Swan Private Market Update #28

This Market Update report was originally sent to Swan Private clients on March 10th, 2023. Swan Private guides corporations and high net worth individuals globally toward building generational wealth with Bitcoin.

This Market Update report was originally sent to Swan Private clients on March 10th, 2023. Swan Private guides corporations and high net worth individuals globally toward building generational wealth with Bitcoin.

Over the last year, the Federal Reserve has undergone one of the fastest rate hiking cycles in its history. As rates have soared and the proverbial tide has gone out, many companies in the broader cryptocurrency industry were discovered to be swimming naked. One by one, we’ve seen cryptocurrency companies like FTX, Voyager, BlockFi, Genesis, Celsius, and Three Arrows Capital shut their doors. Some of these firms were woefully mismanaged as they overextended themselves in the ultra-low interest rate environment, while others were revealed as outright frauds.

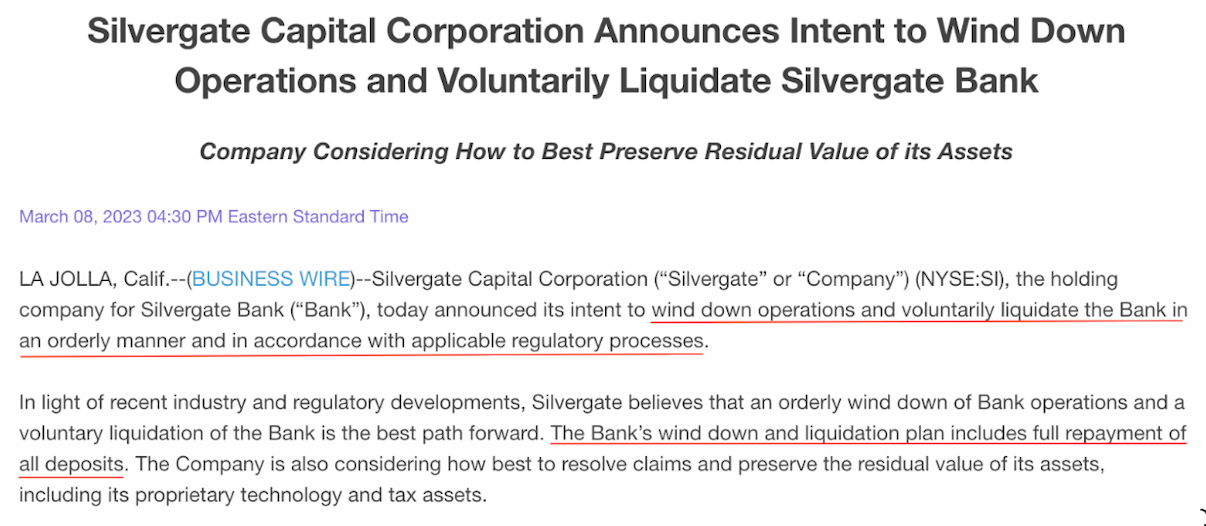

The crypto contagion moved up to the banking sector this week when crypto-friendly bank, Silvergate Capital, announced it will voluntarily liquidate and provide full repayment of all deposits.

Silvergate is the latest victim of the contagion that began last spring with the collapse of the algorithmic stablecoin Terra Luna as the Federal Reserve began raising interest rates. This news comes during a broader cross-agency regulatory crackdown on the cryptocurrency industry that began in earnest after the collapse of FTX.

Silvergate was a relatively small bank that rose to prominence over the years as one of the primary banks serving the cryptocurrency industry. In the last 5 years, it saw its deposits explode upwards as it seized the opportunity during the cryptocurrency bubble fueled by ultra-low interest rates, peaking at over $14 billion in December 2021.

Silvergate continued to grow rapidly after it launched its Silvergate Exchange Network (SEN), which allowed for 24/7 real-time, settlement of digital assets between investors and crypto exchanges. The SEN platform grew to become a critical piece of infrastructure for the broader cryptocurrency industry.

The graphic below highlights how the SEN platform served as the central plumbing of the industry, connecting many of the largest cryptocurrency firms in the broader crypto ecosystem.

Silvergate Capital

Silvergate specifically catered its business to the digital asset industry, and as of September 30th, 2022, 90% of its overall deposit base came from crypto firms. Some of these clients included now-bankrupt firms such as BlockFi and FTX.

To give you an idea of Silvergate’s relationship with the crypto industry, below is a quote from disgraced former FTX CEO Sam Bankman-Fried gushing about Silvergate in Congressional testimony last year,

“Life as a crypto firm can be divided up into before Silvergate and after Silvergate…It’s hard to overstate how much it revolutionized banking for blockchain companies.” — Sam Bankman-Fried

As the crypto bubble popped at the end of 2021, interest in crypto started to wane and clients started to leave Silvergate. This trend only worsened when large firms began to blow up left and right. As a result, Silvergate experienced a significant outflow of deposits and revenues.

In its Q4 financial statement, Silvergate wrote,

“During the fourth quarter of 2022, the digital asset industry experienced a transformational shift, with significant overleverage in the industry-leading to several high-profile bankruptcies. These dynamics created a crisis of confidence across the ecosystem and led many industry participants to shift to a ‘risk off’ position across digital asset trading platforms. In turn, the Company saw significant outflows of deposits during the quarter and took several actions to maintain cash liquidity.”

This drop in business activity can be observed in the decline in usage of the SEN platform. SEN platform volumes were down 47% in the fourth quarter compared to the fourth quarter of the year prior. On top of that, digital asset customers started to leave the bank in droves. Sivergate had 1,620 digital asset customers on December 31, 2021, compared to just 1,381 a year later.

This trend accelerated rapidly in Q4, as Silvergate clients rushed for the exits as they feared for the bank’s future as it came under scrutiny from regulators and politicians in the aftermath of FTX.

In December 2022, Senator Elizabeth Warren, Senator John Kennedy, and Congressman Roger Marshall penned a letter to Silvergate CEO Alan Lane asking for information about Silvergate’s operations, stating, “The public is owed a full accounting of the financial activities that may have led to the loss of billions in customer assets, and any role that Silvergate may have played in these losses.”

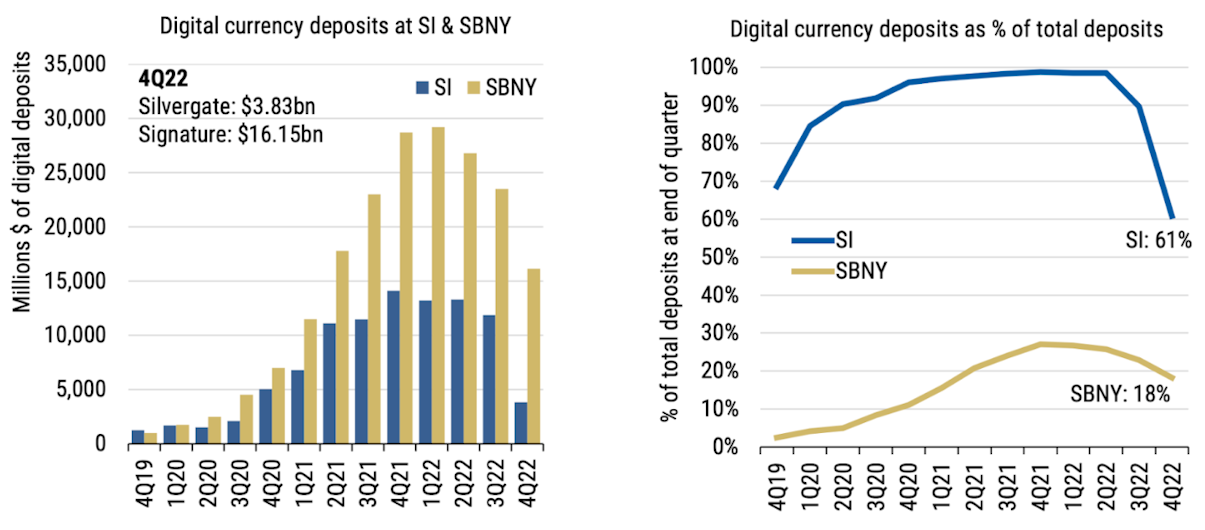

During Q3, the average digital asset customer deposits stood at $12 billion, during Q4, that number stood at $7.3 billion, down 39%.

Below are charts that show how the digital currency deposits of SIlvergate and Signature, another popular crypto-bank, fell off a cliff in Q4. Silvergate’s digital currency deposits fell a whopping 68% Q/Q in Q4.

Morgan Stanely

The problem here is that a majority of Silvergate’s deposit base came from digital asset customers. This deposit base is extremely volatile and is tied to the market sentiment of the broader digital asset industry. When the prices fall, these clients lose interest and withdraw their funds, which requires Silvergate to repay those deposits. It makes for an unstable, volatile source of funding that can disappear rapidly.

This is what the FDIC, OCC, and Fed were warning about in a recent rare joint statement when they urged banks to apply effective risk management when dealing with deposits linked to crypto entities. They stated, “Significant volatility in crypto-asset markets, the effects of which include potential impacts on deposit flows associated with crypto-asset companies.”

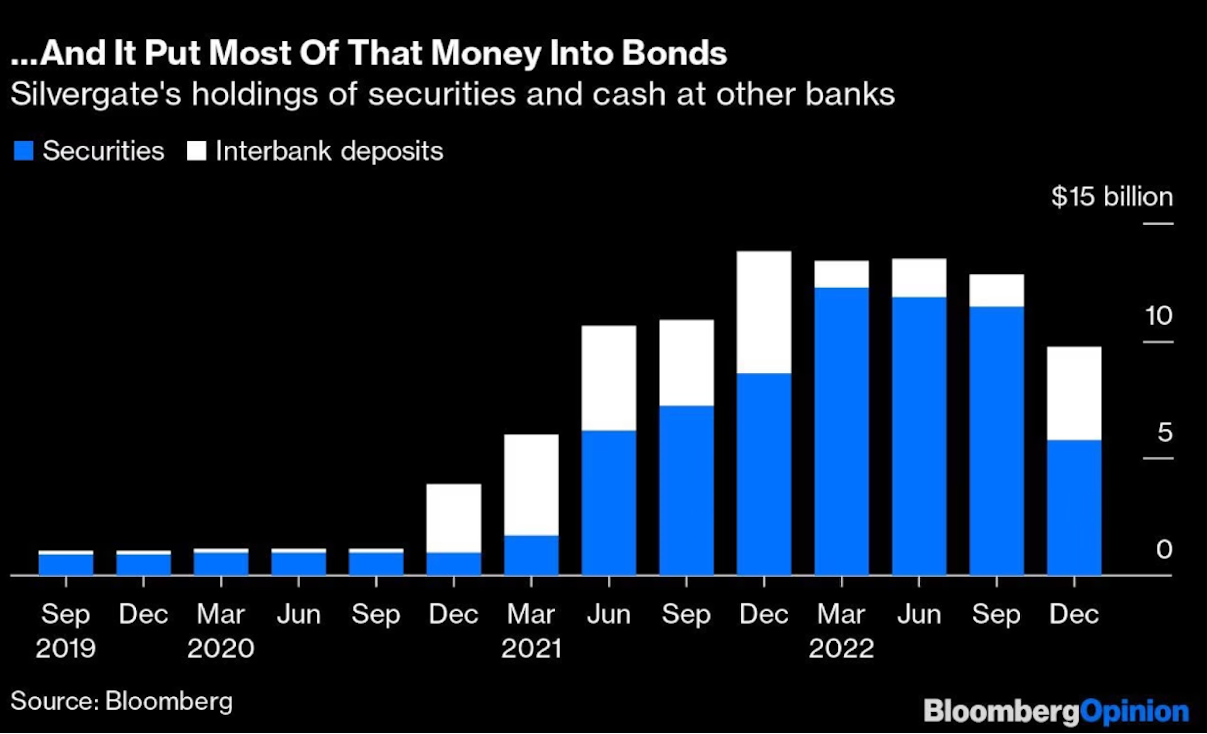

To prepare for this scenario, Silvergate invested most of its funds in long-duration mortgage-back securities and Treasury bonds. It bought a majority of these bonds before the Federal Reserve went on its hiking tirade when interest rates were low.

As the Fed raised interest rates, the value of Silvergate’s bond holdings plunged, eroding the value of the bank’s assets. The catch here is that, per accounting rules, Silvergate didn’t have to mark their bond holdings to market (at the current market price) so long as they held their bonds to maturity. However, when depositors started to flee the bank, Silvergate was forced to sell these bond holdings to meet the withdrawals.

When this happened, Silvergate had to mark to market all the bonds on its balance sheet and report a realized loss. This ate int the bank’s equity, which only spooked clients more, leading to more withdrawals. A classic bank run ensued.

Suddenly, Silvergate was left in a liquidity crisis as it tried to meet withdrawals by selling its bond positions that were underwater due to the rising rate environment. Silvergate sold its bond positions at a large loss to fund withdrawals, inflicting a $1 billion hole in its earnings at the end of 2022.

This is the problem entities run into when they borrow short and lend long. There was an interest rate mismatch where Silvergate owed money to depositors who wanted to withdraw their money now, but they had their assets in long-duration bonds that they couldn’t afford to sell without marking a large loss on their balance sheet.

The problems continued to mount for Silvergate as they continued to lose depositors amidst a slew of bad news in 2023. Depositors continue to flee, its major business partners like Coinbase and Galaxy Digital left the bank, and it came under investigation by the DOJ for its involvement with FTX.

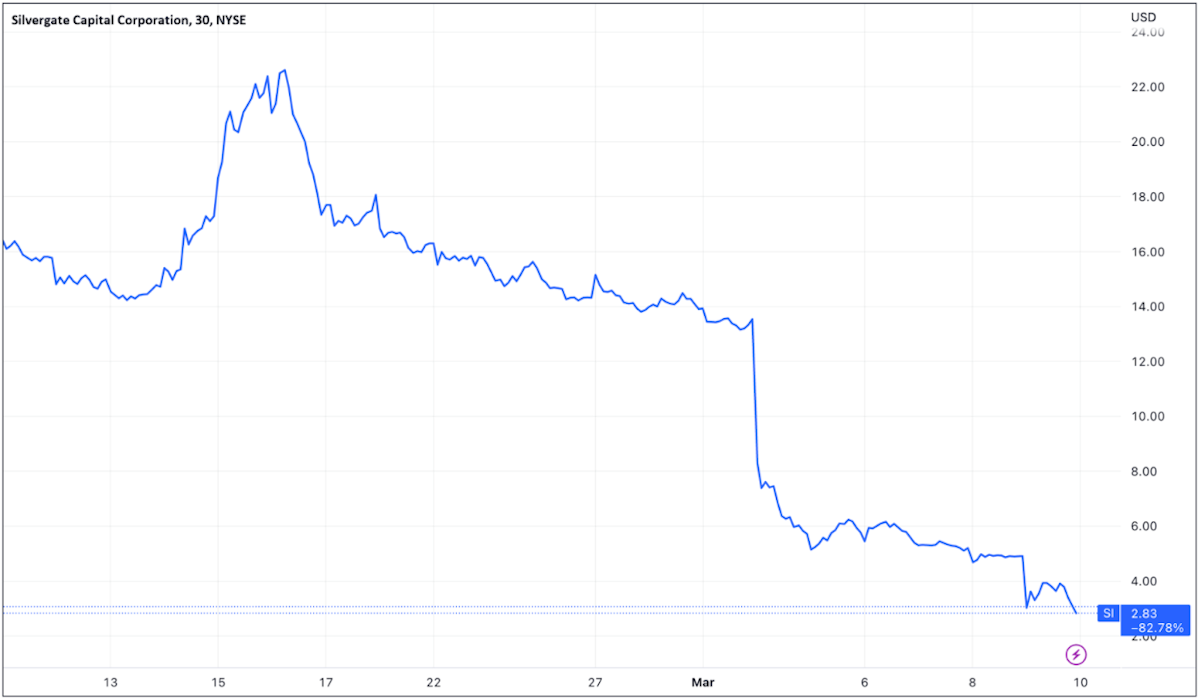

These developments made Silvergate’s stock a prime target for short sellers. According to S3 partners, its stock became the most shorted U.S. stock, with open short interest estimated to be at 22.6 million shares, or 82% of float.

Silvergate’s stock price is now down -82.7% over the last month alone.

Now that Silvergate has declared that it will wind down its operations, this has caused Senator Elizabeth Warren to come out of the woodwork and claim that this was a result of “crypto risk.”

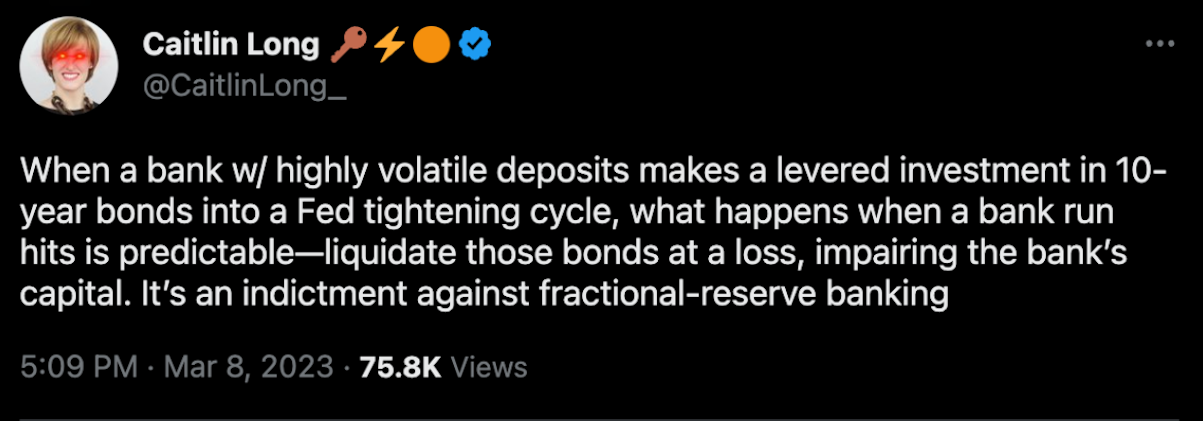

But to call the fall of Silvergate a result of “crypto risk” is missing the big picture. In fact, Silvergate should be applauded for winding down operations in an orderly fashion that will make all depositors whole. This was a classic example of what can happen when banks do not have the assets on hand to fund withdrawals. This is what can happen with any fractionally reserved bank in the event of a bank run, regardless of if the bank was dealing with the cryptocurrency industry or not.

CEO of Custodia Bank, Caitlin Long explains this well in the tweet below.

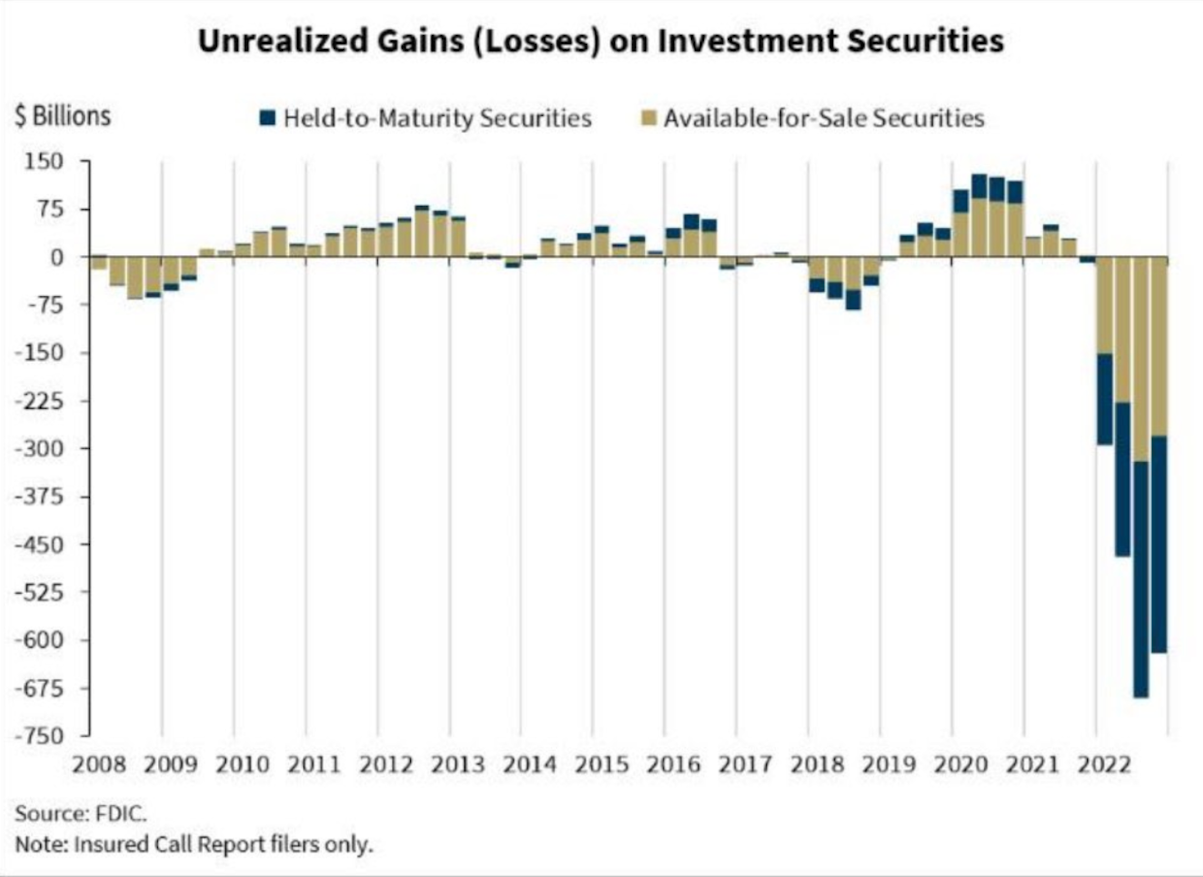

This Silvergate development highlights a bigger risk within the banking sector as a whole. FDIC-insured banks are currently sitting on massive unrealized losses as their bond holdings have lost a significant amount of value as interest rates have soared.

Below shows that there are currently over $600 billion in unrealized losses held by FDIC-insured banks today, mostly consisting of bonds that are deeply underwater.

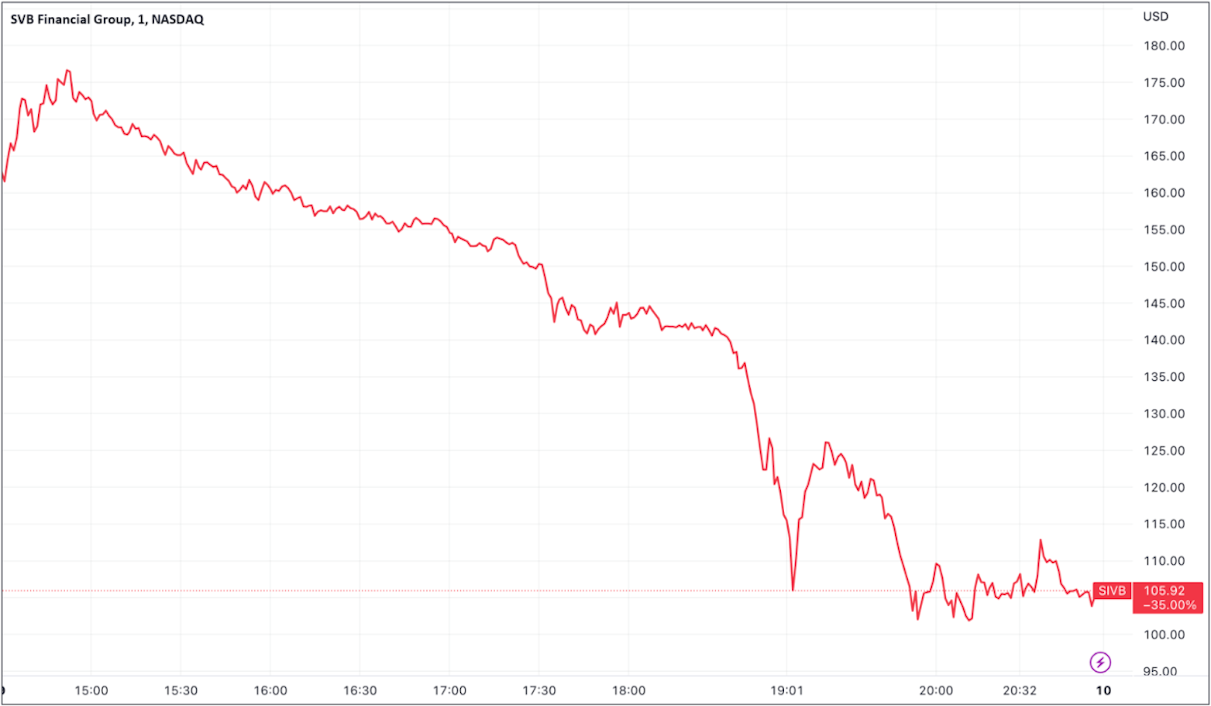

This dynamic of the wide difference between the bonds’ book values and market values is not isolated to crypto banks like Silvergate. This became evident when the 16th largest commercial bank, Silicon Valley Bank Financial Group experienced a similar problem and saw its stock drop -35% on Thursday after it lost $1.8 billion selling $21 billion worth of bonds to fund withdrawals.

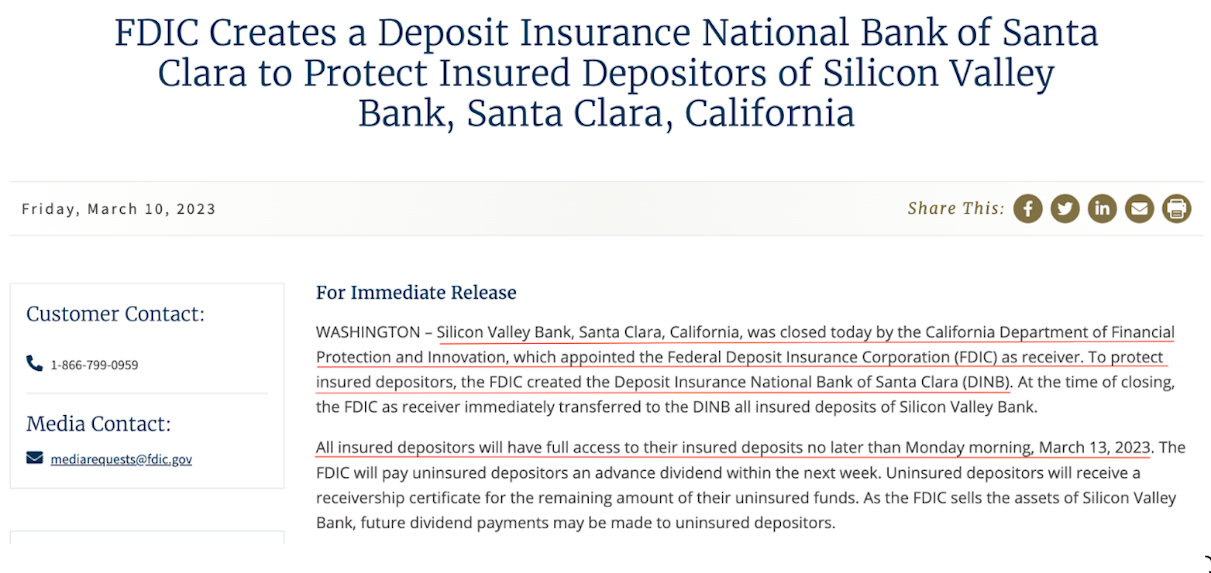

Shares of SVB were halted Friday morning as the shares sold off another -65% overnight as the bank desperately attempted to raise capital. Later that morning, it was announced that the bank would be closed and regulators would take control of its deposits.

The bank failure of Silicon Valley Bank marks the second-largest bank failure in history and the largest bank failure since the Global Financial Crisis.

All of SVB’s deposits that are <$250,000 are insured by the FDIC, but it is estimated that over $150 billion, around 97% of its deposits, are uninsured, given that many of SVB’s customers are technology companies.

This could pose a big problem to the thousands of companies that banked with SVB when it comes to their ability to make payroll over the next several weeks. We have not seen the end of this story.

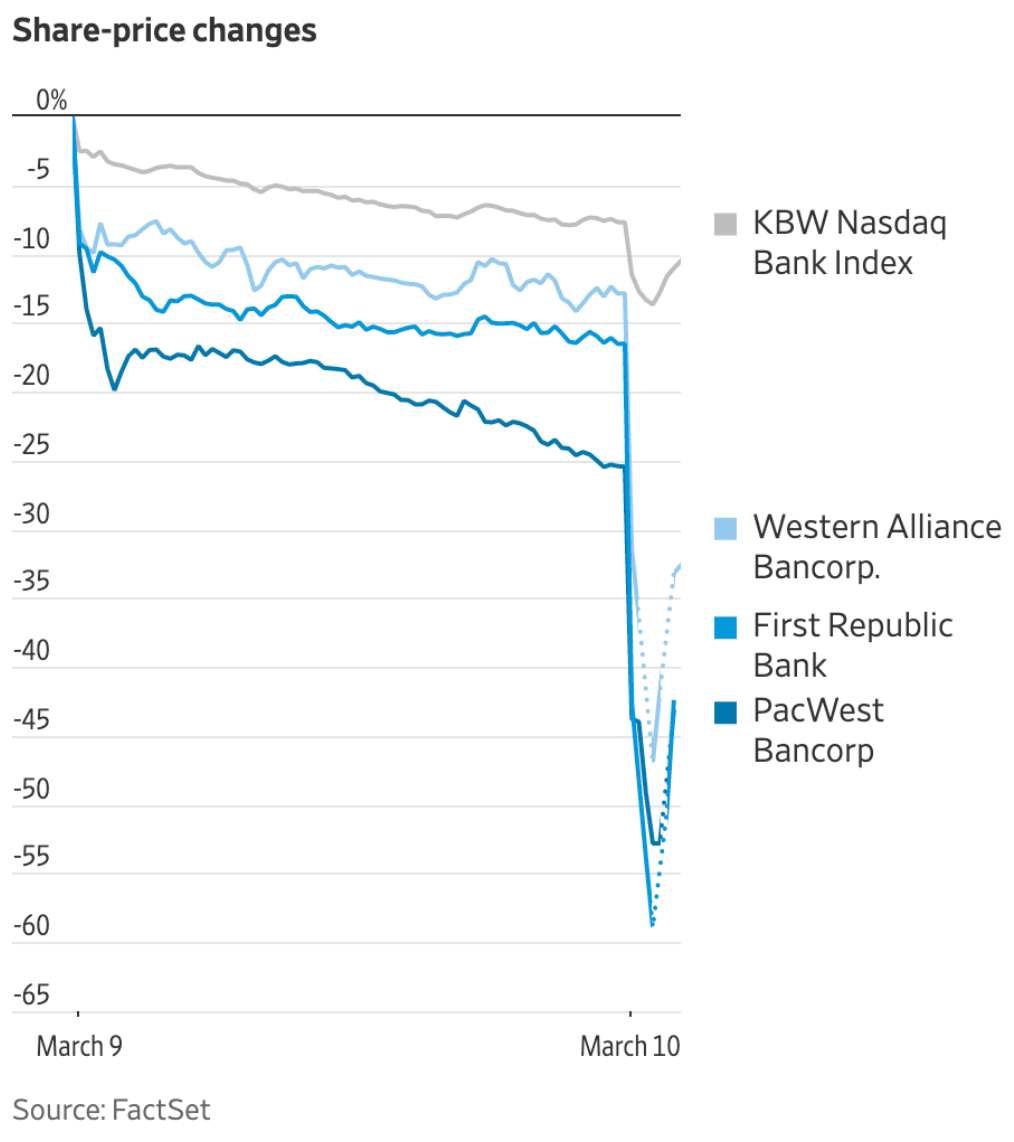

On Friday morning, fear continued to spread to other regional banks such as First Republic Bank, PacWest Bancorp, and Western Alliance Bancorp as their share prices plummeted and were eventually halted by authorities.

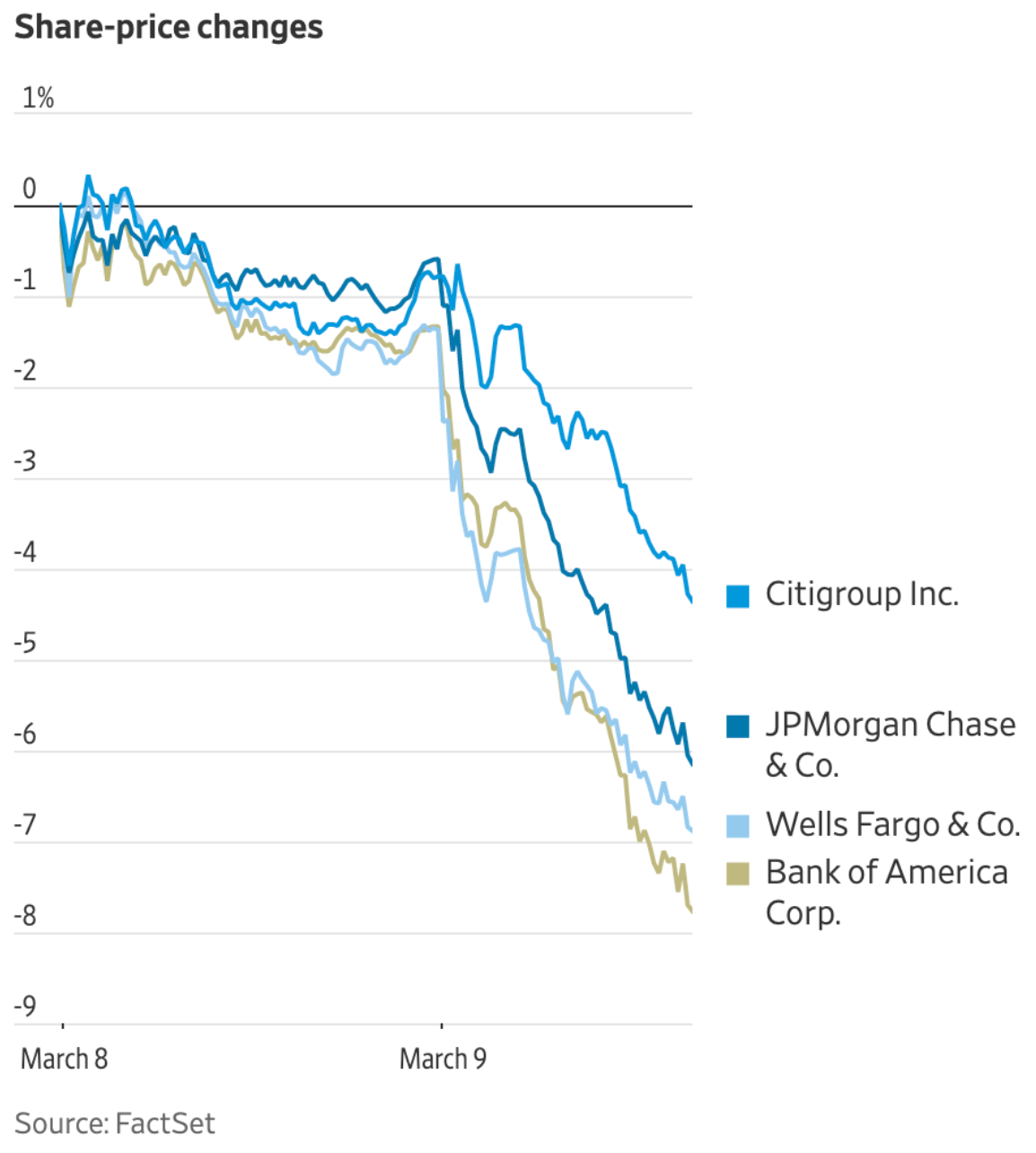

The contagion in the financial industry was not just isolated to smaller regional banks. The four major U.S. banks lost an estimated $52 billion in market value on Thursday alone.

This carnage in the banking industry comes after Federal Reserve Chairman Jerome Powell testified before Congress earlier in the week stating that it is likely that the Fed will need to raise rates higher and hold them for longer.

Powell said, “The ultimate level of interest rates is likely to be higher than previously anticipated. If the totality of the data were to indicate that faster tightening is warranted, we’re prepared to increase the pace of rate hikes.”

After Powell’s hawkish testimony, the market gave a 65% chance that the Fed would hike rates another 0.50% at the next FOMC meeting. Last month, this probability was only around 10%.

However, given the recent turmoil in the banking industry, the odds of a 50 bps rate hike have declined. Many analysts have speculated that the Fed would eventually have to stop hiking interest rates to battle inflation “when something breaks.” Thursday was the first sign that there might be some cracks forming in the financial system due to this new high-interest rate environment.

If there is one thing that the Federal Reserve likes to bail out, it’s banks. Could this turmoil in the banking sector be the start of something bigger that could force the Fed Pivot that so many market participants have longed for?

Treasury Secretary Janet Yellen certainly seemed concerned about these recent developments. In a testimony today before the U.S. House Ways and Means Committee, she stated that the Treasury Department is “monitoring a few banks amid SVB Financial’s funding woes, ”

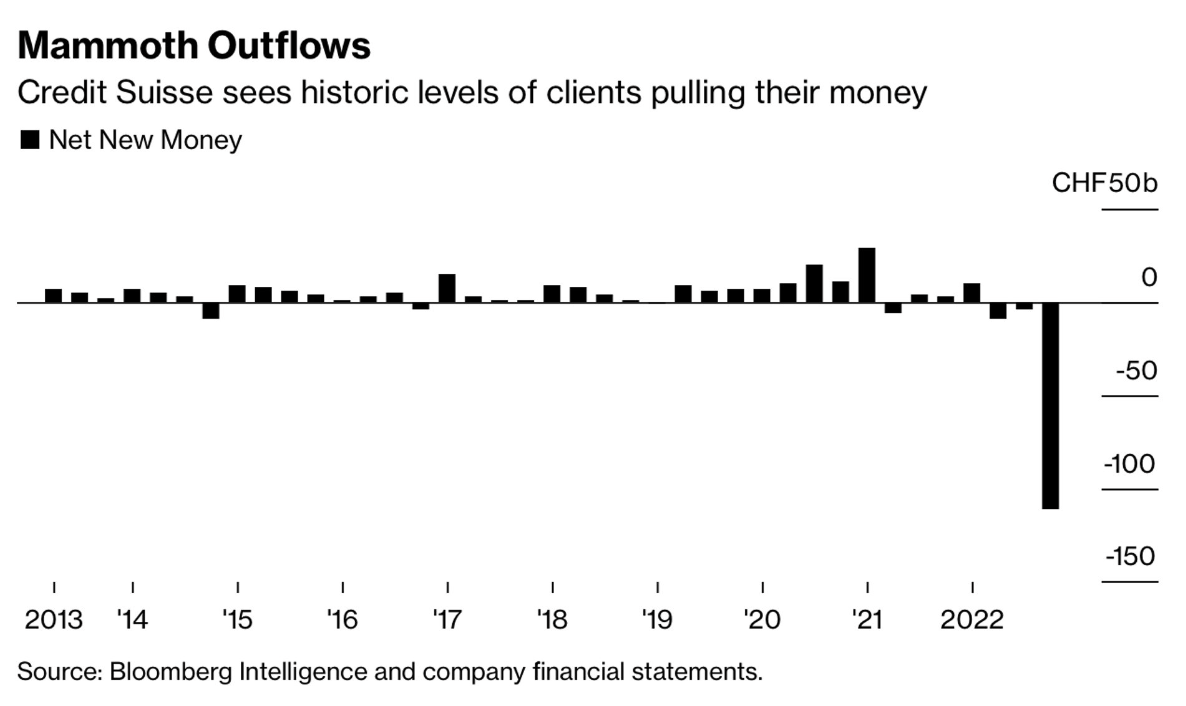

For this contagion to become systemic, either a lot more smaller banks would need to come under duress or a systemically important financial institution would have to come under pressure. One such large financial institution to keep an eye on is Credit Suisse, which has also seen deposits run out its door in record numbers.

Clients pulled around $120 billion in deposits from Credit Suisse in the last three months alone, and the bank reported a $1.3 billion loss in Q4 of 2022. The health of this large, important European bank is something to keep an eye on in the months to come.

The large U.S. banks are in a very different situation compared to Credit Suisse. Every year the Fed conducts a rigorous stress test to assess how these banks would perform under periods of distress. The scenario tested late last year was the unemployment rate peaking at 10%, real GDP declining by more than 3.5%, and steep declines in asset prices across stocks, bonds, and real estate. The results of the stress test showed that these large banks had sufficient capital to withstand these hypothetical adverse conditions.

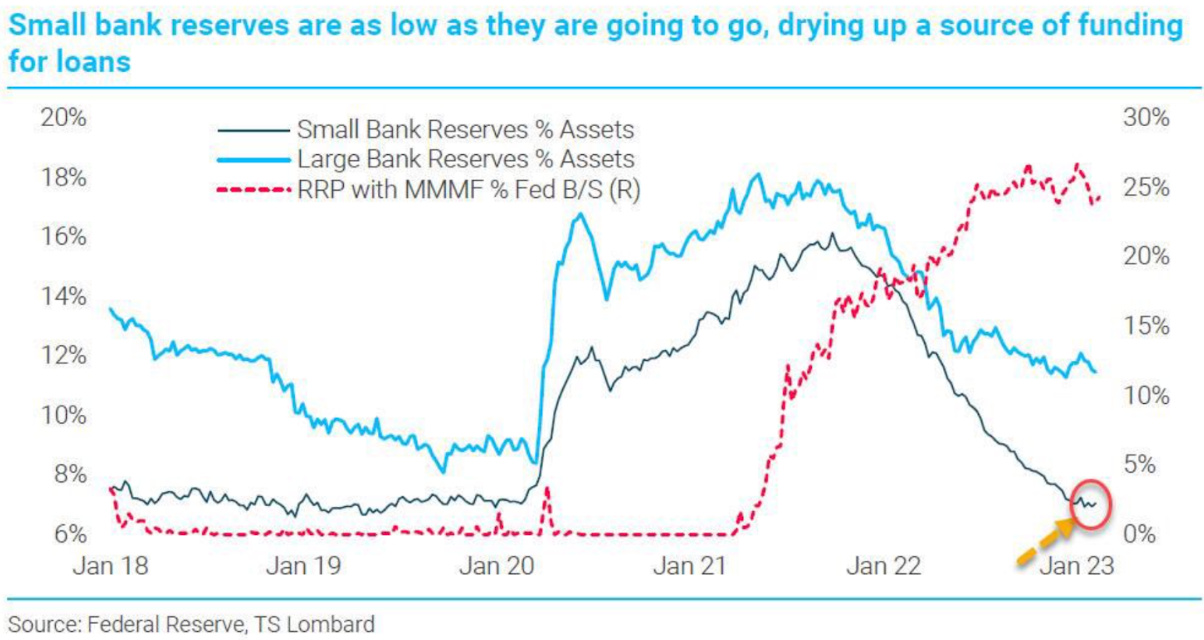

Large U.S. banks have built up a large capital buffer due to regulations passed in the aftermath of the Global Financial Crisis, but small banks are not as protected. Their reserves continue to get drained, putting them at increased risk.

Deposits continue to flee these small banks, in part, because clients can now obtain higher interest rates in money market funds and treasury bills compared to the low rates of interest in deposit accounts. Small bank funding continues to dry up just as their bond portfolios have lost value as the Fed has hiked interest rates, a toxic combination for these institutions. We will be monitoring the banking sector closely in the coming weeks.

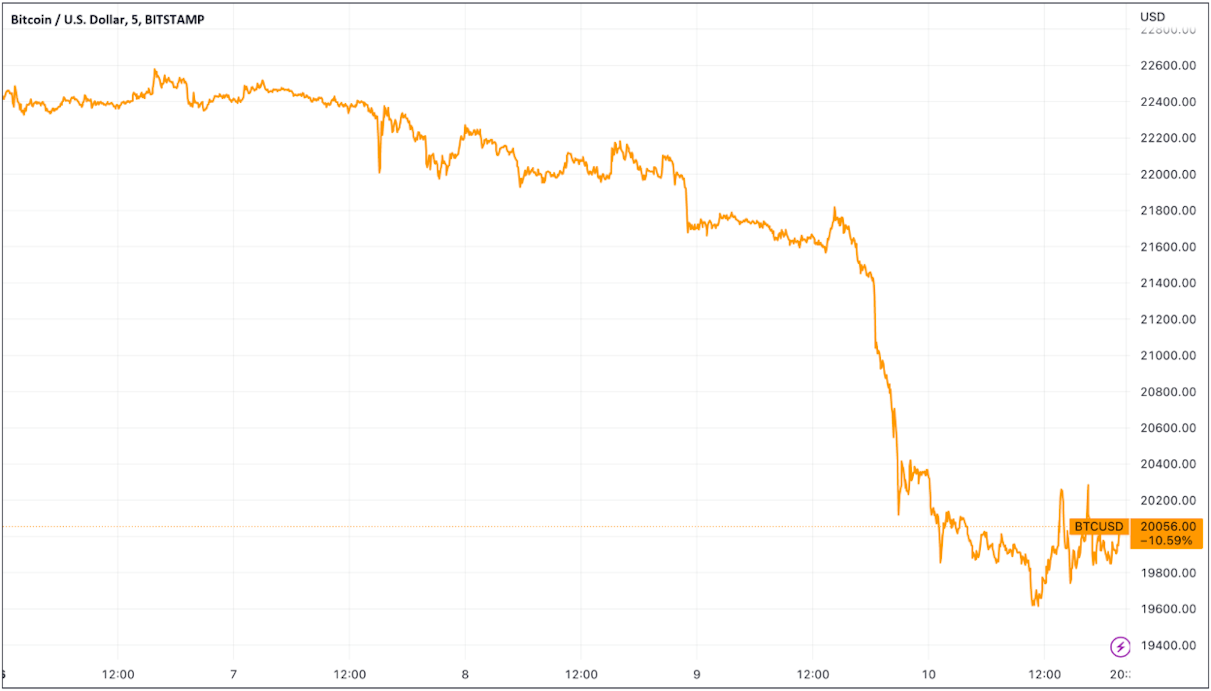

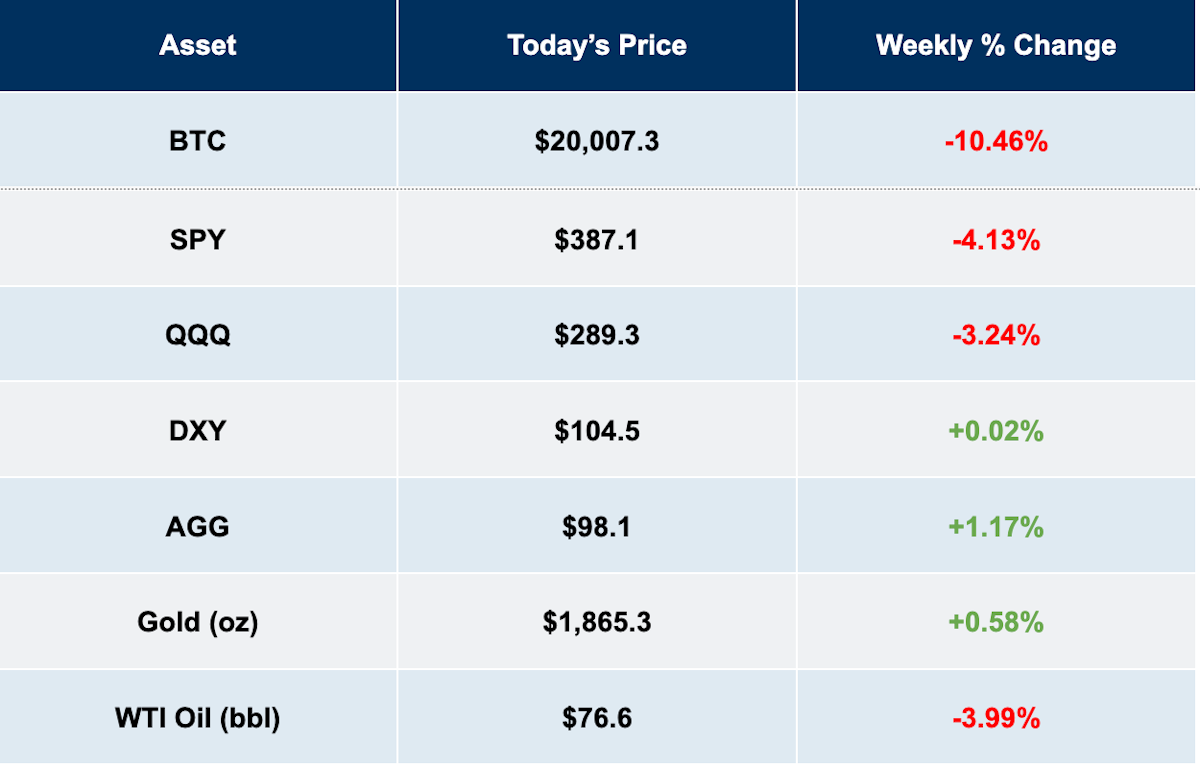

As the bank stocks sold off, so did Bitcoin, with Bitcoin falling -10.6% in the last 5 trading days.

All of these developments across the broader banking industry highlight the need for investors to own an asset that has no counterparty risk in these uncertain times. We saw in the Global Financial Crisis of 2008 how quickly counterparty risk can spread in the highly interconnected traditional financial system during a credit crisis. It’s important for investors to protect themselves against this risk.

When an investor holds Bitcoin in self-custody, there is no person or entity they have to trust to gain access to their savings. Bitcoin is sound money that you own when you hold your own private keys. No trust is required.

Bitcoin’s short-term price will continue to fluctuate with the global macroeconomic landscape and with changes in monetary and fiscal policy. But long-term, Bitcoin’s lack of counterparty risk is one reason why it remains an attractive asset to own in a diversified portfolio during these uncertain times.

Market Overview

Tradingview, Prices as of 03/10/23

Hold your IRA with the most trusted name in Bitcoin.

Sam Callahan is the Lead Analyst at Swan Bitcoin. He graduated from Indiana University with degrees in Biology and Physics before turning his attention towards the markets. He writes the popular “Running the Numbers” section in the monthly Swan Private Insight Report. Sam’s analysis is frequently shared across social media, and he’s been a guest on popular podcasts such as The Investor’s Podcast and the Stephan Livera Podcast.

Thoughts on Bitcoin from the Swan team and friends.

Some Coldcard hardware wallets were compromised due to false randomess. Learn which type of Coldcard users were affected and what custody alternatives exist.

A 50-day campaign to advance freedom and sovereignty through Bitcoin adoption