Swan Private Insight Update #22

This report was originally sent to Swan Private clients on April 14th, 2023. Swan Private guides corporations and high net worth individuals globally toward building generational wealth with Bitcoin.

In 2017, an unregulated offshore cryptocurrency exchange burst onto the scene, rapidly ascending as a dominant force within the crypto industry. It offered a range of products and hundreds of different cryptocurrencies and even launched its own token, which has since “gone to the moon.”

This report was originally sent to Swan Private clients on April 14th, 2023. Swan Private guides corporations and high net worth individuals globally toward building generational wealth with Bitcoin.

Fast forward a few years, and the exchange is bringing in hundreds of billions in profits as the crypto frenzy takes hold. A charismatic founder leads the exchange. He enjoys frequent appearances on cable news shows and his net worth surges to tens of billions during the crypto bubble. At its peak, rumors circulate that he occupies the 11th spot among the world’s wealthiest individuals. However, many believe his immense wealth couldn’t be entrusted to better hands. The founder is celebrated for his commitment to effective altruism, pledging to donate 99% of his fortune to charitable causes. He proudly showcases his exchange’s philanthropic initiatives, and its logo garners worldwide recognition, adorning various sponsored sports teams. Enthusiastic fans eagerly anticipate the innovative products this trailblazing company will introduce to realize its founder’s vision of a “decentralized financial system.”

Sound familiar? You’re not alone if you immediately thought of FTX and Sam Bankman-Fried. The striking similarities between Binance, led by its founder Changpeng Zhao (CZ), and FTX are undeniable.

The most significant distinction between the two exchanges, besides the fact that FTX is no longer operational, is the sheer size of Binance compared to FTX. Binance firmly holds the title as the world’s largest cryptocurrency exchange in terms of trading volume, boasting an estimated user base of over 100 million. Moreover, FTX’s demise further consolidated Binance’s position, driving additional market share in its direction as an alternative offshore exchange offering comparable products and competitive fees. Presently, Binance commands over 50% of the total crypto market share by trading volume.

Kaiko Exchange Volume Data

But how did Binance grow into such a behemoth of the cryptocurrency world?

As you’ll read below, much of Binance’s meteoric ascent can be attributed to its seemingly flagrant disregard for the law. As users and revenues poured into the exchange, propelling its growth, numerous allegations, investigations, and regulatory actions shadowed its progress. Over time, it has become increasingly evident that the exchange’s business practices provide enough circumstantial evidence to warrant caution among users and investors.

Throughout its history, Binance has demonstrated a remarkable ability to evade regulators and sidestep the law. It has undoubtedly benefited from the regulatory arbitrage inherent in this emerging asset class; however, it now seems that these questionable business practices are beginning to catch up with the giant crypto exchange.

Buy automatically every day, week, or month, starting with as little as $10.

Just last month, the CFTC filed a civil lawsuit against Binance, accusing it of illegally offering trading products to US customers. This lawsuit coincides with a four-year investigation by the DOJ and IRS into Binance for potential violations of anti-money laundering laws and sanctions.

For those who have been paying attention, these regulatory actions and investigations should not come as a shock. Binance has been raising eyebrows since its inception in 2017.

In this article, we will underscore some of the red flags that users should consider before entrusting even a single dollar of their savings to this offshore exchange. We will look at Binance’s inauspicious beginning, the centralization of its proprietary token and blockchain, its dubious listing practices, and revelations from the recent CFTC lawsuit.

While we rely solely on publicly available information, inevitably resulting in some speculation, a thorough examination of Binance’s suspicious behavior patterns, pervasive adverse incentives and dubious track record can help illuminate the risks associated with this global cryptocurrency exchange.

The origin of Binance dates back to 2017, amidst the Initial Coin Offering (ICO) boom. ICOs were celebrated as a new fundraising method that enabled projects to raise capital by issuing and selling their own cryptocurrency tokens to investors.

At the time, ICOs gained popularity, being hailed as a revolutionary fundraising mechanism. However, in retrospect, ICOs are now synonymous with fraud, as a majority of them proved to be little more than pump-and-dump schemes and blatant scams. Despite this, Binance was able to capitalize on the ICO frenzy and performed its own ICO at the perfect time, right before ICOs faced intense regulatory scrutiny and investors began to realize their fraudulent nature.

Legend has it that CZ first learned about ICOs at a potluck dinner in the summer of 2017. Seeing this as an easy opportunity to raise funds for his exchange, he quickly moved to launch his own token, which he dubbed BNB. In a mere three days, the BNB whitepaper was written. Nine days later, the ICO for BNB commenced. Within a week, CZ had effortlessly raised $15 million.

A total of 200 million BNB tokens were issued during the ICO. Like most ICOs of the time, 40% of the tokens were allocated to the founding team themselves for further developments and marketing efforts.

Binance White Paper

Binance’s reasoning behind issuing such a large share of the tokens to the team is highlighted below.

Funds Usage

35% of the funds will be used to build the Binance platform and perform upgrades to the system, which includes team recruiting, training, and the development budget.

50% will be used for Binance branding and marketing, including continuous promotion and education of Binance and blockchain innovations in industry mediums. A sufficient budget for various advertisement activities, to help Binance become popular among investors, and to attract active users to the platform.

15% will be kept in reserve to cope with any emergency or unexpected situation that might come up.

In the white paper, it is stated that the purpose of the raise was to bootstrap the company into becoming a “world-class crypto exchange.” Investors of BNB tokens bought them anticipating that they would gain in value as Binance grew, and due to the “tokenomics” around the token itself including:

BNB token holders received a discount on fees on the platform.

Every quarter, Binance would use 20% of its profits to buy back BNB and burn them, reducing the supply.

BNB would be used to pay fees on Binance’s future decentralized platform, Binance Chain, once it was built.

When Binance issued BNB, it immediately raised eyebrows because it looked a lot like security to many market participants as defined by the Howey Test.

The Howey test is used to determine whether an offering qualifies as an investment contract and therefore is a security under federal securities laws. It’s hard to argue how Binance’s ICO of BNB wasn’t an illegal security offering.

Here are the four prongs of the Howey Test:

An investment of money (ICO) ✅

In a common enterprise (Binance) ✅

With an expectation of profits (BNB tokenomics) ✅

Derived from the efforts of others (Binance) ✅

If a transaction satisfies these four criteria, it is deemed an investment contract and a security, falling under the purview of federal securities regulations. These regulations mandate registration and disclosure requirements with the SEC. Despite BNB’s striking resemblance to a security, Binance refrained from taking any of these necessary steps. Instead, they proceeded to issue the token and were off to the races.

When CZ was asked whether or not BNB was a security on a podcast in 2018, this was his response.

“No. It’s actually not a company coin. The Binance coin itself lives on the blockchain. Right now, it lives on the Ethereum blockchain, but very soon we will have our own blockchain that is also a decentralized platform. It’s not a coin by the company. It’s still a community. We are the issuers. We have issued it, and people have bought, and it has been spread out. We do hold a large number of it, but we will not be able to issue anymore. So we no longer have a lot of control on the coin. What we could control, as we are the very large holders of the coin, is we are financially incentivized to make the coin worth more. We are very encouraged to do that. We don’t promise returns. But we are working hard to increase the value of Binance coin.” — CZ

This statement was quite shocking to come across. In it, CZ says that even though they issued the tokens, it is not a company coin because it “lives on the blockchain that is also decentralized.” He then goes on to say that because the tokens are distributed, they do not have control. Finally, he says that they are incentivized to “make the coin worth more” and are “working hard to increase the value of Binance coin.”

While I am not an attorney, my understanding of federal securities law leads me to believe that CZ essentially outlined the Howey Test as it pertains to BNB. It should come as no surprise then that, as of June 2022, the SEC is currently probing whether the BNB ICO should have been registered with the agency as a security.

So Binance was likely bootstrapped through the issuance of an unregistered security (BNB), but let’s entertain the possibility that CZ is correct. Let’s assume that BNB’s existence on a decentralized blockchain and its distribution among holders render it beyond their control. But is this really accurate? Is BNB decentralized and, thus, outside Binance’s control?

Initially, BNB was issued as an ERC-20 token on the Ethereum blockchain. However, in 2019, Binance launched its own rival blockchain, dubbed the Binance Chain. Currently, around 137 million BNB tokens reside on the Binance Chain, while 16.5 million BNB are still on Ethereum.

According to Binance, the primary motivation for launching its own blockchain was to create a blockchain specifically designed for speed and scalability. Ethereum is infamous for its sluggishness and susceptibility to congestion during periods of high volume. Binance wanted to fix that. The problem is there are inherent trade-offs when designing a blockchain. This is commonly referred to as the “Blockchain Trilemma.”

The Blockchain Trilemma highlights the difficulty in simultaneously achieving the three most desirable properties of a blockchain: scalability, security, and decentralization. Consequently, designers are often compelled to prioritize one or two of these attributes over the others.

In the case of Binance Chain, Binance clearly aimed to build a blockchain meant for speed, and in doing so, sacrificed decentralization and security. This was acknowledged by CZ himself in his 2020 New Year Message.

“BNB Chain/DEX is definitely less decentralized than Ethereum…The code is not fully open-source, yet. And there is a limited number of validator nodes for performance reasons. But you do control your private key. In the worst case, the validators could collude and shut down the network, but there is a more than a decent chance that the community will bring it back up again. In any event, no one ever has your keys.” - CZ

Binance’s stated objective was to gradually decentralize Binance Chain as more validators joined the network and the ecosystem expanded. The initial high centralization was meant to be temporary during the product’s launch phase.

In September 2020, the BNB, now mainly on the Binance Chain, fueled the launch of the Binance Smart Chain (BSC), and Binance Chain was rebranded to Beacon Chain. Beacon Chain is used for governance and decision-making platforms, and BSC is used for smart contract functionality and building decentralized applications.

By February 2022, the two chains came together to form the BNB Chain, which consisted of the BNB Beacon Chain and the BNB Smart Chain.

In a blog post, Binance declared that its original goal of decentralization had finally been realized with the creation of BNB Chain, and that Binance now has no longer exercised control over the protocol.

“BNB Chain was originally initiated by Binance but has since grown to become a community-driven, permissionless, and decentralized blockchain ecosystem. Binance is now simply one of the many contributors operating within the BNB Chain ecosystem rather than some kind of dominant force wielding unilateral power over it.”

But the claim that BNB Chain is decentralized starts to unravel when we examine its underlying structure and governance more closely.

To begin with, the BNB Chain uses a consensus mechanism called Proof of Staked Authority (PoSA) for transaction validation and network governance.

In this system, a validator must undergo a strict vetting process by Binance before being allowed to validate transactions and generate new blocks. Once approved, users can delegate their BNB tokens to these validators, who then share block rewards with their delegators.

In a standard Proof-of-Stake system, token holders stake their tokens and exert influence based on the amount they stake. However, with Binance’s approach, BNB token holders delegate their tokens to trusted third-party validators vetted by Binance.

This is where the issue arises. In Proof-of-Stake protocols, users can stake their tokens and become validators, thus influencing the protocol’s governance. But with Binance’s consensus mechanism, a centralized company, Binance, authorizes who becomes a validator. This necessitates obtaining permission from Binance to access the BNB Chain validator set — a far cry from a permissionless system.

So how many of these BNB Smart Chain validators are there today?

21 — There are only 21 active BNB Chain validators (Let the decentralization wash all over you).

Adding to the concern, Messari’s Wilson Withiam found that these 21 BNB Chain validators are determined daily by the BNB Beacon Chain validator set, which is even more centralized, governed by a mere 11 validators.

Worse still, Withiam discovered that most validators in the BNB Chain ecosystem are either directly managed by Binance or have close relationships or partnerships with the company.

Messari

This evidence demonstrates that BNB’s structure is far from the decentralized system Binance claims it to be, but rather one that is governed directly by Binance itself.

The centralized nature of BNB Chain became evident when BNB Chain suffered a hack last October to the tune of $566 million. In response to the exploit, 19 validators of the BNB Chain halted the supposedly “decentralized” blockchain.

If a blockchain is decentralized, it is immutable. That’s kind of the whole point. A genuinely decentralized blockchain allows anyone to view the entire history of transactions with confidence, knowing that the records have not been manipulated or tampered with. This coordinated shutdown by validators exposed the true extent of BNB Chain’s centralization. Shutting down and subsequently relaunching a blockchain becomes considerably easier when a single, centralized entity like Binance controls the majority of validators. Decentralization always reveals itself in a time of crisis.

The real reason this is a problem is it gives Binance the ability to influence the protocol in which they either directly own or have custody of a significant majority of the token’s circulating supply.

Unfortunately, this may have been precisely what transpired. Cryptohippo conducted some incredible investigative work, uncovering an abnormality in the BNB Beacon Chain. He found that the fourth largest wallet holding 22 million BNB ($6.9 billion), had no transaction history on the blockchain whatsoever.

The Chief Scientist of Binance responded by saying that this wallet was a “Staking Escrow Wallet,” but that still doesn’t explain why the 22 million BNB deposited doesn’t have any transaction history.

Another independent researcher, Data Finnovation, took the work a step further and tried to sync the BNB Beacon Chain from the genesis block, and the node received an error. It failed to validate the blockchain. He then tried again, and the error came again, just at a different block.

The author’s main conclusion was, “It is no longer clear BNB Beacon Chain should properly be called a blockchain, as there are issues with the process where ‘blocks are chained’ such that ‘the work to change the block would include redoing all the blocks after it.’

His findings from an attempt to sync a node to the BNB Beacon Chain revealed that it essentially breaks every 24 hours, and yet the “blockchain” continues to operate. Weird! It can do this because of a “state recovery tool” that Data Finnovation discovered, which edits the hash histories of the blockchain each time it malfunctions, effectively rewriting the transaction history. Consequently, the entity rewriting this history exercises control over the blockchain’s operation, making it less of a genuine blockchain and more of a centrally-controlled database that breaks every 24 hours, with its history having to be unilaterally rewritten by a centralized party.

At the very least, these suspicious activities on the BNB Beacon Chain “blockchain” demonstrate that it is not decentralized like Binance markets it to be. At its worst, it may suggest tampering with the transactional history of the BNB Beacon Chain, which could potentially obfuscate other nefarious activities. This could explain the mysterious appearance of 22 million BNB in the fourth largest wallet without any history of the deposit transaction on the BNB Beacon Chain.

At the heart of the FTX fiasco was the issuance of its own token, FTT, which enabled the company to inflate its balance sheet. By controlling the liquidity of the FTT token on the exchange, FTX could inflate the price to astronomical levels, resulting in the company’s valuation skyrocketing. This attracted additional funding from venture capitalists, allowing FTX to expand and increase its influence.

The company even used FTT tokens as collateral for loans to acquire dollars, which were then spent on various investments ranging from crypto startups to beachfront properties in the Bahamas.

Binance followed a similar path, offering its own exchange token, BNB, with over 40% of the supply allocated to the founding team. Upon examining Binance’s strategy over time, it becomes evident that most actions are centered around pumping the price of BNB.

This makes sense since Binance itself is the largest holder of the token. Consequently, they actively drive value to BNB through use cases, incentives, and strategic implementations. Users receive trading fee discounts when using BNB, BNB is utilized as gas on the BNB Chain, and users can stake BNB for yield on the platform.

The most blatant method Binance employs to boost BNB’s price is through its burn program. In the ICO white paper, it states, “Every quarter, we will use 20% of our profits to buy back BNB and destroy them until we buy 50% of all the BNB (100MM) back.”

In an interview in 2018, CZ stated, “This [burn mechanism] is similar to a dividend but instead of sending money out, we destroy coins we have.”

But then, in January 2020, Binance secretly changed the wording in the original white paper regarding the burn mechanism, which now reads, “Every quarter, we will destroy BNB based on the trading volume on our crypto-to-crypto platform until we destroy 50% of all the BNB.”

This change raises questions about Binance’s intentions—perhaps linking the burn mechanism to trading volume would result in more significant burns and higher price appreciation for the token, of which they hold a majority?

But how much BNB does Binance actually hold? In the wake of the FTX collapse, Binance came under intense scrutiny and demanded an independent audit to ensure all user funds were backed on the exchange.

In a now-famous interview on CNBC, the anchor asked CZ if Binance could handle it if someone asked you for $2.1 billion back; CZ dodged the question, responding with, “We are financially ok. We’ll let the lawyers handle it. We are financially strong.”

What followed was not a full independent audit as was requested, but rather a Proof of Reserves report from Binance’s auditing firm Mazar’s Group, which gave an incomplete snapshot of the exchange’s balance sheet. Mazar’s Group eventually deleted the Binance Proof of Reserves from its website and later suspended all business with cryptocurrency firms.

Nic Carter, who has studied Proof of Reserves for years, ranked Binance’s Proof of Reserves as the worst report compared to other exchanges in terms of the methodology used.

Nic Carter

This report raised more questions than it answered regarding the composition of Binance’s balance sheet. But what the proof of reserves did reveal was the amount of BNB held in user-controlled wallets, with 16.5M BNB on ETH and 6.5M BNB on BNB Smart Chain. By the process of elimination, we can deduce the percentage of the BNB circulating supply held in wallets controlled by Binance.

Cryptohippo once again did the hard work, tracking down addresses controlled by Binance, and calculated that 67-81% of all BNB — equating to over 131 million BNB tokens — are held in BNB Beacon Chain wallets controlled by Binance, which were not included in the published Proof of Reserves. The graphic below shows the BNB addresses managed by Binance on the Beacon Chain, including the mysterious 22 million BNB wallet with no transaction history.

Cryptohippo

These findings shed light on how Binance holds a significant majority of the BNB circulating supply on its balance sheet in wallets they control. Just like FTX, this creates a conflict of interest and makes one wonder if Binance has acted to manipulate the price of BNB to benefit its own business.

The similarities in the price action of BNB and FTT certainly raised a lot of eyebrows. Both tokens exploded in price. You can see below how both tokens exploded in price and had similar chart patterns before FTT collapsed to zero.

We know that FTT ended up being manipulated by the issuer and exchange operator. Only time will tell if Binance is pulling similar shenanigans with BNB. Still, the incentives are evident, considering how critical the price of BNB is to Binance’s success and the fact that it holds a large amount of BNB on its own balance sheet.

When Binance burst onto the scene in 2017, it attracted new users at an astonishing rate. It reportedly took the platform three months to gain 120,000 users, another three months to reach one million, and a week later, they hit two million. But how did they accomplish this?

One strategy that Binance used to differentiate itself from competitors is it gave a platform to a wide variety of cryptocurrencies. Binance listed every token under the sun. If a user wanted to trade some obscure token, odds are they could find it on Binance.

By the end of 2018, 151 coins were listed on Binance (up from 101 at the start of the year). To put that in perspective, by the end of 2018, Coinbase had 9 cryptocurrencies listed (up from 4 to start the year).

This led to many accusations that Binance lacked internal policies and procedures in place to ascertain whether a token they listed was an unregistered security or an outright scam.

Binance has been consistently vague about its listing policies. When asked about it in a podcast in 2019, CZ remarked,

“If we don’t fully disclose that because people will engineer that, and we change that all the time anyway, we don’t follow one standard process. At the end of the day, we just want to list new coins. How much for listing do we charge? Well, it changes with every case as well.”

- CZ

The point here is that Binance is incentivized to list as many tokens as possible to collect fees and drive revenues, regardless of the security status or legitimacy of the tokens.

Binance’s legal review process for listing tokens involved asking the token projects to hire a lawyer to confirm that the token was not a security. This creates a conflict of interest since the lawyer is selected and paid by the token team that wants their token listed. A better approach would be for Binance to hire its own legal team to conduct a legal review and charge the team the lawyer fees. But they chose not to do this.

It’s obvious why these token projects would want to get listed on Binance. A recent analysis found that token prices jump on average +73% in the first 30 days following their listing on Binance.

CZ noted the benefits of a token getting listed on Binance in another podcast interview,

“We provide such value for these coins. We give them liquidity, our large user base, and provide them with credibility because they passed the Binance review. It’s worth way more. None of the projects we list complain about it at all. They never say we paid too much in listing fees.”

- CZ

Considering the sheer amount of coins Binance listed and the fact that they asked the tokens project themselves to hire a lawyer for legal review, it’s hard to understand the “Binance review” that CZ refers to.

Binance’s primary goal is to list as many tokens as possible to rake in the listing fees — full stop. In another podcast from 2018, CZ gave a range of what those fees are.

“I know that there is no one set price if I want to have my token listed on Binance, but what is the range of fees I might pay for that? It is usually around a couple of hundred thousand dollars, to be honest.”

- CZ

But Binance didn’t stop with just listing seemingly every token that came to them, they had to find a way to pump BNB, and so they pioneered a new way to list a token through an Initial Exchange Offering via the Binance Launchpad.

Binance Launchpad is a platform that allowed projects to raise funds and launch their token project directly on the Binance platform. The token sale occurred directly on Binance, and users are typically required to use BNB to participate in the token sale.

So far, 68 projects have been launched through Binance Launchpad for a total of $119 million raised.

Binance.com

Launchpad serves as yet another example of how Binance will do anything to pump the price of BNB at every opportunity.

Binance emerged as a clear winner when it came to listing a plethora of tokens during the ICO boom of 2017 and 2018. But the losers were the retail investors. These users bought tokens that received the “Binance seal of approval” and were falsely marketed to them as “the next big thing.” Many of these cryptocurrencies are down -90% from their all-time highs and will never recover.

In April 2020, these practices led to a class-action lawsuit filed with the Southern District of New York, with Binance and CZ named as defendants. The case read, “How did a company [Binance] barely a year old generate such extraordinary profits? By building a platform that solicited the buying and selling unregistered securities at a historically unprecedented scale.” While a class-action lawsuit does not equate to guilt, it does highlight the consequences and victims resulting from Binance’s questionable listing practices in pursuit of its meteoric growth.

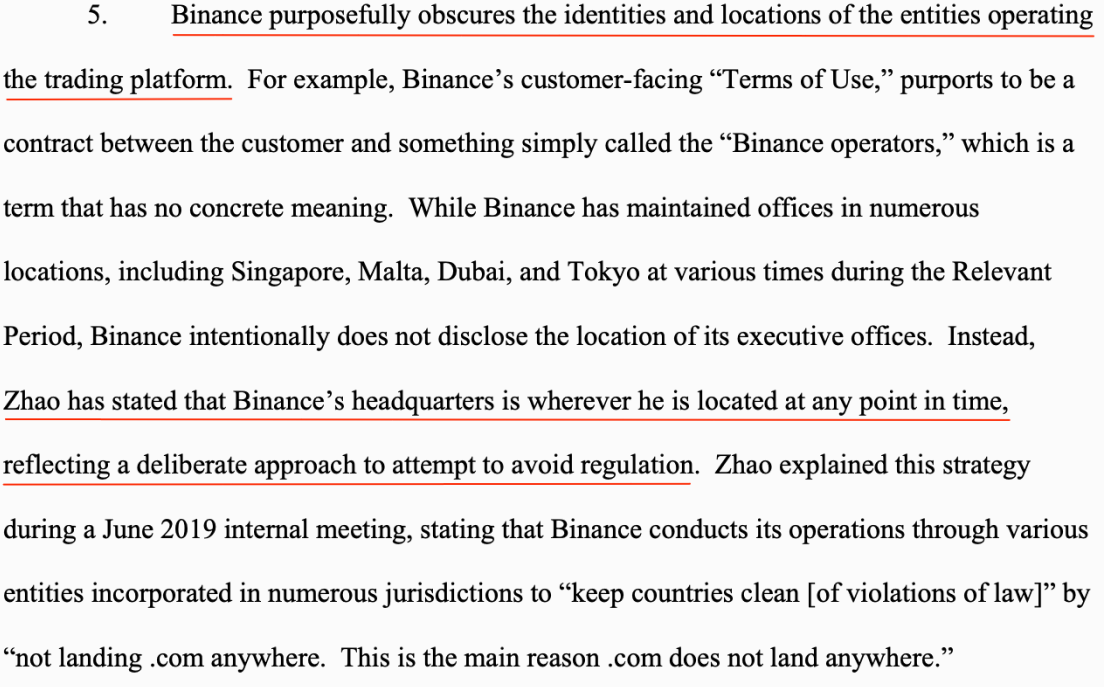

One of the critical factors that enabled Binance to rise as the world’s leading crypto exchange was its ability to evade regulators by not establishing a fixed headquarters in any specific jurisdiction. Initially, Binance was based in China, but it relocated its servers to Japan shortly before China’s crackdown on crypto exchanges. Japanese regulators then issued a warning to Binance, stating that it was operating without a license, which prompted Binance to move to Malta in 2018. In February 2020, Malta’s financial regulators clarified in a statement that Binance was not licensed to operate within the country.

The precise location of Binance’s operations today remains uncertain. A holding company is situated in the Cayman Islands, and at least 73 entities controlled by CZ exist globally, but he refuses to disclose which entity is responsible for the main exchange.

Reuters reporting, corporate filings, Binance documents

Even though Binance doesn’t reside in one jurisdiction, this has not stopped market participants from all over the world from accessing the website. As a result, regulators globally have to issue warnings and impose restrictions on their citizens regarding the use of Binance.

This noncompliance with financial laws lies at the heart of the recent CFTC lawsuit against Binance in the U.S. In the lawsuit, the CFTC outlines how Binance has deliberately evaded US regulations by concealing the location of its headquarters.

When Binance first launched, it showed little concern for the financial laws that govern the United States’ financial markets. It did not register with any regulatory entities and failed to adhere to the necessary requirements before allowing U.S. customers to access its website. This persisted until September 2019, when Binance notified U.S. users that it would no longer provide services to them following increased regulatory scrutiny. Subsequently, Binance launched Binance.US, asserting it was an independent entity designed to comply with the U.S. regulatory requirements.

Despite Binance outwardly appearing to be proactively engaging with U.S. regulators, internally, Binance remained focused on retaining U.S. customers on Binance. The CFTC lawsuit accuses Binance of knowingly evading regulations, failing to comply with AML/KYC policies, and illegally offering trading products to U.S. customers. Allegedly, Binance instructed U.S. customers to use VPNs, maintained weak compliance controls, and encouraged VIP clients to circumvent these controls by opening up Binance accounts through shell companies.

The creation of Binance.US did little to decrease the amount U.S. customers using Binance. According to Binance’s own revenue reports, about a year after Binance notified U.S. users that they could not access the site, approximately 17.8% of Binance’s customers were still located in the U.S.

This lawsuit highlights that Binance created loopholes and promoted the evasion of its own compliance controls to maintain U.S. customers on their exchange, all in pursuit of profit.

This all occurred under CZ’s watch and direction. As the lawsuit aptly states,

FTX — anyone?

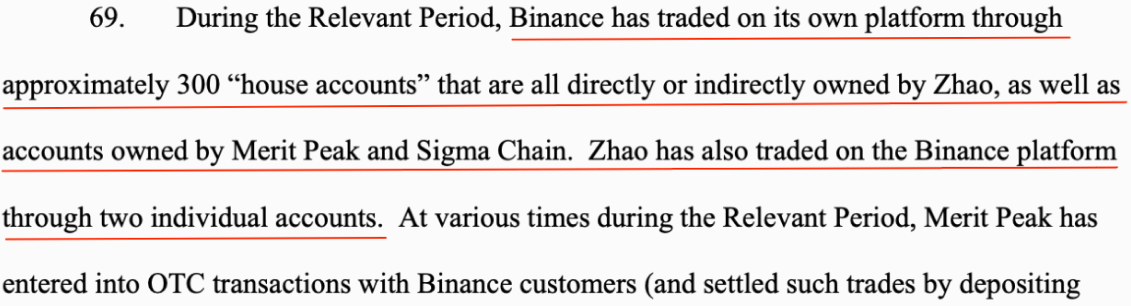

Maybe the most startling part of the CFTC lawsuit was the revelation that CZ owns 300 separate Binance accounts that have engaged in trading on the Binance platforms including the trading firms Merit Peak Limited and Sigma Chain AG, that act as market makers.

Binance failed to disclose in its Terms of Use that it engages in trading on its own platform with market makers managed by CZ, and the 300 “house accounts” are exempt from the insider trading policy that Binance recently implemented for employees.

Market makers play a crucial role in facilitating liquidity, ensuring price stability, and reducing bid-ask spreads. They profit from the difference between the price bid by buyers and asked by sellers.

For example, if the bid price for a stock is $50 and the ask price is $50.10, the bid-ask spread is $0.10. When a market maker buys the stock at $50 and immediately sells it at $50.10, they make a profit of $0.10 per share, minus any trading fees and other costs. This adds up and can be extremely profitable.

The SEC is currently investigating the relationship between Binance, CZ, and the two market-making firms mentioned previously. The key question is whether these market makers, owned by CZ and trading on the platform, received preferential treatment, giving them an unfair competitive advantage over other traders and boosting their profits.

This situation is again reminiscent of FTX. Sam Bankman-Fried infamously owned both the market-making firm Alameda Research and the exchange FTX. He was accused of sending billions of dollars in customer deposits to Alameda Research, which was given special privileges on the platform. A recent document from the FTX bankruptcy team revealed Alameda Research had the “unique ability to trade and withdraw virtually unlimited assets [on FTX], regardless of the size of its account balance and without risk of its positions being liquidated.”

When the same individual owns both the exchange and the market maker, it creates a major conflict of interest where they could potentially prioritize their own orders or manipulate prices to their advantage.

Reuters recently reported suspicious transactions that flowed from Binance.US to Merit Peak to the tune of $400 million over the first three months of 2021. Former Binance.US CEO Catherine Coley questioned this transaction, saying, “Where are those funds coming from?” but she did not receive a response. She later left the company and has not made any public statements since.

The nature of the source of these funds remains unknown, as does the reason for their transfer from Binance.US to the accounts of a market maker owned by CZ. However, the transaction suggests that Binance has some level of control over Binance.US’s finances despite publicly claiming the two entities are separate.

Throughout its history, Binance has faced many accusations of market manipulation, specifically in relation to wash trading. Wash trading involves executing trades with oneself to create the illusion of high trading volume and liquidity. In a recently published NBER paper titled “Crypto Wash Trading,” they categorized Binance as one of ten “Tier-1 Unregulated Exchanges,” and their findings concluded, “the average wash trading to be 53.4% of trading on unregulated Tier-1 exchanges.”

Given the obvious conflicts of interest involving CZ owning both market makers and the exchange, it’s not difficult to imagine that some form of market manipulation may occur, although no direct evidence has surfaced.

What further raised suspicions was Binance’s acquisition of crypto data provider CoinMarketCap for $400 million in 2020.

Many market participants found this concerning that the largest exchange now also owns the most popular data aggregator that shows the trading volumes. Some saw this as a conflict of interest where Binance could skew the data and manipulate the exchange volumes on the website.

One of those skeptical of the acquisition was a rival exchange operator Hong Fang, CEO of OKCoin, who issued a warning in a Twitter reply to an article on Binance’s CoinMarketCap acquisition.

This recent lawsuit from the CFTC revealed some of the questionable practices taking place behind closed doors at Binance, raising concerns about the conflicts of interest inherent in the exchange’s corporate structure. Binance is ultimately controlled by one man, who not only lacks a board of directors but also manages multiple market makers trading on the platform.

It’s important to note that the CFTC has not accused Binance of fraud. Nevertheless, the lawsuit exposes a corporate culture prioritizing profits over compliance with the law. This is perhaps why former U.S. regulator and Binance.US CEO Brian Brooks resigned his the position after only 3 months on the job. Should Binance be found guilty in court, the company could face a multi-billion dollar settlement. It would likely be required to permanently sever all ties with the U.S. financial markets.

To summarize Binance’s meteoric rise as the world’s largest cryptocurrency exchange, one could liken it to a mysterious rocket ship with dark-tinted windows that no one can see inside of, powered by cryptocurrency promoters and retail investors' tears.

Since its ICO, Binance has grown its user base by soliciting retail investors with digital penny stocks, continually driving value to the BNB token they hold, all while falsely marketing its products as decentralized and evading legal authorities at every turn.

It now appears that there is blood in the water, and the regulators are circling this large crypto casino and the individuals that run it. While Binance has not yet been formally charged with fraud or criminal wrongdoing, the numerous red flags and striking similarities to FTX’s downfall are challenging to ignore. Binance has experienced immense success over the past five years, with the casino business treating them well. However, it remains to be seen just how fragile this secretive operation truly is. If you have funds still on Binance, the warning signs are unmistakable.

Act accordingly.

Buy automatically every day, week, or month, starting with as little as $10.

Sam Callahan is the Lead Analyst at Swan Bitcoin. He graduated from Indiana University with degrees in Biology and Physics before turning his attention towards the markets. He writes the popular “Running the Numbers” section in the monthly Swan Private Insight Report. Sam’s analysis is frequently shared across social media, and he’s been a guest on popular podcasts such as The Investor’s Podcast and the Stephan Livera Podcast.

News

More NewsThoughts on Bitcoin from the Swan team and friends.

Swan Guard brings world-class Bitcoin security with advanced risk controls, scam defense, and expert support — vigilantly protecting your Swan account and safeguarding your Bitcoin.

After managing a Swiss gold fund for 8 years, I realized Bitcoin surpasses gold as the ultimate store of value. Here’s why every gold investor should study Bitcoin closely.

Ben Werkman joins Swan as CIO. New LBE primer explains key concepts, implementation steps, risk management, and valuation approaches.