Buy Real Bitcoin, Not a Bitcoin ETF: Why Ownership Still Matters

A spot Bitcoin ETF tracks the price of Bitcoin. Owning shares is not the same as owning Bitcoin.

Since late March, I have publicly warned our clients and the broader Bitcoin community about the impending collapse of the cryptocurrency Luna and its native stablecoin, TerraUSD (UST).

Barely more than a month after I raised the alarm, Luna/UST went from a collective market capitalization of ~$50 billion to now down 99%. The collapse of the Luna/UST Ponzi scheme occurred even faster than I expected, but this implosion was perfectly predictable. This was not a Black Swan event. It was a White Swan event.

Several market participants, including myself, Lyn Alden, Kevin Zhou, and Adam Back, identified critical flaws in Luna/Terra’s mechanism design that made it susceptible to a hyperinflationary “death spiral.” Anyone who has studied the history of currency pegs understood where this trainwreck was headed. Furthermore, anyone who has seen other algorithmic stablecoins implode in the past, like Iron Finance or Luna founder Do Kwon’s previous failed attempt, Basis Cash, knew that this crash was inevitable given the intrinsic flaws of the Luna/Terra design.

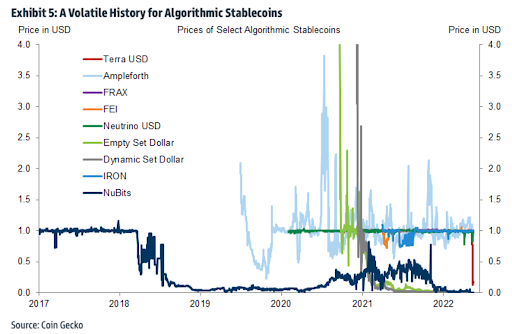

Decentralized algorithmic stablecoins are an oxymoron and an impossibility. As shown below, they have a history of being anything but stable, as they are always open to an attack.

As we continue to receive many questions about this, I decided to write this explainer about currency pegs, stablecoins, and the related risks they have on the broader cryptocurrency market. I hope it will clarify how and why the Luna/Terra Ponzi collapse happened, and what it means for Bitcoin moving forward.

But before we get into the Luna/Terra debacle, let’s start by looking at traditional currency pegs, why countries turn to them, and what risks can arise. By studying currency peg failures of the past, we can better understand how Luna/UST collapse was all but assured.

A currency peg is a policy where a nation pegs its currency at a fixed exchange rate to a foreign currency, a basket of foreign currencies, or an asset like gold to stabilize a local currency and promote the free flow of trade.

Currency pegs are common in emerging markets where local currencies are more likely to be unstable, making it more difficult for local business planning, investment, and trade. Currencies are primarily pegged to a more stable currency, such as the dollar or the euro, to create stability between trading partners and allow investors from developed countries to access smaller capital markets with decreased risk. Furthermore, a pegged currency can reduce volatility and exchange rate risk, allowing individuals and businesses to focus on their pursuits instead of worrying about the stability of their local currency.

Today about 20 countries have their local currencies fixed to the US dollar, with a famous example being the Hong Kong Dollar. Countries peg their currencies to the dollar because it is the world reserve currency, is widely used in international trade, and is the most stable compared to other fiat currencies. These currency pegs help import some of the stability of the dollar and also help to promote trade, but the hard part is not pegging the local currency; it’s maintaining the fixed peg as market dynamics change.

When a central bank commits to a currency peg to a foreign currency, they use foreign exchange reserves (FX reserves) to back the peg. FX reserves consist of assets denominated in a foreign currency such as deposits, bonds, Treasury bills, and other government securities.

If demand for the currency falls and the peg drops, then the central bank will buy its local currency by selling its FX reserves to support the peg. Suppose the peg rises as demand for the local currency increases. In that case, the central bank will release more of its currency into the market, increasing the supply and reducing the exchange rate. This is how a central bank maintains a fixed exchange rate in response to fluctuations in the supply and demand of its currency.

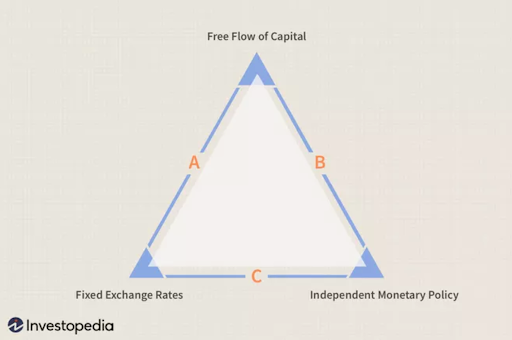

One important caveat with a fixed currency peg is that a pegging country must give up its monetary policy autonomy in order to stabilize its local currency and increase trade. This is often referred to as the Mundell-Fleming Trilemma or “the Impossible Trinity”. This trilemma explains a central bank’s options when it considers its monetary policy, it can 1.) set a fixed exchange rate, 2.) allow free flow of capital without a fixed exchange rate, or 3.) have an independent monetary policy.

The trilemma here is that you can only have 2 out of the 3 at any one time.

Mundell-Fleming Trillema

When Emerging Markets suffer from inflation and instability, many decide to peg their currency to a more stable currency (e.g., dollar, euro), while allowing for a free flow of capital, sacrificing their monetary policy autonomy in the process.

This becomes a problem when the economic conditions of the two countries in the currency peg scheme are not in sync. For example, if economic conditions in the US and a pegging country deviate, then applying US monetary policy can exacerbate the problems in the pegging country, exposing it to a currency peg that is too high or too low. In other words, in a fixed rate environment, a pegging country cannot independently dictate its monetary policy to respond to domestic economic conditions without threatening its currency peg. If a country has pegged its currency to the dollar, its interest rate policy has to follow the Federal Reserve’s policy, even if it harms its domestic economy.

This trilemma leads to inherent risks when a country has a fixed exchange rate with a foreign currency and then experiences deteriorating economic conditions domestically. They are limited in their tools to both protect the currency peg and respond to domestic economic shocks. To make matters worse, when a peg comes under pressure and the currency begins to depreciate, it opens the doors for opportunistic speculators to short the currency, which adds more inflationary pressures to the already weak currency. This dynamic can lead to a scenario where a currency peg breaks, the central bank runs out of its FX reserves to support the peg, the local currency depreciates rapidly, and a full-blown currency crisis ensues.

This is precisely what we’ve seen play out throughout history with fixed currency pegs. When asymmetric shocks and disparities between the economies of the currencies involved with a currency peg occur, we’ve seen the pegs fail spectacularly.

One of the most well-known examples of a currency peg failing is when George Soros “broke the Bank of England” in the early 1990s. The BOE had recently changed policy regimes and had fixed its currency at a new high rate. George Soros thought the British pound was overvalued and that the BOE didn’t have sufficient bank reserves to defend the new peg, so he built a massive $10 billion dollar short position on the British pound.

Soros was right. The BOE tried to support the currency peg and drained its FX reserves, but the FX reserves were insufficient. By the end of the ordeal, the British pound would devalue 25% against the dollar, and Soros would make over $1 billion on the trade.

Another example of a currency peg failing was the Thai baht in 1997, which sparked the Asian Debt Crisis. After four decades of economic growth, Thailand’s economy started to slow considerably. Due to the deteriorating economic conditions, the Thai baht faced pressures to depreciate. The central bank tried to defend the peg it had maintained for nearly a decade, but it was eventually abandoned. The baht would go on to lose 60% of its value against the dollar, leading to a rampant wave of currency speculation across Southeast Asia.

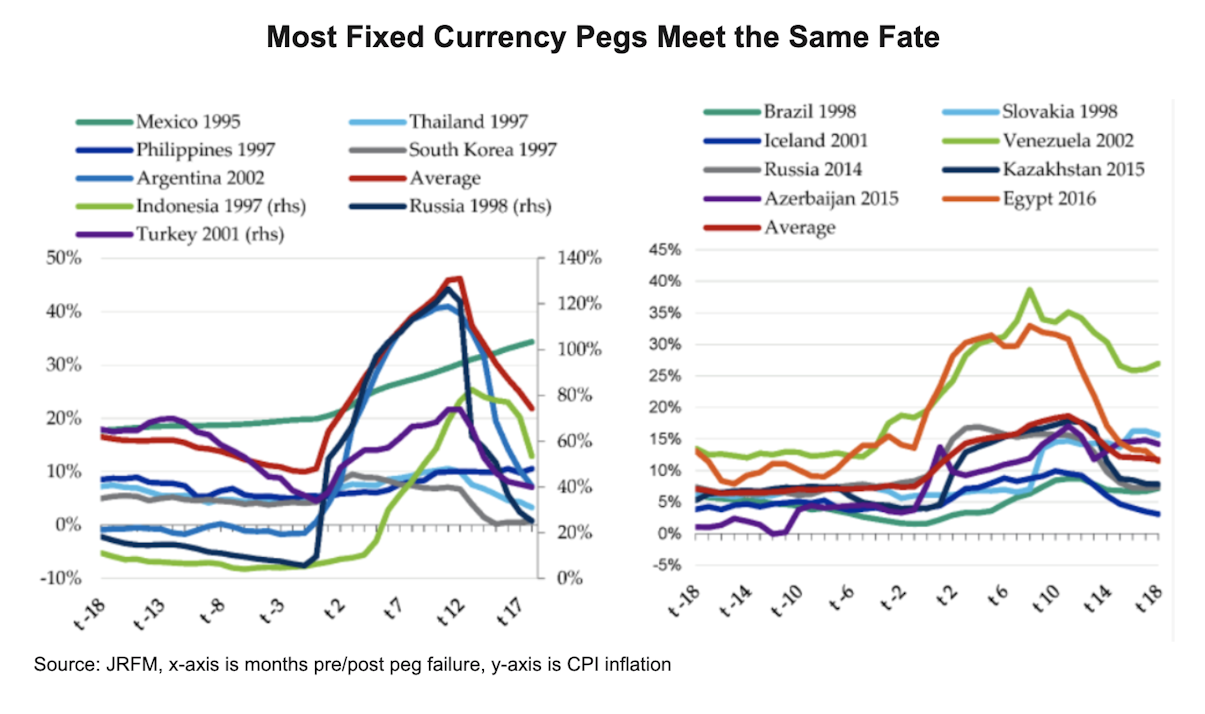

Those were two famous examples, but over the last several decades there have been many more instances of currency pegs breaking followed by rapid currency devaluations. The charts below show 16 times from 1995 to 2016 when currencies broke their pegs and suffered severe currency devaluations shortly after.

Most Fixed Currency Pegs Meet the Same Fate

The main takeaway here is that it’s extremely difficult, if not impossible, to maintain a fixed currency peg when the economies of the two linked currencies experience different challenges and asymmetric shocks. Central banks have struggled to maintain fixed currency pegs for decades, and have mostly failed. It’s folly to attempt to create artificial stability through a fixed currency peg in a world that is inherently unstable. It’s not a question of if a fixed currency peg will fail, but when. Despite this long track record of failure, some cryptocurrency founders think they can succeed where central bankers have failed — with stablecoins.

Stablecoins are best thought of as digital bearer assets that run on public blockchains that aim to peg their price to sovereign fiat currencies to inherit their price stability.

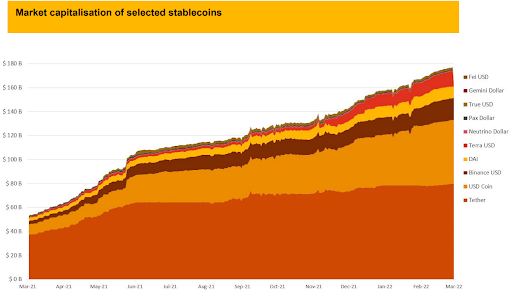

Over time, stablecoins have grown in both their usage and variety. According to Messari and Coingecko, the global stablecoin market reached nearly $175 billion dollars in March 2022, before UST imploded.

In the beginning, these stablecoins were primarily used by traders to take advantage of their lack of volatility when trading in/out of volatile native digital assets. Now stablecoins are used in emerging markets for people to gain access to dollars, and within various crypto protocols to facilitate leverage schemes disguised as financial innovation.

Stablecoins have experienced explosive growth over the past couple of years and from that growth, three different forms of stablecoins emerged:

Fiat collateralized — these are backed 1:1, typically by dollars or dollar-equivalent assets in a bank account. You can redeem these coins for dollars held in a bank account and vice versa. (ex: USDC, USDT)

Crypto overcollateralized — another digital asset backs these over the dollar amount of the stablecoin, and in return for depositing, a trader gets a minted stablecoin back. (ex: Maker DAI, BitUSD)

Algorithmic non-collateralized — no collateral backing; instead there is a stabilization mechanism in which the supply is expanded when the peg is too high, and the supply contracts if the peg is too low. (ex: UST, FRAX)

Stablecoins like USDT and USDC are theoretically fully backed 1:1 by assets in a bank account, so their pegs are much more stable. Other forms of stablecoins are not backed by fiat, and as a result, they are much less stable, and their pegs are more challenging to maintain.

Algorithmic stablecoins are the most experimental and risky of the group because the peg is not backed by anything at all but is rather actively managed by an algorithm that reacts to market forces (changes in supply and demand). This is the stablecoin category that Luna/Terra falls into.

The Terra algorithmic stablecoin system was designed as follows:

Luna was the governance token of the Terra system and acted as the collateral for the TerraUSD (UST) stablecoin. Terraform Labs (was the centralized foundation responsible for bootstrapping the system and providing liquidity when needed.

UST was designed to be redeemable for $1 dollar worth of Luna and vice versa. This was the mint/burn mechanism that would manage the supply of Luna/UST to maintain the $1 peg.

For example, if UST rose $0.10 above its peg, then market participants would be incentivized to burn $1 worth of Luna and mint 1 UST, collecting $0.10 profit, inflating the UST supply, and bringing down the peg back to $1 in the process. This also reduced the Luna supply, bolstering its price.

If UST dropped $0.10 below its peg, then market participants would be incentivized to burn 1 UST and mint $1 dollar worth of Luna. They then could choose to hold the redeemed Luna or sell it for $1 to collect the $0.10 profit. This would reduce the supply of UST and raise the peg back to $1.

These arbitrage opportunities are what incentivized market participants to maintain the Luna/UST peg…for a while.

Problems start to arise when the market cap of Luna does not keep up with the market cap of UST. If demand for UST outpaces Luna, and the price of Luna falls, then UST could become less “backed” by Luna, and the peg would be put at risk. In response to this design vulnerability, Terraform Labs had to incentivize UST holders to not redeem their UST for USD because, in that scenario, the peg would drop below $1, and arbitrageurs would be incentivized to defend the peg by burning more UST and minting more Luna, which would crash the price of Luna even more as its supply inflated. This dynamic would further put the Luna/UST peg at risk. It would create a feedback loop where UST and Luna investors begin selling in concert, creating a death spiral.

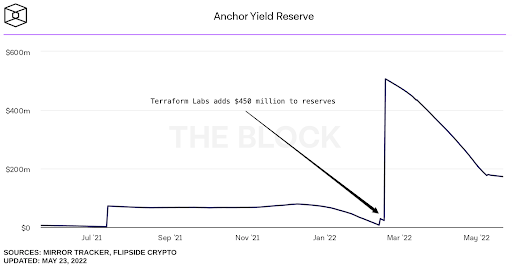

To overcome this, Terraform Labs created artificial demand for UST by offering a 20% yield on UST in the Anchor Protocol, which was also built by Terraform Labs. This yield was primarily funded by Terraform Labs through sales of their Luna token treasury. To avoid collapse, Terraform Labs would need to continually provide funds to the yield reserve to pay the 20% yield to UST holders so they wouldn’t burn their UST for Luna or USD. This occurred in mid-February when the yield reserve was topped off with a fresh $450 million dollars to continue the charade.

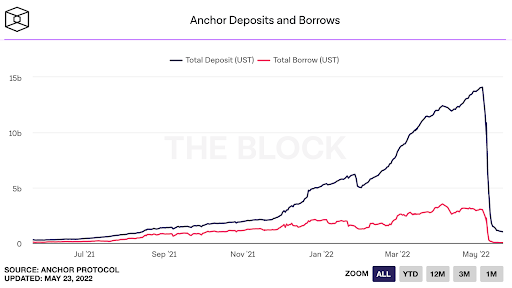

Before the attack, the peak total value locked inside the Anchor Protocol was over $14 billion. This was obviously not a sustainable operation. The yield reserves continually were being drained to fund the 20% Anchor UST yield to create demand for UST.

To make up for the rapidly expanding UST supply and the inherent fragility of the pegging mechanism, Terraform Labs created the Luna Foundation Guard (LFG) when it donated $4 billion dollars worth of Luna and raised $1 billion dollars in a private token sale led by Jump Crypto and Three Arrows Capital. LFG’s purpose was to buy large amounts of bitcoin as a defense mechanism in the case of an emergency. If market instabilities occurred and the peg became at risk, they would sell these bitcoin reserves to support the price of UST if the peg broke downwards, much like an Emerging Market central bank sells its FX reserves to support its currency peg if it breaks below the fixed exchange rate.

According to the Luna Foundation Guard, these were the assets in their reserve before the crisis began.

This Ponzi-like system was the perfect setup for an opportunist short seller who identified the weakness of the pegging mechanism and made a bet that Terraform Labs would not be able to defend the peg if it broke with substantial volume.

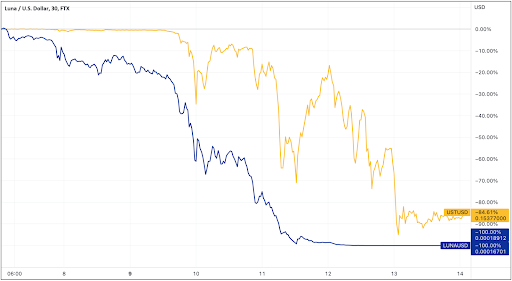

From April 7th to May 7th, things started to break down for Luna/UST when the general market took a downturn, and the price of Luna had dropped ~30% from $108 to $76 per coin.

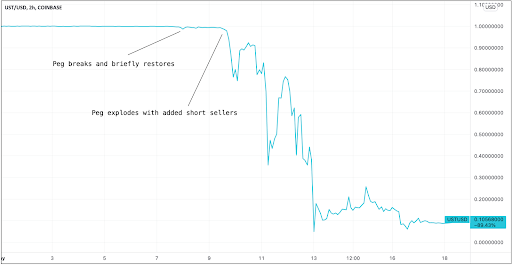

Due to the UST supply rapidly expanding from investors attracted to the 20% yield on Anchor Protocol, concerns emerged around Luna effectiveness as a collateral given its downward price action. This doubt led to investors selling UST due to fear that they would not be able to get full redemption value due to Luna’s price action. The peg initially broke on May 8th but was briefly restored.

This set the stage for an epic short opportunity. Similar to how George Soros bet against the Bank of England in the 1990s, a short seller bet that Luna/UST Ponzi was unsustainable and started to attack its peg. They first borrowed 100,000 BTC from a large exchange and went short. They then made a $1 billion UST deal OTC and systematically began selling UST, further putting pressure on the Luna/UST peg.

This led to a classic bank run in the Anchor protocol as investors all began trying to withdraw their UST from Anchor at once. Investors panicked, and billions of UST deposits were withdrawn from the Anchor Protocol in mere hours.

These panicked users withdrew their UST from Anchor, sold their UST, and redeemed it for Luna. Each user who sold then had a choice to make: 1) Hold onto their Luna, whose supply was rapidly inflating as the price was crashing, or 2) sell their Luna for dollars. Most chose the latter.

At this point, that same short seller began selling the rest of their UST holdings, some $650 million dollars worth. This caused the Luna/UST peg to break significantly, inciting even more panic. The result was a rapid decline in the price of Luna to the point where UST was now no longer fully collateralized by Luna. A classic death spiral then ensued as investors ran for the exits and the price of Luna and UST fell simultaneously.

It was here that LFG stepped in by allegedly selling their Luna and Bitcoin reserves to buy up UST in an attempt to stop the bleeding. However, as the price of Luna and UST fell, so did the price of Bitcoin as the LFG allegedly sold tens of thousands of their bitcoin. (Note: It is still unknown if they actually sold the bitcoin).

In the end, LFG’s efforts were a lost cause. Like emerging markets that drain their reserves when trying to support their fixed currency peg, LFG drained its funds, but it was not enough, and the peg still collapsed.

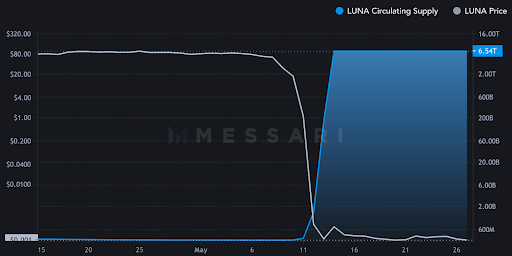

As investors continued to sell UST in droves, this minted more and more Luna. This led to a hyperinflation event where the Luna supply increased rapidly in one day. Jimmy Song wrote this thread that reported on Luna’s hyperinflation in real-time. As a result, the supply of Luna went from around 725 million to 6.9 trillion, or almost a 1,000,000% increase, in one day.

At this point, the gig was up. Luna had suffered a hyperinflationary event for the ages, the peg had collapsed entirely, and ~40 billion dollars worth of market value was destroyed in days.

New details surrounding the Luna/UST crash continue to come out every day. There are reports of retail investors losing life savings, firms reporting massive losses, founder Do Kwon is being fined $78 million for alleged tax evasion, and there are multiple ongoing investigations alluding to evidence of large whales who dumped their positions on retail investors. Also, many unknowns still remain around whether or not LFG actually sold the bitcoin in their reserves, or if management retained possession of the bitcoin.

This Twitter account is currently digging into investigations around the Luna/Terra crash. I suggest following along for updates on the situation. I do not think we have heard the end of this story, and I believe more allegations will emerge about the operators and major investors of this giant Ponzi scheme. Meanwhile, the founders of Terra Luna are at it again. They are currently attempting to resuscitate the failed project by launching Terra 2.0. Why anyone would invest their money with these people again is beyond me.

Unfortunately, the mom-and-pop investors are usually the ones left holding the bag in these events. Many of the large firms that invested in and marketed this coin were able to exit before the crash occurred, escaping with massive profits. Strangely, some of these whales felt the need to share this in their comments following the crash. Pantera Capital CIO Joey Krug admitted that they had sold 80% of their Luna position before the crash. Furthermore, Pantera Capital partner, Paul Veradittakit, seemingly bragged that they had turned their $1.7 million dollar Luna investment into around $170 million dollars. Galaxy Digital CEO, Mike Novogratz, wrote in a letter that Galaxy had “booked profits along the way” before the Luna collapse happened. They pumped an obvious Ponzi, and got out before the collapse. Either they knew it was a Ponzi and booked hundreds of millions of illegitimate profits, or they were too ignorant to see the obvious Ponzi dynamic and shouldn’t be managing anyone’s money. There’s no third option. From their own commentary, it appears they knew exactly what game was being played here, but simply did not care about the retail investors who would be burned in the process.

We will see what investigations reveal down the road regarding these major investors and insiders involved with the Luna/UST crash. In the end, the short seller who played a significant role in collapsing the Ponzi scheme is rumored to have walked away with over $800 million dollars in profits from the trade.

This White Swan event is precisely why we actively warn the public about risks associated with other cryptocurrencies like Luna/UST that are marketed as promising by their promoters. A vast majority of these other “cryptos” have increased operational, security, and regulatory risks, and have centralized teams that control them. This becomes evident in the event of a catastrophe when their “crypto” turns out to be decentralization theater. Sophisticated investors involved in private token sales buy tokens at dirt cheap prices, advertise them as decentralized and secure to retail investors, pump the price up, and dump the tokens on them, making massive profits.

This unfortunate event further highlights the fundamental differences between Bitcoin and every other cryptocurrency. There are no private token sales or complex yield schemes involved in Bitcoin. Only Bitcoin is decentralized. Only Bitcoin is leaderless. Only Bitcoin is secure. Only Bitcoin has proven to maintain its value over the long term.

The ramifications of the Luna/UST blowup will likely have long-term consequences for the broader crypto and stablecoin industry. The SEC already doubled its crypto enforcement team last month and specifically mentioned the risk of stablecoins and DeFi as part of the reason.

With stablecoins, we see run risks, which could threaten financial stability, risks associated with a payment system and its integrity and risks associated with increased concentration if stablecoins are issued by firms that already have substantial market power,…We definitely see significant risks.

US Treasury Secretary

This Luna/UST fiasco will likely bring the industry under regulatory scrutiny in an effort to protect retail investors. It’s important that regulators create a responsible regulatory framework that does not stifle innovation or conflate Bitcoin with the rest of the broader cryptocurrency industry.

The truth is the history of currency pegs foreshadowed what would occur with Luna/UST. From the Bank of England to the Bank of Thailand to now Luna/UST, fixed currency pegs are nearly impossible to maintain in this highly complex and rapidly changing world. It was a mixture of hubris, arrogance, greed, and ignorance that led this doomed idea to get off the ground in the first place. We are fortunate the scheme blew up before it grew larger and became more of a systemic risk.

Hearing the stories of retail investors losing their life savings has left a bad taste in the mouths of many people, both Bitcoin supporters and critics alike. As a member of the Bitcoin industry, I will continue to warn people of the risks of the broader cryptocurrency industry to help preserve their wealth and help them avoid these outcomes. The risk of a major stablecoin blowing up is now behind Bitcoin. It has survived another exogenous threat, and it will continue to do precisely what it was designed to do since its very first block.

Swan Bitcoin provides recurring buys, savings plans, instant buys, Private Client services for businesses and HNWI, Advisor services for financial advisors, and world-class Bitcoin education.

Cory Klippsten is the CEO of financial services firm Swan Bitcoin. He is a partner in Bitcoiner Ventures and The Bitcoin Opportunity Fund, and as an angel has funded more than 50 early stage tech companies. Before startups, Klippsten worked for Google, McKinsey, Microsoft and Morgan Stanley, and earned an MBA from the University of Chicago. He grew up in Seattle, split 15 years between NYC and Chicago, and now lives in LA with his wife and daughters. His hobbies include basketball, history and travel (Istanbul and Barcelona are favorites).

Sam Callahan is the Lead Analyst at Swan Bitcoin. He graduated from Indiana University with degrees in Biology and Physics before turning his attention towards the markets. He writes the popular “Running the Numbers” section in the monthly Swan Private Insight Report. Sam’s analysis is frequently shared across social media, and he’s been a guest on popular podcasts such as The Investor’s Podcast and the Stephan Livera Podcast.

News

More NewsThoughts on Bitcoin from the Swan team and friends.

A spot Bitcoin ETF tracks the price of Bitcoin. Owning shares is not the same as owning Bitcoin.

Live video verification, Jade Plus signing devices, and a purpose-built recovery assistant give families and businesses greater control over their Bitcoin.

Passkeys enable faster, more secure device-based logins (face/fingerprint) that reduce password risks and strengthen our Swan Guard security protections.