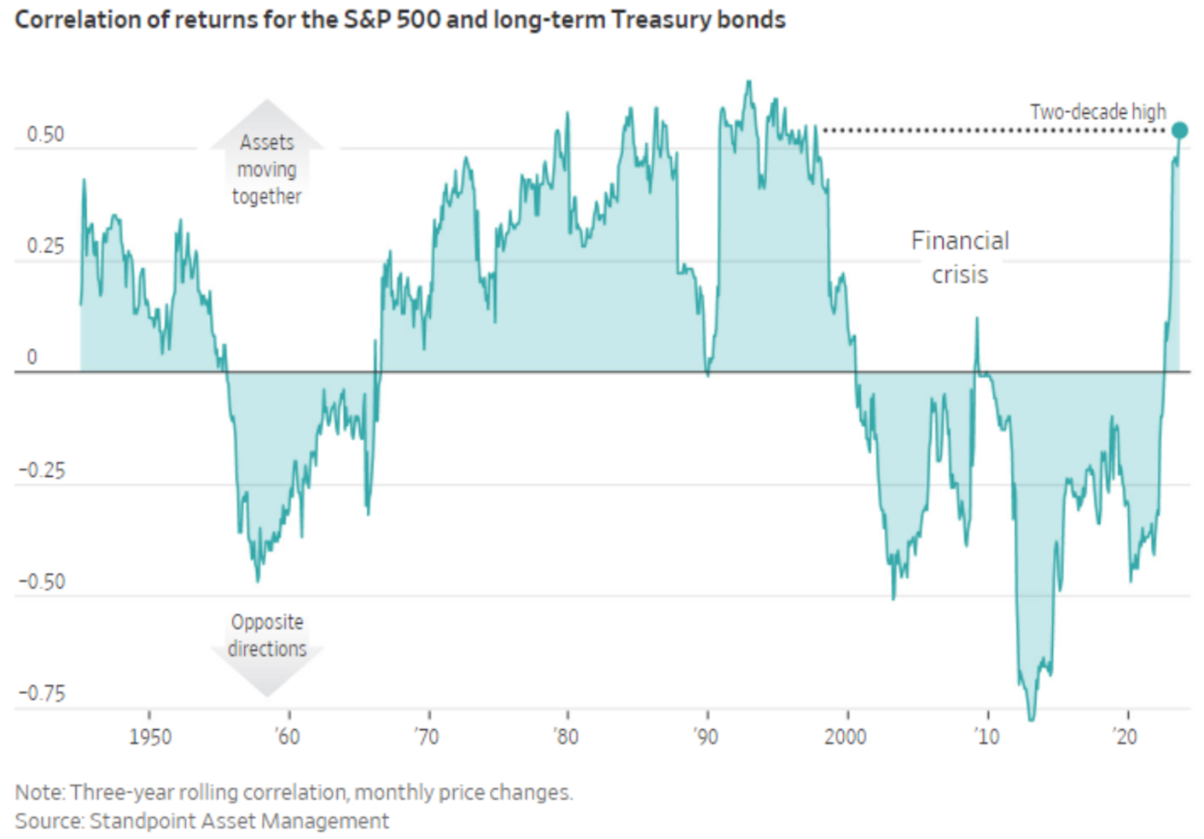

But what’s really scary is that bonds and stocks have fallen together over the last quarter. Over the last couple of years, we have seen the relationship between stocks and bonds change.

For the last 20 years, bonds have not only acted as a “shock absorber” for portfolios, rising when stock prices fall, but they have also delivered positive returns as central banks manipulated interest rates lower. For younger investors, this relationship is all they have known, but there have been times throughout history when stock and bond prices move together. However, that has not always been the case.

Observe in the chart below how long-term Treasury bonds and the S&P 500 were positively correlated from the late 1960s to 2000.

As we enter a new investing regime of higher rates and sticky inflation, this change in the relationship between the prices of bonds and stocks has enormous ramifications for all investors.

It means that bonds no longer provide the portfolio protection for investors like they have since 2000. As Bob Dylan famously sang, 'The Times They Are A-Changin’. But why now? One word — inflation.

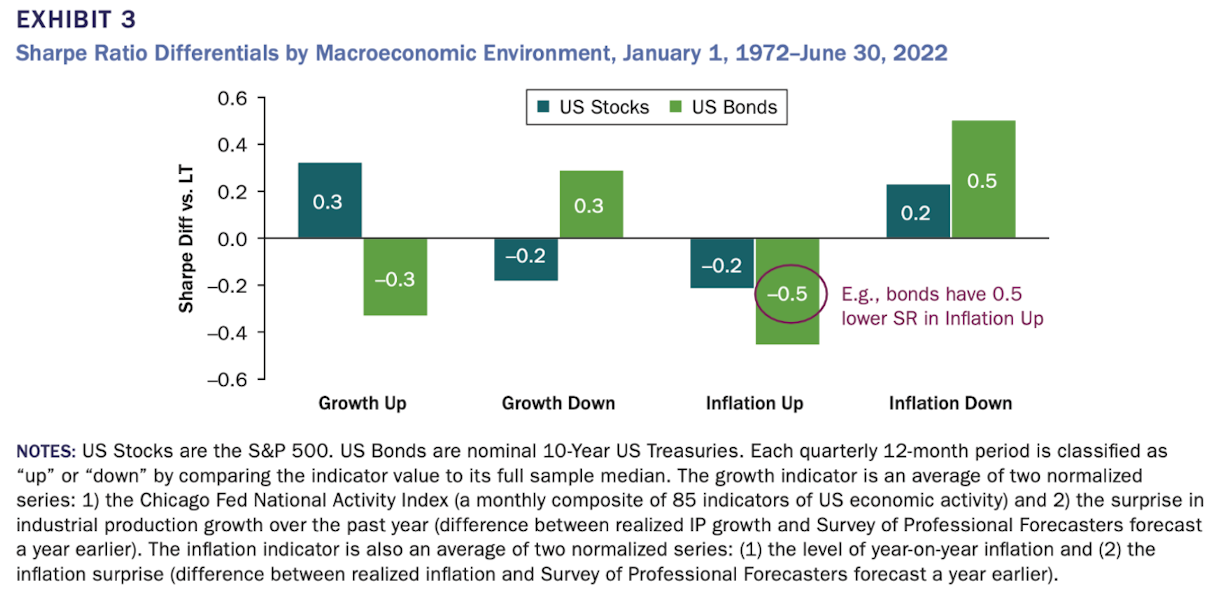

AQR Capital Management looked into when stocks and bonds stop enhancing risk-adjusted returns for a diversified portfolio and discovered that this was mostly observed in periods of rising inflation.

The report writes,

“What about inflation? Positive inflation news directly reduces the value of bonds’ fixed nominal cash flows, as well as raising short-term interest rate expectations, so prices fall. Equities, in theory, give investors a claim on real cash flows, but in practice, rising inflation has usually been associated with falling stock prices. Stocks and bonds therefore have same-signed sensitivities to inflation news.” — AQR Capital Management

The figure below from the report illustrates this changing relationship by categorizing 50 years of data into “up” and “down” growth and inflation regimes and calculating the risk-adjusted return (Sharpe ratio) of stocks and bonds in each regime. The chart shows the difference in Sharpe ratio for each asset class in each regime, and finds that Sharpe ratios for bonds and stocks decline in tandem in periods of rising inflation.

AQR Capital Management

The chart above should serve as a warning sign for investors today. Bonds have already been bleeding out during this period of elevated inflation and have not offset stock market declines.

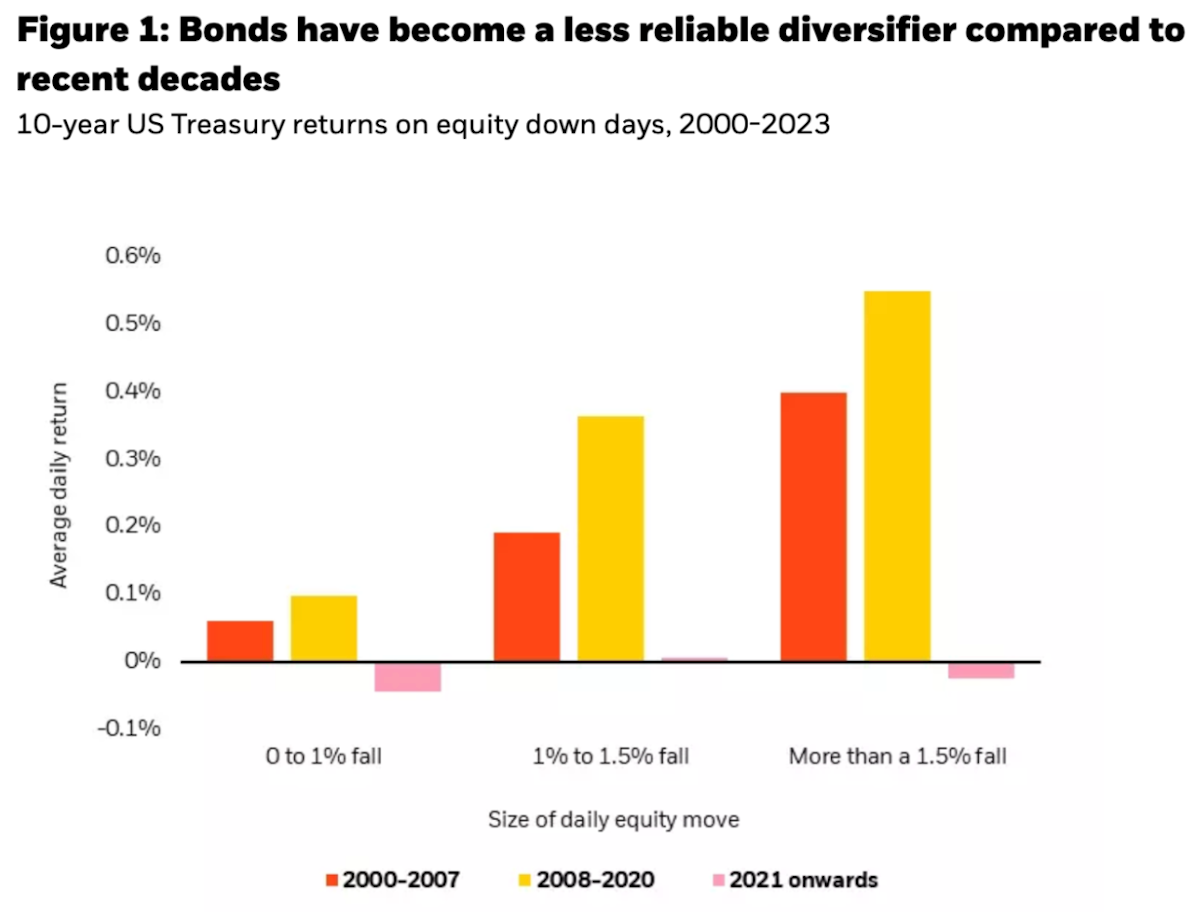

This is highlighted in the figure below showing how bonds have not provided positive returns on equity down days since 2021.

BlackRock

So what are sophisticated investors doing to prepare for this new investing environment of high inflation brought on by reckless spending? They are increasingly allocating to alternative asset classes to enhance returns and reduce risk through diversification.

Traditionally, in times of inflation, investors have turned to fixed-supply alternative assets such as real estate, commodities, dividend-yield stocks, and gold. But this time around, investors could turn to a new type of fixed-supply alternative asset, one with a growth potential that cannot be matched — Bitcoin.

We are already seeing this narrative play out.

Asset management firm AllianceBernstein, with over $600 billion in AUM, recently called Bitcoin a “safe haven asset” in a memo.

CEO of BlackRock Larry Fink called it a “flight to quality” on national television.

Billionaire investors Paul Tudor Jones and Stanley Druckenmiller both said they are constructive on Bitcoin in a recent interview.

Even Bitcoin critics like Mohamed El-Erian, Chief Economic Advisor at Allianz, recently admitted that investors are beginning to view Bitcoin as a safe haven asset because they have lost confidence in government bonds.

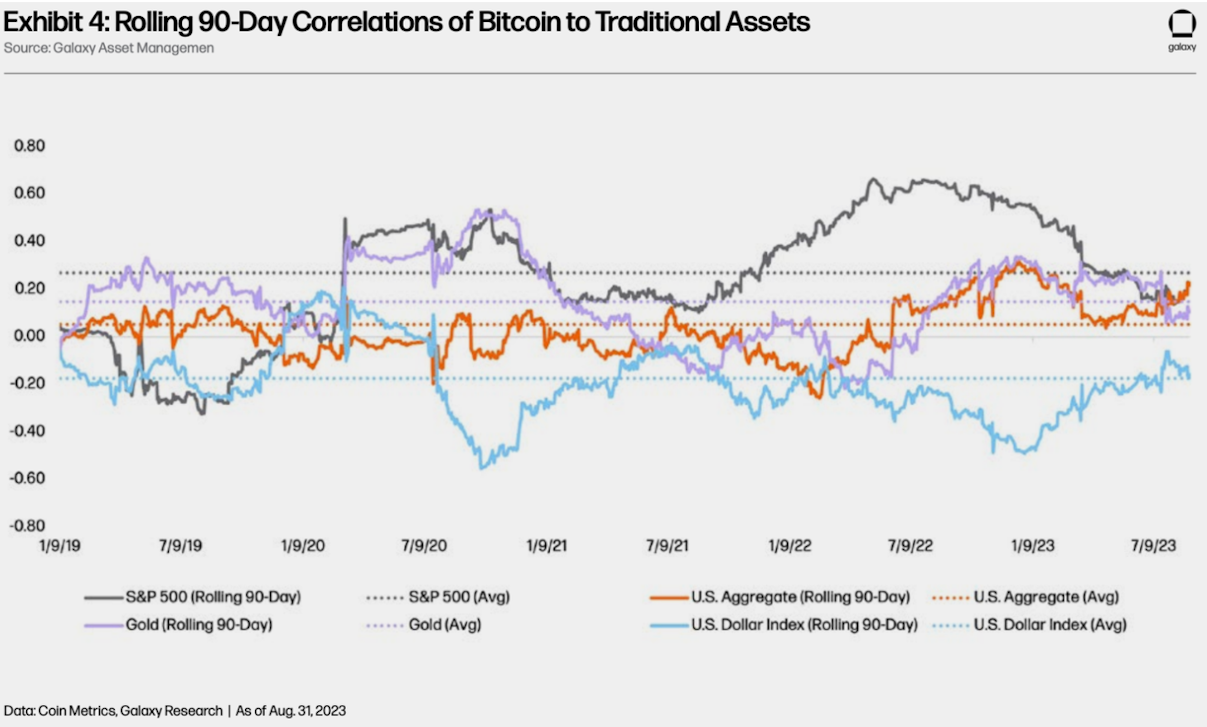

And why not? Over the last 5 years, Bitcoin has shown to have a low and even negative rolling 90-day correlation with other major asset classes.

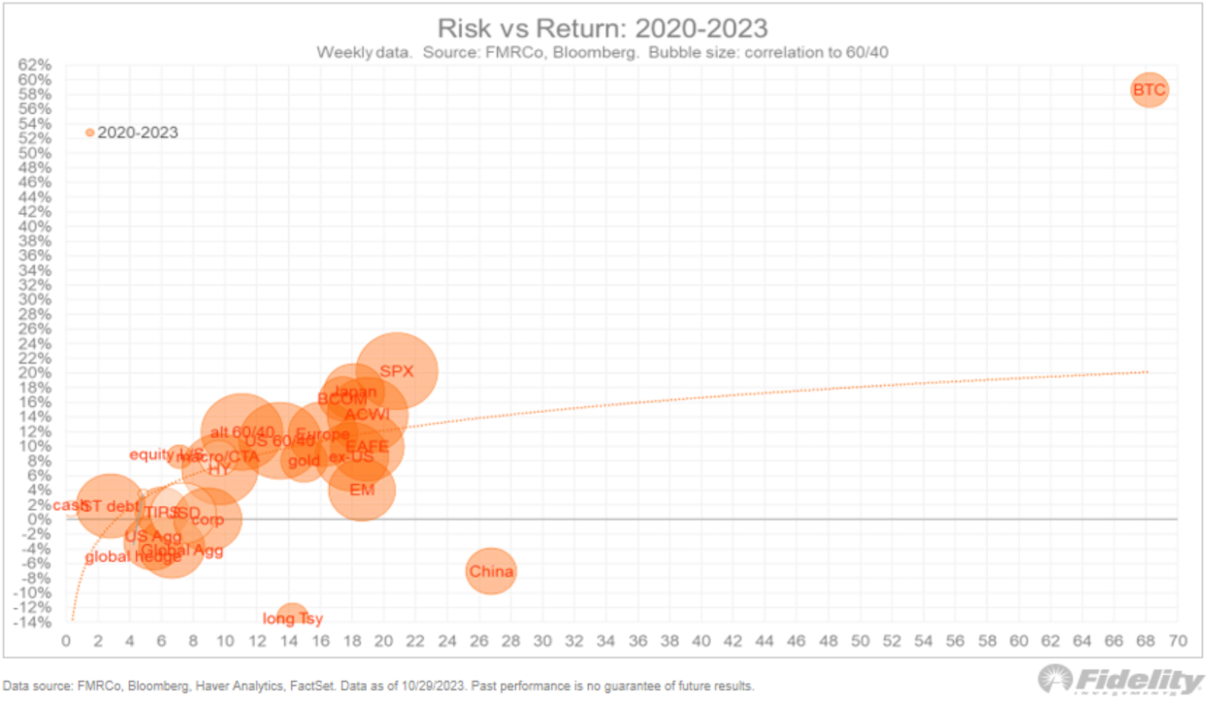

Fidelity’s Director of Global Macro, Jurrien Timmer recently called Bitcoin “exponential gold” and highlighted below how Bitcoin’s risk-adjusted returns are simply in another stratosphere compared to other asset classes since 2020.

When an asset outperforms like this and is doing so in an uncorrelated fashion, that’s going to catch the eyes of a lot of portfolio managers.

There have been some data points that suggest that this recent rally has been driven by institutional investors who may be beginning to understand how Bitcoin could enhance their portfolios.

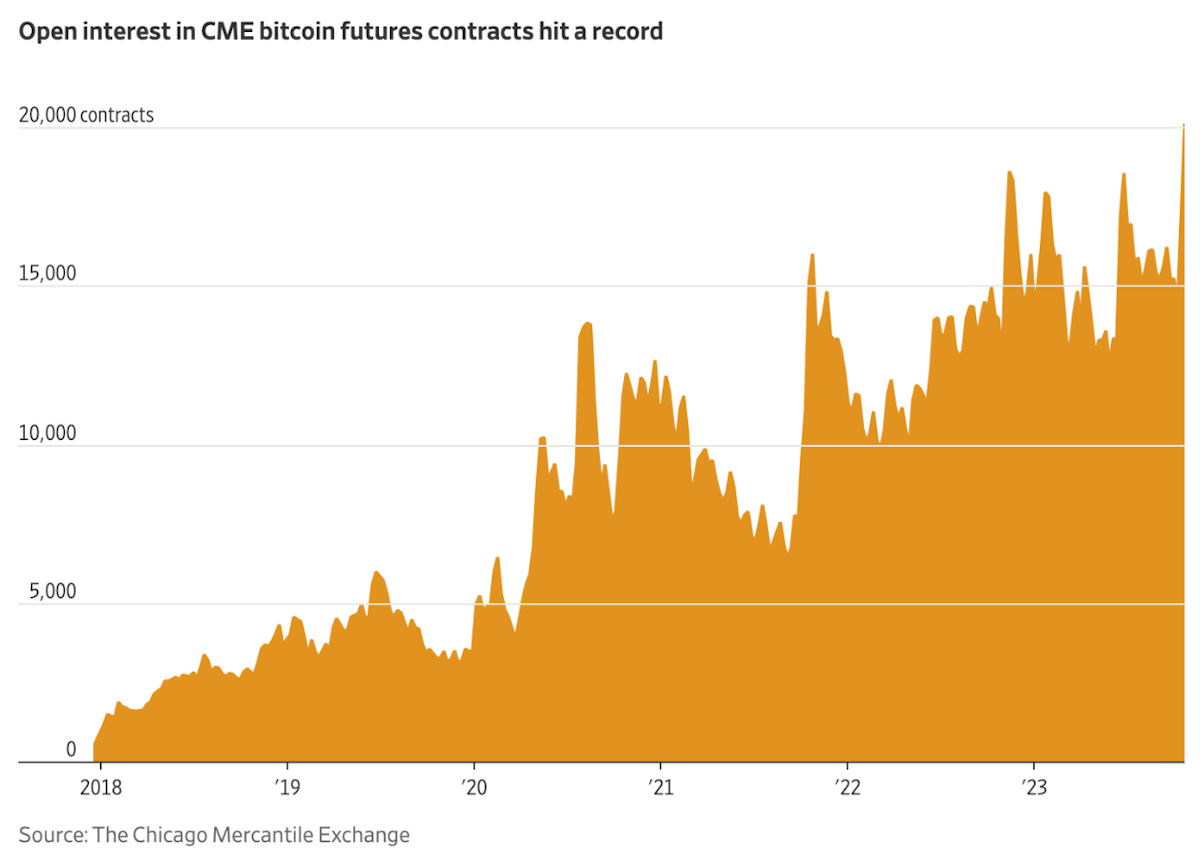

One is that Bitcoin futures open interest — the number of unsettled and active contracts — trading on the Chicago Mercantile Exchange surpassed previous record highs from 2021.

Institutional traders prefer to trade on this highly regulated and respected trading venue and tend to use futures products more than retail investors, so this metric is a good proxy for institutional interest.

Fun fact: the notional value of the open interest in the CME bitcoin futures contracts surpassed 100,000 BTC for the first time in history.

Some other metrics hinting at bigger players driving this recent price rally can be observed on-chain.

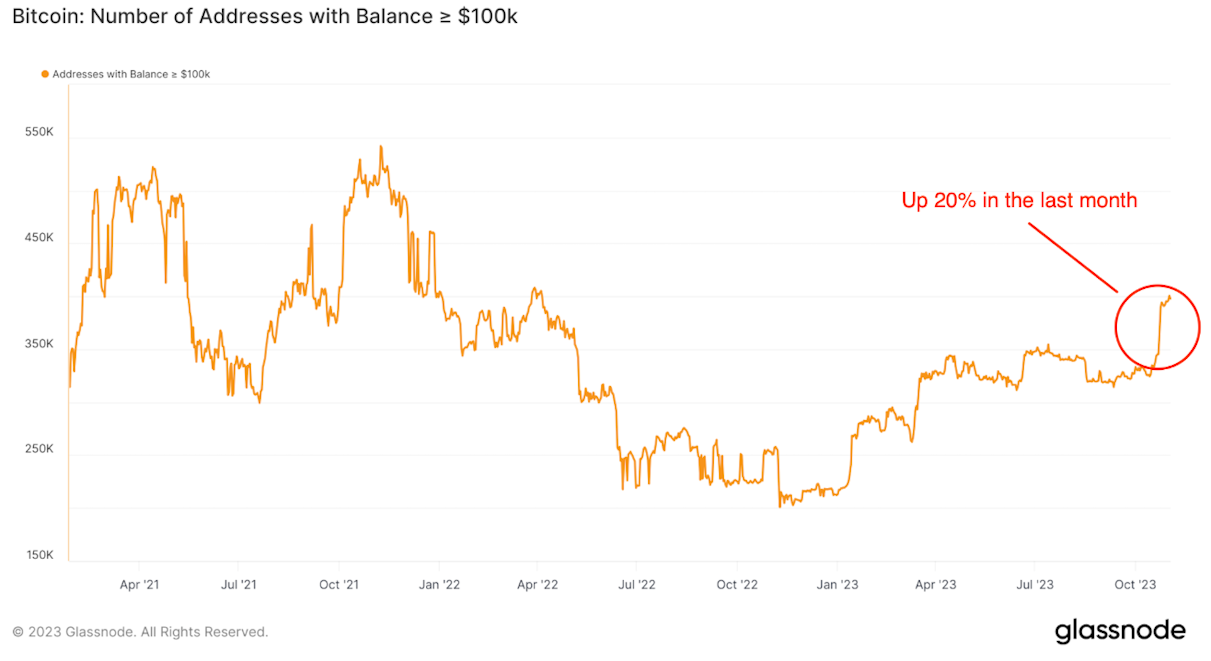

The number of addresses holding at least $100,000 in BTC has increased by 20% over the last month.

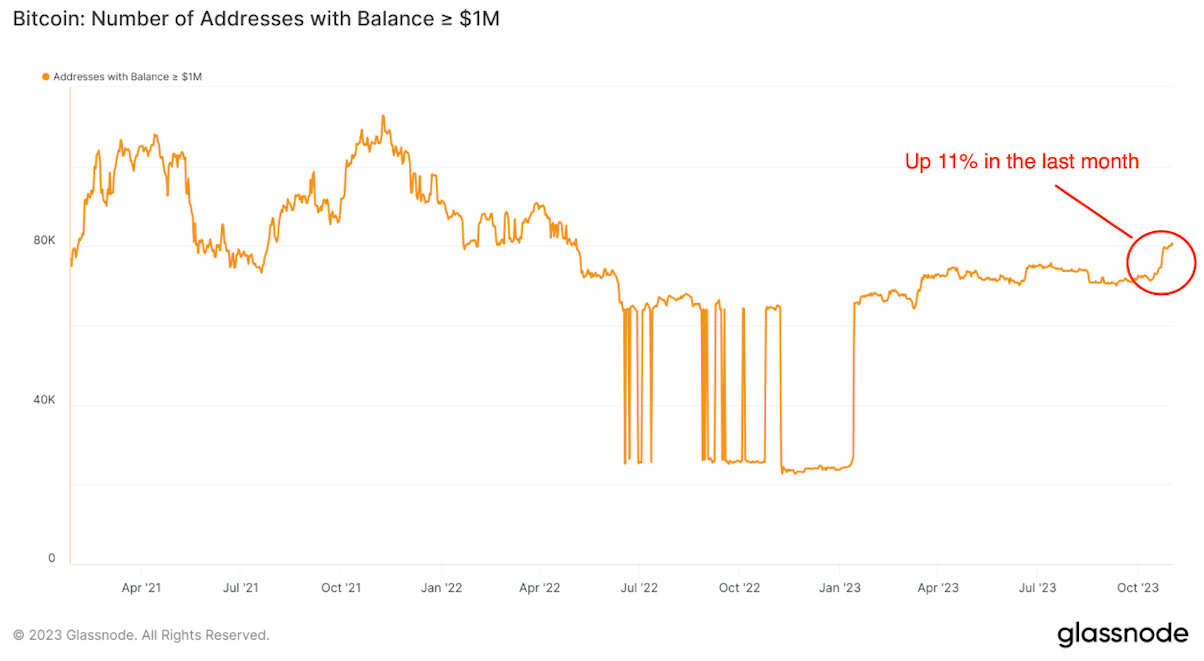

In addition, the number of addresses holding at least $1 million in BTC has increased by 11% over the same time frame.

It seems that institutional and other big investors are waking up to the fact that Bitcoin has a unique value proposition. It has the characteristics of a safe haven asset like gold but with the growth potential of a promising tech stock.

Today, the economy is running hot in an unhealthy manner as the government continues to spend money it doesn’t have and stimulate the economy in the short term at the expense of long-term stability. The bond market is starting to question the sustainability of these policies and that has caused historic losses for bond investors. It’s time investors begin to understand that we have entered a new inflationary regime driven by reckless spending that is only projected to grow by the CBO’s own projections. As a result, it’s never been more important for market participants to understand how this new environment changes the relationship between stocks and bonds and for them to consider other strategies to diversify their portfolios to protect their wealth in the years to come.

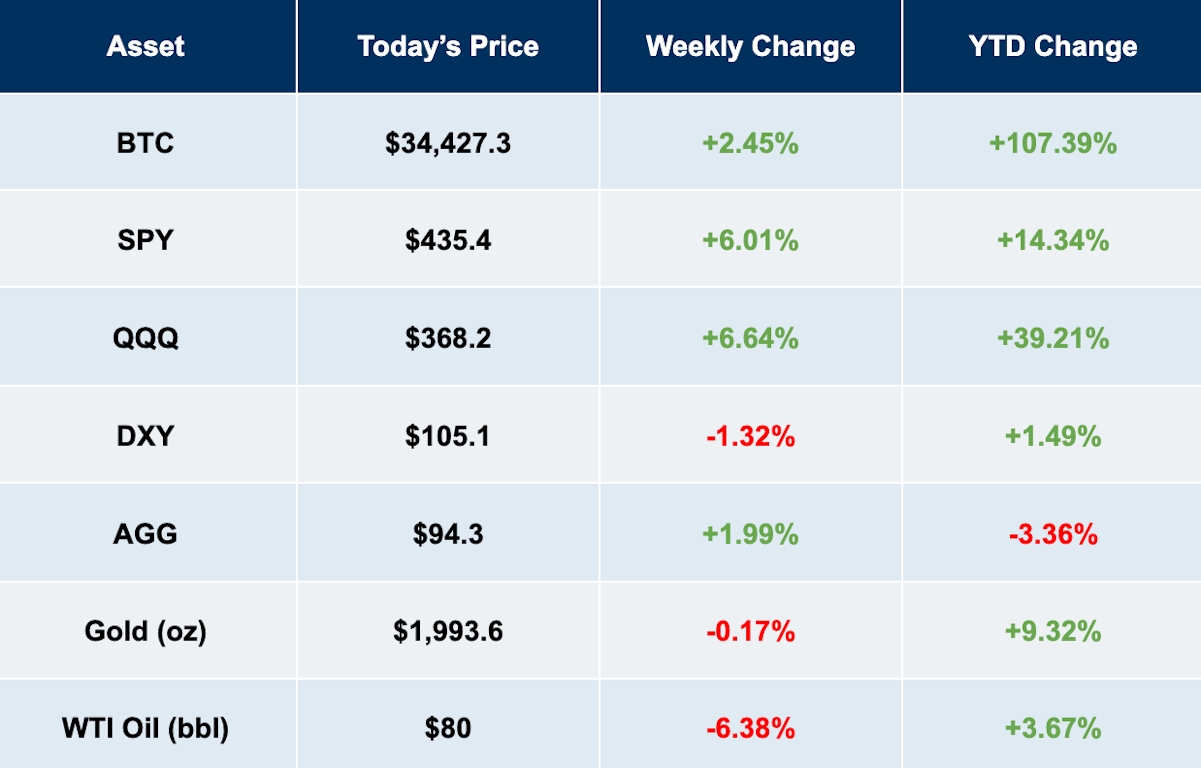

Market Overview

Tradingview, Prices as of 11/03/23

Hold your IRA with the most trusted name in Bitcoin.

Sam Callahan is the Lead Analyst at Swan Bitcoin. He graduated from Indiana University with degrees in Biology and Physics before turning his attention towards the markets. He writes the popular “Running the Numbers” section in the monthly Swan Private Insight Report. Sam’s analysis is frequently shared across social media, and he’s been a guest on popular podcasts such as The Investor’s Podcast and the Stephan Livera Podcast.

News

More NewsThoughts on Bitcoin from the Swan team and friends.

Swan Guard brings world-class Bitcoin security with advanced risk controls, scam defense, and expert support — vigilantly protecting your Swan account and safeguarding your Bitcoin.

After managing a Swiss gold fund for 8 years, I realized Bitcoin surpasses gold as the ultimate store of value. Here’s why every gold investor should study Bitcoin closely.

Ben Werkman joins Swan as CIO. New LBE primer explains key concepts, implementation steps, risk management, and valuation approaches.