Swan Private Market Update #37

This Market Update report was originally sent to Swan Private clients on August 11th, 2023. Swan Private guides corporations and high net worth individuals globally toward building generational wealth with Bitcoin.

This Market Update report was originally sent to Swan Private clients on August 11th, 2023. Swan Private guides corporations and high net worth individuals globally toward building generational wealth with Bitcoin.

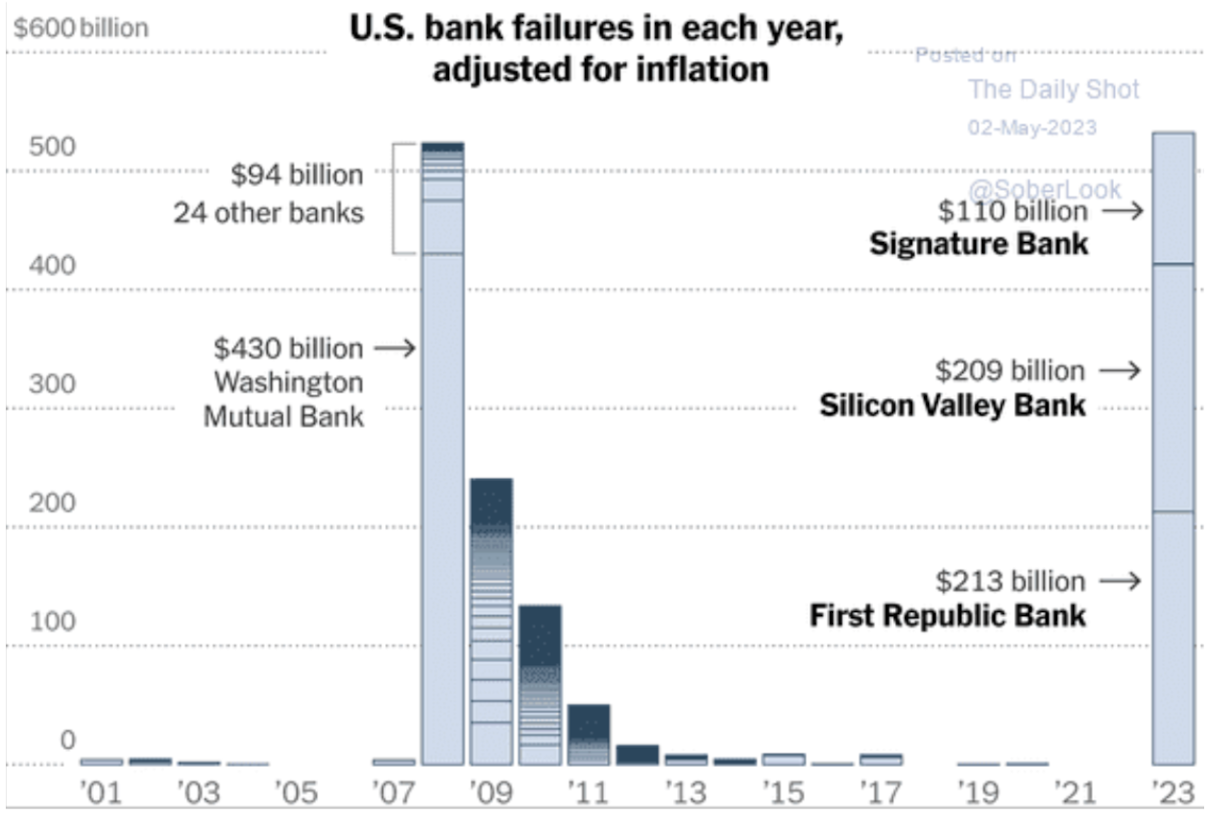

Another week, another major bank failure. This time First Republic Bank, the once 13th largest bank in the United States, was seized by the FDIC and sold to JP Morgan Chase via auction on Monday. This marked the 2nd largest bank failure in history, behind Washington Mutual Bank in 2008.

In 2023, three banks with a combined $532 billion in assets have now failed. It’s safe to say that we are currently in the middle of a full-blown banking crisis.

Regional banks continue to come under pressure as their assets have bled out as interest rates have soared. Many of these regional banks are sitting on Treasuries and mortgage-backed securities that have suffered greatly as the Fed has gone on its hiking tirade. At the same time, these same banks have been hit on the liability side as depositors have left in droves to the safety of larger banks or in search of higher yields in money market funds.

First Republic’s stock cratered when it released its Q1 earnings report revealing its precarious financial position. The report showed that over $100 billion in deposits were withdrawn from the bank in the first three months of 2023 alone. As a result, First Republic’s stock had crashed -88.5% year-to-date at the end of the first quarter.

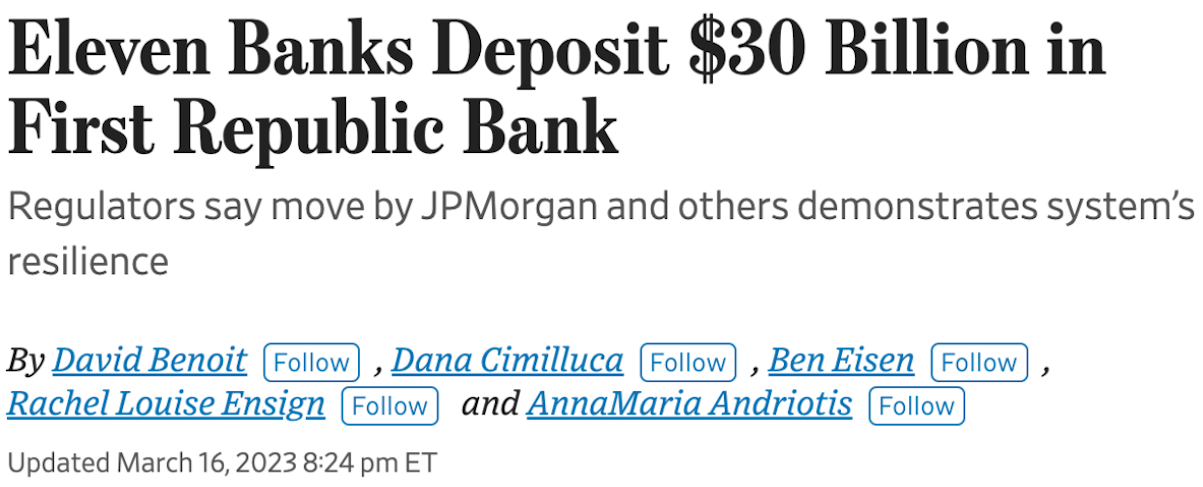

To stem the outflow of deposits, First Republic received a liquidity injection from eleven large banks in the form of $30 billion in deposits back in March.

On top of that, First Republic did not hesitate to access all the emergency lending facilities it could to keep its doors open.

As the bank came under serious duress, it borrowed:

$63.5 billion through the Federal Reserve’s discount window

$13.8 billion from the new Bank Term Funding Program

$28 billion from the Federal Home Loan Bank

Yet despite all of those liquidity measures, First Republic still died. Its shareholders have been wiped out. It goes to show that no amount of liquidity can fix a solvency problem and highlights how the Fed’s emergency programs may not be enough to prevent future bank collapses.

Entering the weekend, there was plenty of speculation on whether or not the FDIC would seize First Republic, but the FDIC was strangely silent. Some thought that after the second and third largest bank failures in history (Silicon Valley Bank and Signature Bank), the FDIC was hesitant to put another major bank into receivership. But in the end, they had no choice. Late Sunday, regulators shut down the lender and immediately sold most of its assets and $93 billion of its deposits to JPMorgan Chase.

This was the ideal outcome for the FDIC because by selling all the deposits to JPMorgan, the government did not have to deem First Republic a “systemic risk” and backstop all uninsured deposits like what occurred in the failures of Silicon Valley Bank and Signature Bank. This result was better optics because technically the depositors were not backstopped by the government.

Hold your IRA with the most trusted name in Bitcoin.

This was another example of regulators picking winners and losers, and in this case, they picked the same winners that they’ve picked over the last several decades — wealthy individuals and JPMorgan Chase.

JP Morgan and its CEO Jamie Dimon were hailed by some as heroes who helped save the FDIC insurance fund around $10 billion in losses after the deal.

Jamie Dimon himself lauded his bank’s response to First Republic’s collapse, “Our government invited us and others to step up, and we did.”

But, of course, Jamie Dimon didn’t buy First Republic Bank out of the goodness of his heart. JPMorgan made sure the deal was full of sweeteners before they shook hands on it.

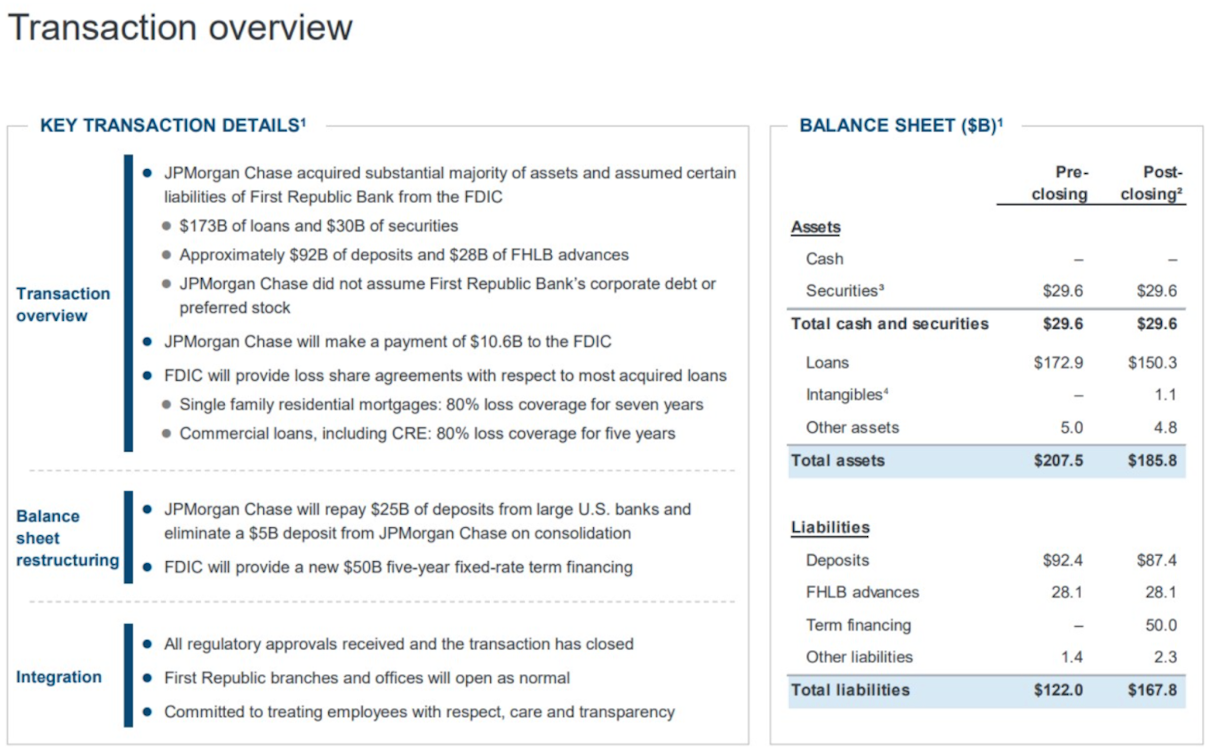

As part of the acquisition, the FDIC has agreed to a $50 billion five-year burden-sharing arrangement where it will cover the unrealized losses on First Republic’s loans. This includes 80% loss coverage on single-family residential mortgages for seven years and 80% loss coverage on commercial real estate loans for five years. Said differently, the FDIC will eat the vast majority of losses on all the bad loans on First Republic’s books, and JPMorgan will get billions in new deposits and assets with massive upside and downside protection.

Below is a snapshot of the details of the deal:

So JPMorgan gets gifted a bank with FDIC guarantees attached to it to protect themselves if the deal goes south. The cherry on top is that JPMorgan gets to look like the savior of the banking system once again, but in reality, the biggest bank just got bigger.

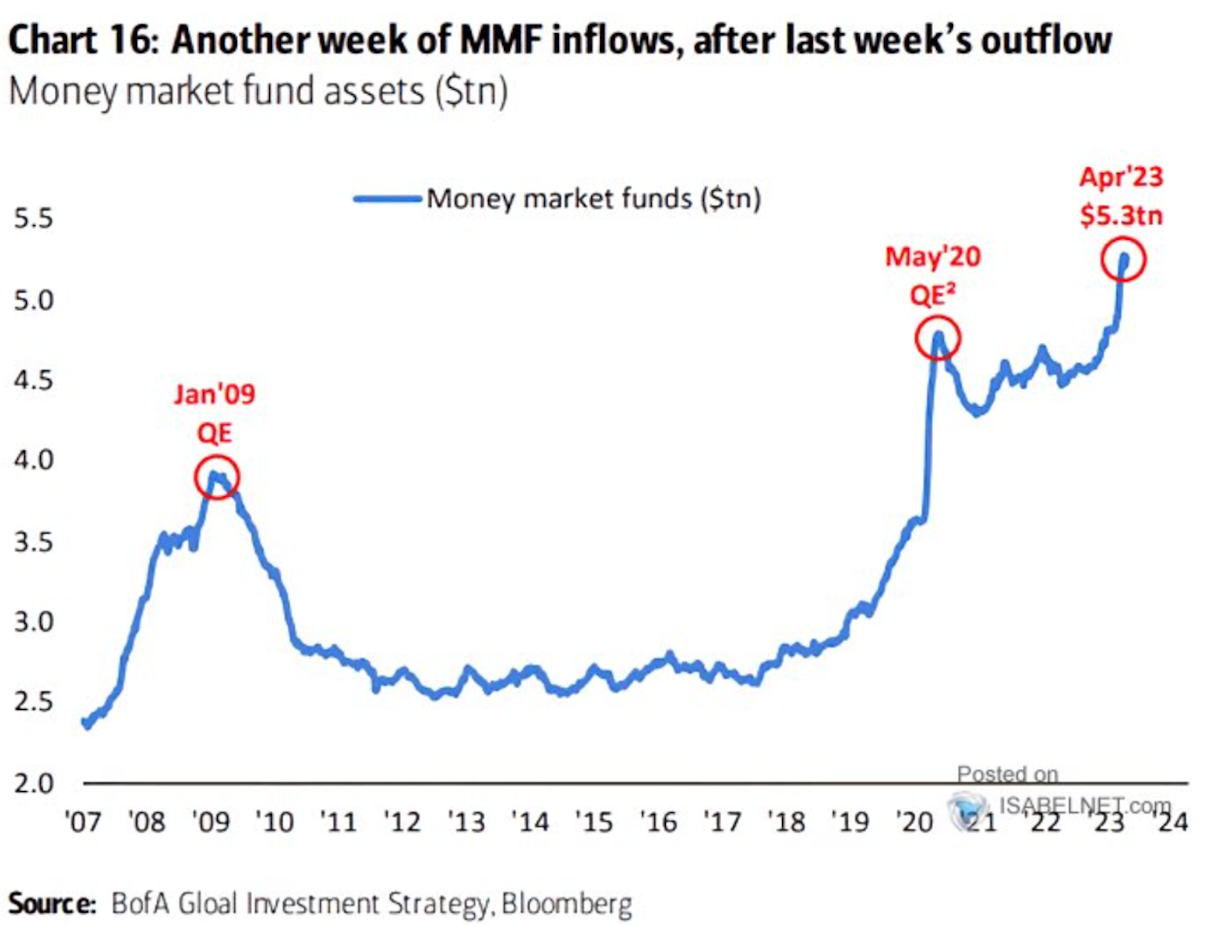

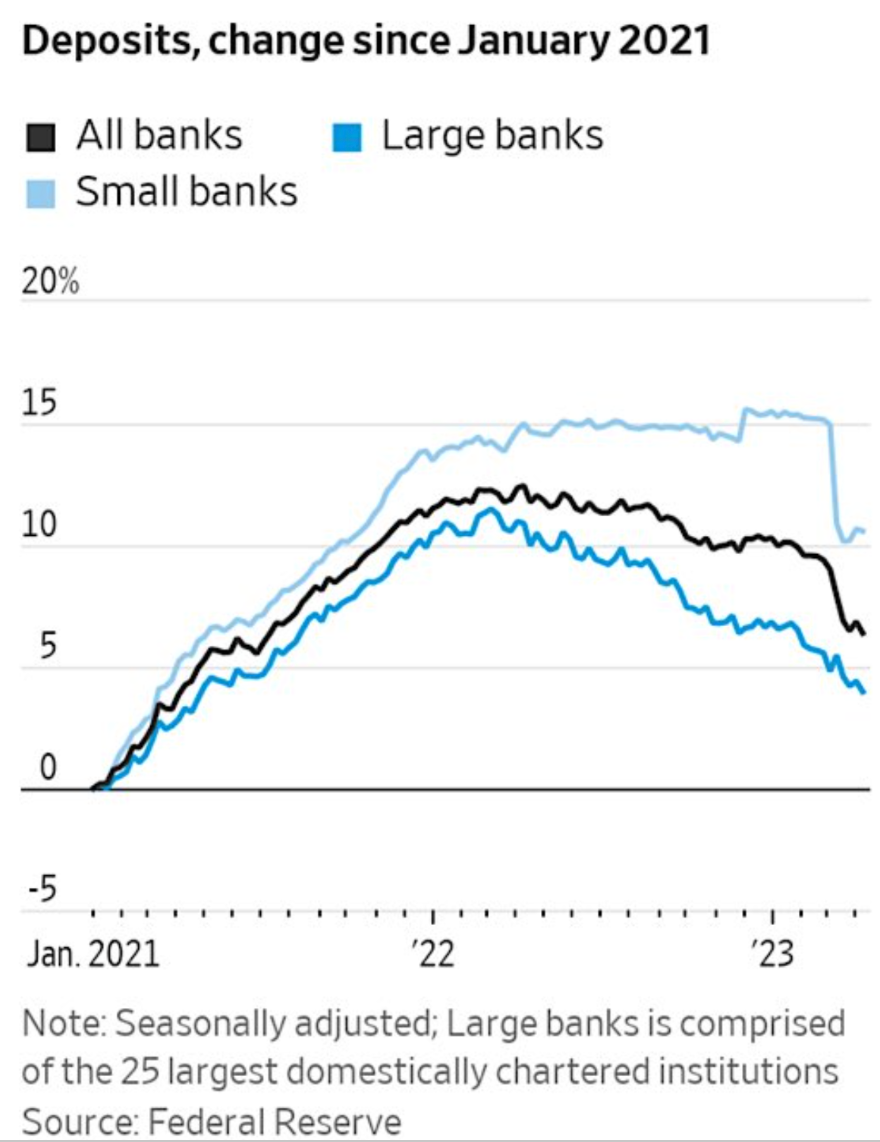

This highlights a trend that we have seen accelerate since the banking crisis began in March. Deposits have continued to flow out of small banks. Some of these deposits are in search of better yield in money market funds now that they can earn ~5% by parking their funds in a money market fund. Money market funds recently hit a record $5.3 trillion in April.

These deposits from small banks are also flowing into large banks as investors feared that small banks are more likely to fail than big banks, especially after Treasury Secretary Janet Yellen essentially confirmed this in a hearing one month ago.

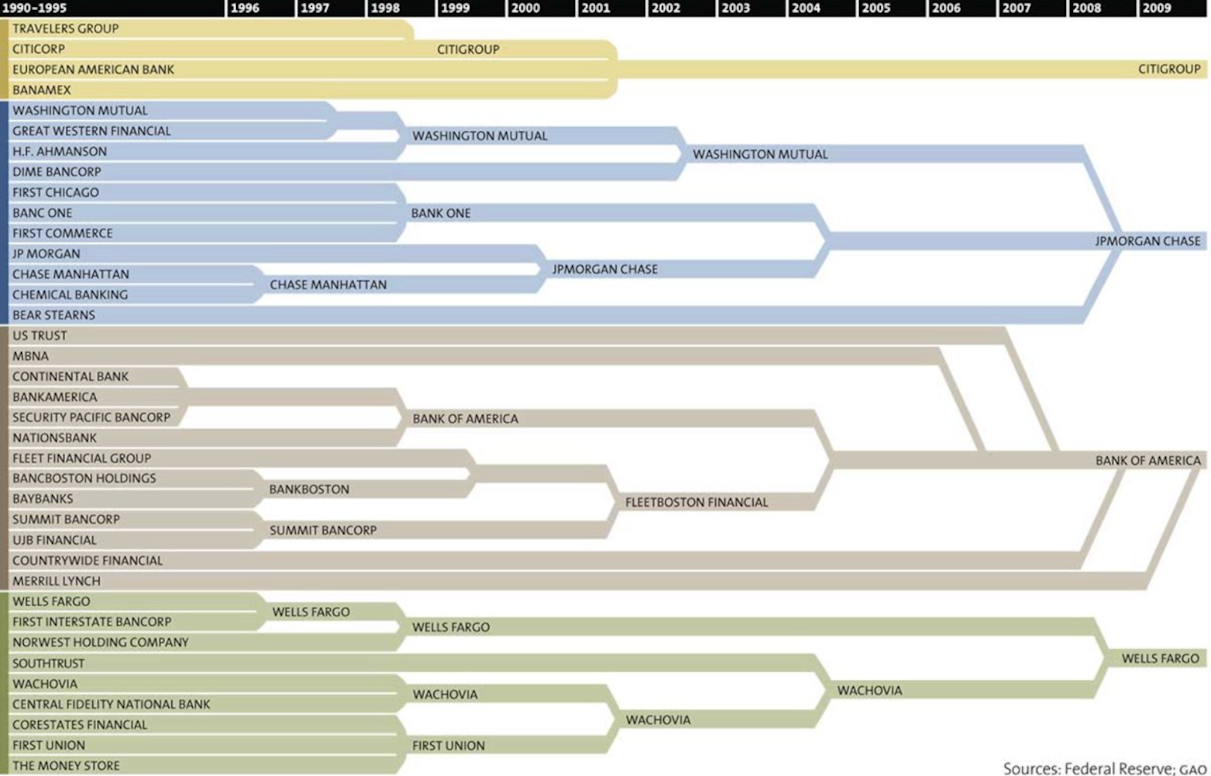

The traditional financial system continues to consolidate. The number of FDIC-insured financial institutions peaked in 1984 at 17,811 and has been in steady decline since, with 4,897 institutions functioning in 2021. JPMorgan has grown into one of the so-called “megabanks.”

Bank consolidation isn’t good for anyone but the big banks. It leads to the potential increase in risks to financial stability and few choices for consumers regarding financial services. This can lead to higher costs and fees for the consumer as competition falls by the wayside.

This recent deal only centralizes the traditional banking industry more as it continues to come under pressure. Not only do recent events shine a light on the fragility of the banking sector, but it also shows how the rules that govern the industry are disregarded in times of crisis.

In the aftermath of the Global Financial Crisis, the Dodd-Frank Act was passed that aimed to decrease bank consolidation and reduce the risk of “too-big-to-fail” institutions by preventing any one institution from holding more than 10% of US domestic deposits. With this recent acquisition, an exemption was made for this rule, and JPMorgan now controls >10% of American deposits. JPMorgan is larger than ever, and the banking sector has never been more centralized than today.

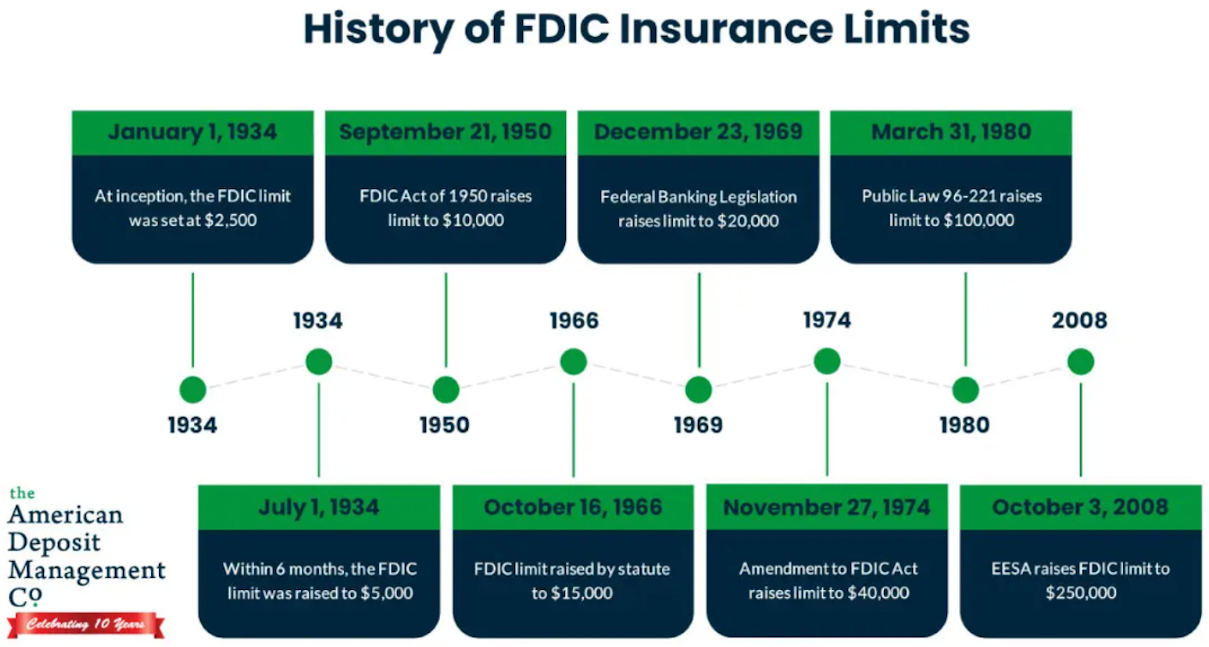

There have also been new calls to raise the $250,000 FDIC cap in the wake of these bank failures. This wouldn’t be the first time the FDIC cap was increased during a crisis. The last time the FDIC cap was raised was in 2008.

This goes to show that the rules in the traditional financial system are disregarded when times get tough. This is in stark contrast to Bitcoin, where the rules are embedded in the code, never to be changed.

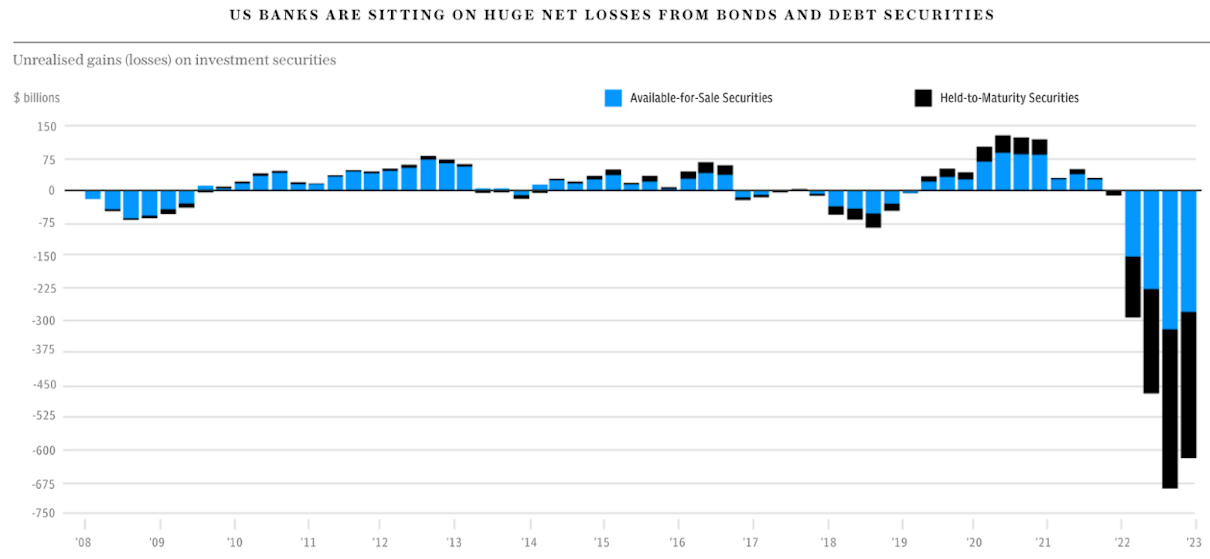

What’s clear is that this banking crisis is not yet over. Many banks are still sitting on massive unrealized losses on their debt securities due to the rapid rise in interest rates over the last year. According to a recent Hoover Institution study, 2,315 US banks are sitting on assets worth less than their liabilities, and the market value of their debt securities is ~$2 trillion lower than the stated book value.

Most of the damage continues to happen at regional banks, which both hold underwater assets in terms of their loan portfolios, but also continue to see deposits leave for the safety of larger banks.

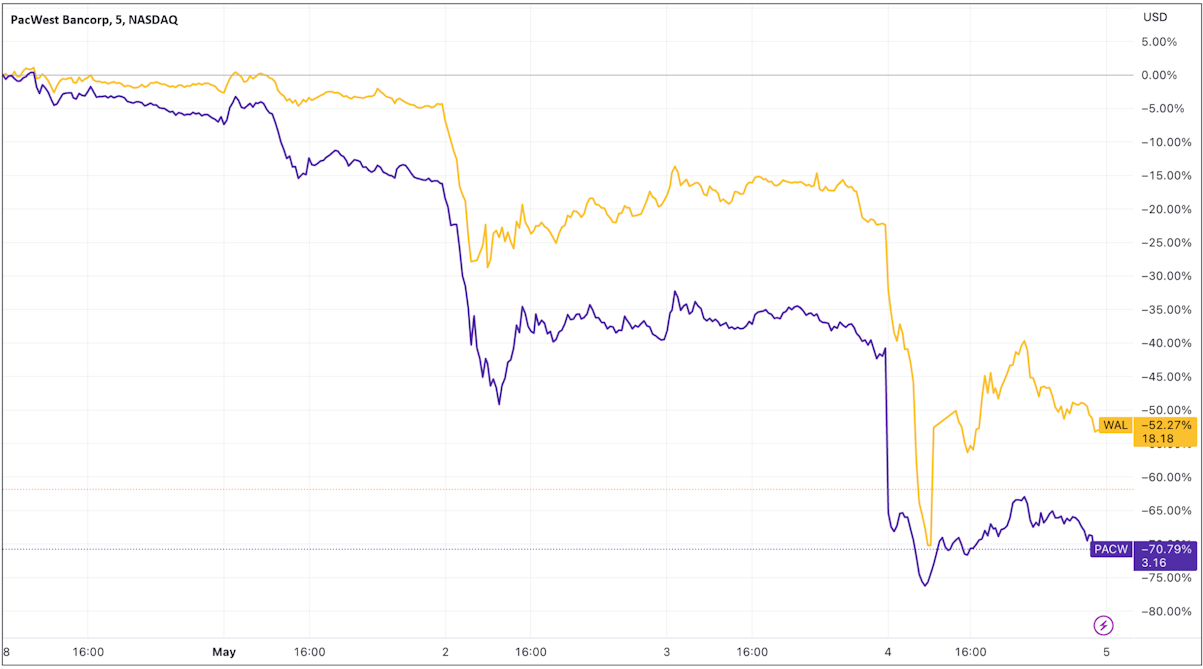

When you look at the year-to-date performance of the regional banking ETF versus the S&P 500 and JPMorgan Chase, the pain felt in these regional banks is clear to see.

It didn’t take long for the next victims of the bank crisis to emerge after First Republic’s downfall. Two more regional banks in PacWest and Western Alliance have both crashed this week. PacWest is down -71% and Western Alliance is down -52% over that time frame.

Both stocks were temporarily halted on Wednesday and short-selling was banned. This just goes to show that this banking crisis is not over.

It certainly doesn’t help that the Federal Reserve continues to hike rates despite the turmoil in the banking system. The Federal Reserve increased its benchmark rate another 0.25% on Wednesday to combat inflation. This will only worsen the value of these banks’ loan portfolios and raise the difference between the yield that depositors can earn when holding their savings at a bank versus putting them in money market funds.

It seems the Federal Reserve is on a war path against inflation and doesn’t care how many bank bodies it leaves in its wake.

In fact, it was recently discovered that the Fed Board was given a presentation back in February on the risk that rising rates have on banks due to the unrealized losses on their loan portfolios. The example bank used in the presentation to highlight the risk — Silicon Valley Bank. And yet, the Fed kept hiking rates despite the warning.

Meanwhile, all of this chaos has acted as one big marketing campaign for Bitcoin. A key motto of Bitcoin is “Be your own bank.” Michael Saylor describes Bitcoin as an incorruptible bank in cyberspace. With Bitcoin, no one needs to trust that a bank is solvent ever again. With each bank that fails, Bitcoin’s value proposition only grows stronger.

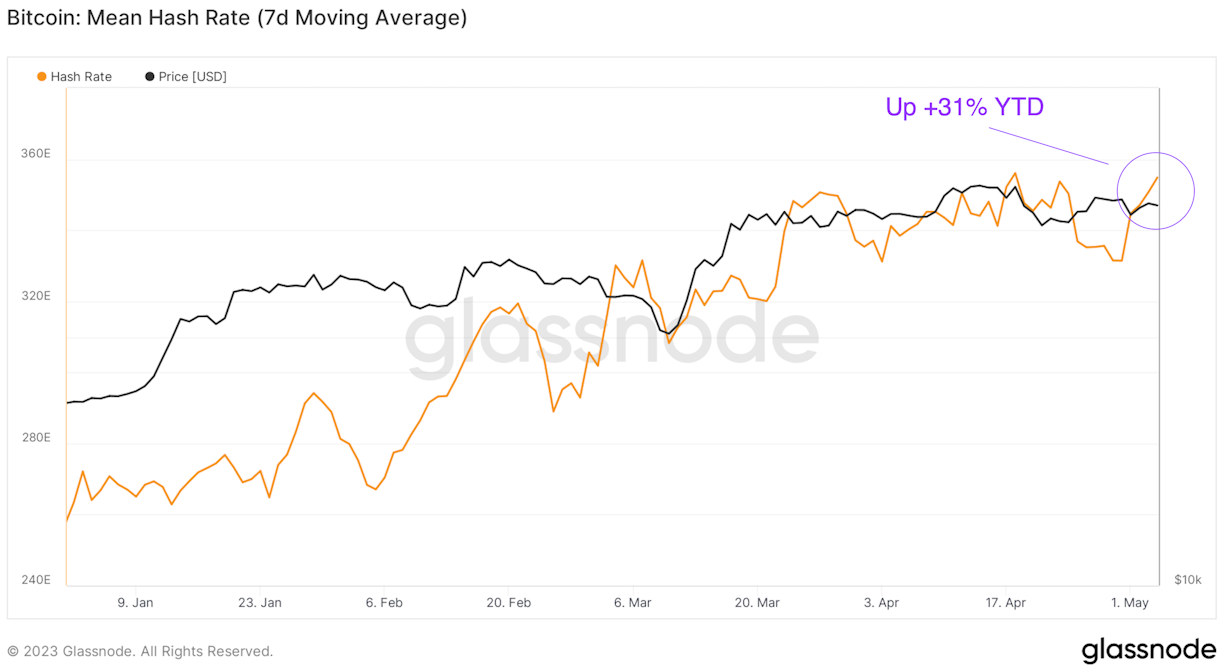

Bitcoin itself is growing stronger. Its hash rate continues to skyrocket in 2023. When speaking with two miners on the most recent episode of Swan Signal, they postulate that this increase is primarily due to the lag in delivery of mining equipment ordered by mining companies over a year ago. The equipment has finally come, and the ASICs are getting plugged in.

Bitcoin’s hash rate is now up over 30% year-to-date. Bitcoin’s security has “gone to the moon” this year.

Another theory is that nation-states are starting to get more involved in Bitcoin mining. One miner on Swan Signal spoke of the chatter in the industry around the uptick in ASIC orders coming out of Russia. Over the last couple of years, there have been plenty of rumors about Russia and Bitcoin adoption, especially after the country has been placed under severe sanctions since the Russian-Ukraine War began. These rumors have been shared by many, including fellow miner Marty Bent.

With abundant natural resources, Russia always seemed like a likely candidate to embrace Bitcoin mining, and now it appears that this idea is becoming a reality. Another smaller nation also was discovered to be mining Bitcoin for years. Bhutan, a small Himalayan nation, recently announced that it has been mining Bitcoin since it was at $5,000. Bhutan has excess hydroelectric power and has put that stranded energy to use by mining Bitcoin.

These developments speak to a couple of things. 1) Incentives drive Bitcoin mining and its adoption around the world, and 2) the Bitcoin mining industry will continue to be driven offshore if America doesn’t begin to recognize this innovative technology.

Luckily, Bitcoiners are doing their best to educate policymakers on the benefits that Bitcoin could bring to the United States. Last week, the Bitcoin Policy Institute held the first Bitcoin Policy Summit that included talks from two sitting US Senators and various industry entrepreneurs educating DC insiders on Bitcoin.

Watch the talks from the summit from Senator Cynthia Lummis, Senator Ted Cruz, and Strike CEO Jack Mallers.

After the event, 21 Bitcoiners took the Hill and spent the day meeting with politicians to discuss how Bitcoin could benefit the United States.

Overall, the response from these policymakers was positive. Many understood how Bitcoin was fundamentally different from other cryptocurrencies. There was one message that kept being brought up by these Congressional Staff Members, “We do not want to push innovation overseas. We know Bitcoin is here to stay. We want to come up with guardrails that don’t stifle innovation.”

My take while I was speaking with these politicians was that these Congressional Offices were more educated and more supportive of the Bitcoin industry than I expected. It was an encouraging visit as regulators continue to crack down on the broader cryptocurrency industry. More and more seem to understand that Bitcoin is a technology that could revolutionize payments and the energy industry.

Bitcoin has proven extremely resilient this year as it has rallied against a backdrop of a regulatory attack on the cryptocurrency industry, a banking crisis, and Federal Reserve continuing to tighten financial conditions. The price continues to consolidate between $28,000 — $30,000, and who has been stacking? Small retail investors have been buying the dip.

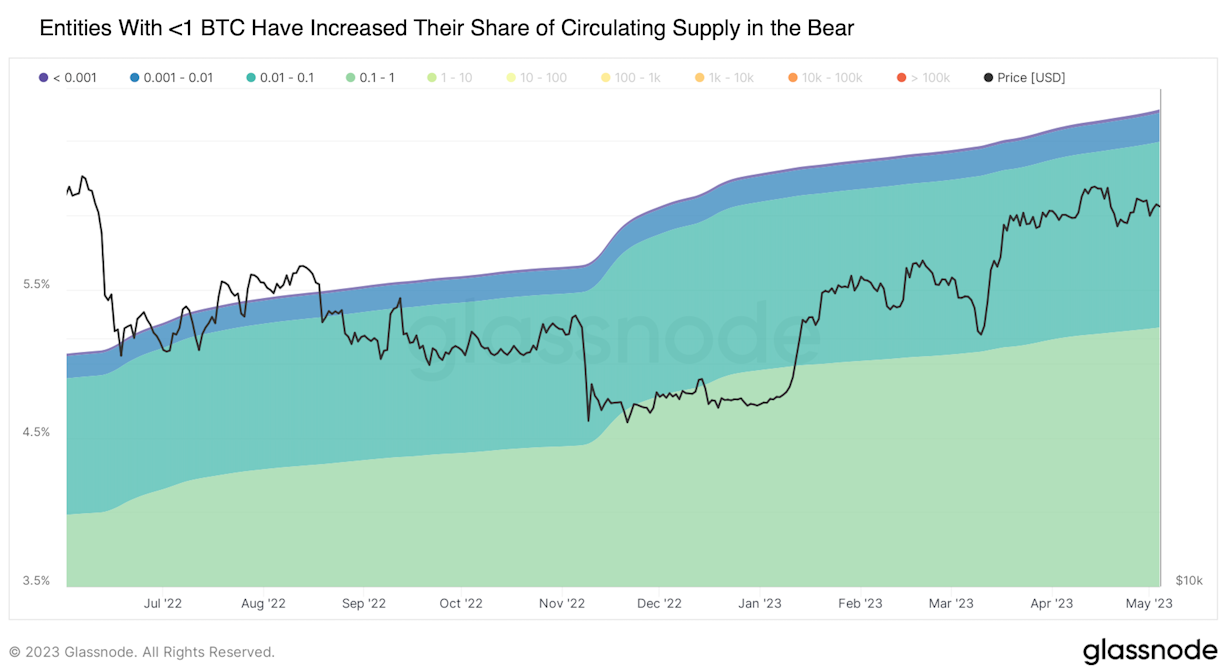

Entities holding less than 1 Bitcoin have increased from 5% of the total supply to 6.6%, a 32% increase since June 2022.

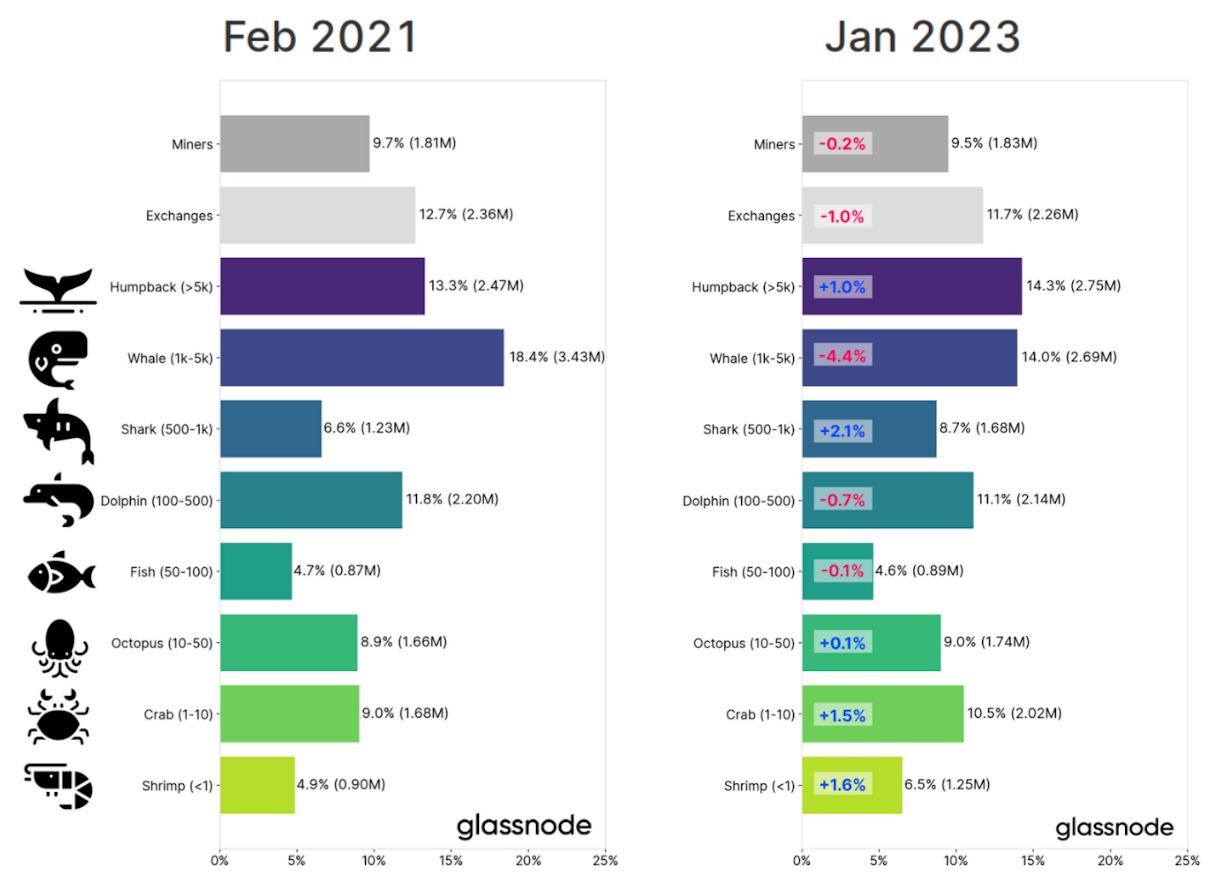

Smaller entities are increasingly holding a greater percentage of Bitcoin’s circulating supply. In fact, addresses holding less than one bitcoin are currently accumulating over 28,000 bitcoin per month, while new supply is only about 27,000. These smaller entities are absorbing the entire newly issued Bitcoin every month! And with the next halving arriving soon, we may just have a supply crunch on our hands in no time. Recent research from Glassnode highlights how the smallest entities are gaining a more significant share of Bitcoin’s supply, and larger entities have seen their share shrink since February 2021.

In other words, Bitcoin’s circulating supply is becoming more decentralized and resilient over time while the traditional banking industry continues to grow more centralized and fragile.

Many investors are looking at indicators that show that Bitcoin may be entering a new bull market as we approach the next halving in the spring of 2024. These investors are wondering if Bitcoin could drop again or if it will continue to rise toward $40,000. The key point to understand is that Bitcoin’s price increases happen violently. If you are on the sidelines when these explosive moves occur, you will drastically underperform.

If we look at the top-3 three-day upward price movements since 2018, we can see how important it is to be invested when these green days happen. For example, if an investor had invested $100 dollars into Bitcoin on May 4th, 2018, by today, that $100 would be $297. But if an investor had invested $100 dollars into Bitcoin that same day but missed the top-3 three-day price movements, their original investment would be worth $153!

In other words, if an investor had missed these top-3 three-day price movements during this period, their total return was 144% less than an investor who captured all of those gains.

The moral of the story, the most important factor for capturing Bitcoin’s future price appreciation is being invested for long periods instead of trying to time the market. When looking at the state of the baking industry, it is hard to not think, “This is why Bitcoin was invented.” In the short-term, Bitcoin’s price will continue to be volatile and fluctuate with the macroeconomic environment. Still, over the long-term, Bitcoin’s value proposition continues to be bolstered with every bank that shuts its doors due to its poor risk management and the Fed’s irresponsible and erratic policy decisions. Stack accordingly.

Market Overview

Tradingview, Prices as of 05/05/23

Hold your IRA with the most trusted name in Bitcoin.

Sam Callahan is the Lead Analyst at Swan Bitcoin. He graduated from Indiana University with degrees in Biology and Physics before turning his attention towards the markets. He writes the popular “Running the Numbers” section in the monthly Swan Private Insight Report. Sam’s analysis is frequently shared across social media, and he’s been a guest on popular podcasts such as The Investor’s Podcast and the Stephan Livera Podcast.

News

More NewsThoughts on Bitcoin from the Swan team and friends.

The credit-based traditional financial system is built on trust, and right now, that trust is breaking down in a world where trustless digital money exists.

Market participants are scratching their heads and wondering, “Is this rally for real?” Let’s look at the data to discern some of the bullish and bearish arguments for where markets will move forward from here.

There are lots of words to describe the last week when it comes to the traditional financial system, but orderly is certainly not one of them.