Swan Private Market Update

This market update was originally sent to Swan Private clients. Swan Private guides corporations and high net worth individuals globally toward building generational wealth with Bitcoin.

This market update was originally sent to Swan Private clients. Swan Private guides corporations and high net worth individuals globally toward building generational wealth with Bitcoin.

There’s no need to mince words when describing the markets over the last two weeks, it’s been ugly. Things started to fall apart last week when CPI inflation surprised many market participants to the upside when it came in at 8.6% YoY, the highest reading in 40 years. This led to a sell-off in equities and bonds as investors connected the dots and realized that this inflation reading would mean more aggressive interest rate hikes from the Federal Reserve, and they were not wrong.

On Wednesday, the Federal Reserve raised the federal funds rate 0.75% to 1.50-1.75%, the largest single increase since 1994. Federal Reserve Chairman Jerome Powell also hinted at an additional 0.50%-0.75% rate hike at the next July FOMC meeting. Federal Reserve officials expect the benchmark rate to be at least 3% by year’s end and are currently expecting interest rates to not be cut until 2024. These same officials also revised their 2022 growth estimates downwards.

When asked about the worry of these aggressive rate hikes causing a recession:

We’re not trying to induce a recession now. Let’s be clear about that. We’re trying to achieve 2% inflation with a strong labor market — that’s what we’re trying to do.

Federal Reserve Chair

It seems highly optimistic for Fed officials to expect a “softish landing” when they choose to combat inflation by raising rates at the most aggressive pace in recent memory in an economy that’s up to its eyeballs in debt. One has to wonder how effective raising rates will be in beating back inflation. Does a 75 bps hike fix broken supply chains and years of underinvestment in the energy sector?

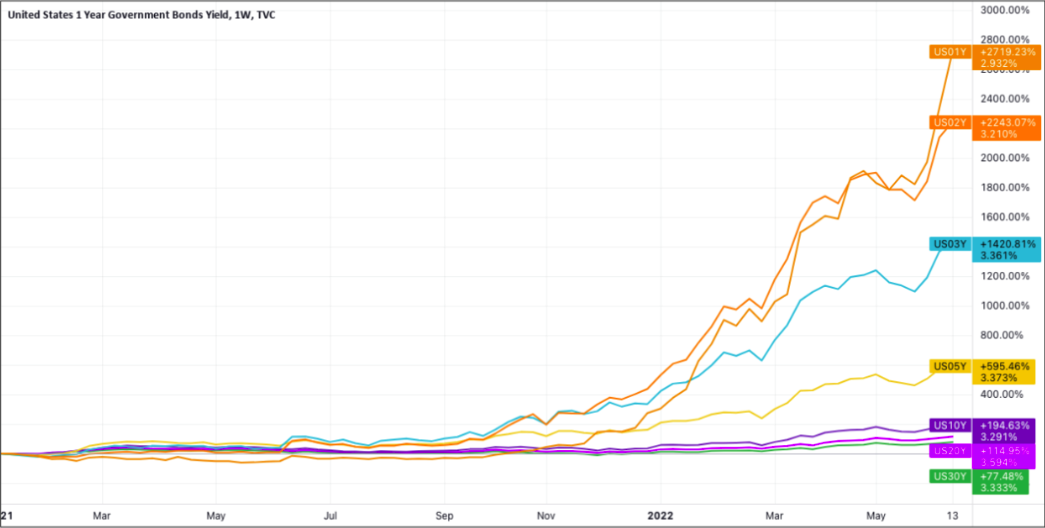

The stock market has continued to sell off sharply amid this environment of tightening financial conditions and high inflation. Over the last two weeks, the S&P 500 is down -11.32%, and the Nasdaq is down -12.86%. Furthermore, Treasury bond yields continue to rocket higher. Since the start of the year, interest rates across the entire yield curve have exploded upwards. On Monday, the 2-year Treasury yield had its largest single-day increase since 2008.

Tradingview

The 10-year Treasury yield spiked earlier this week to 3.39%, its highest since March 2020. The 2-year and 10-year Treasury curve also inverted for the first time since early April, a historically accurate indicator of a recession on the horizon.

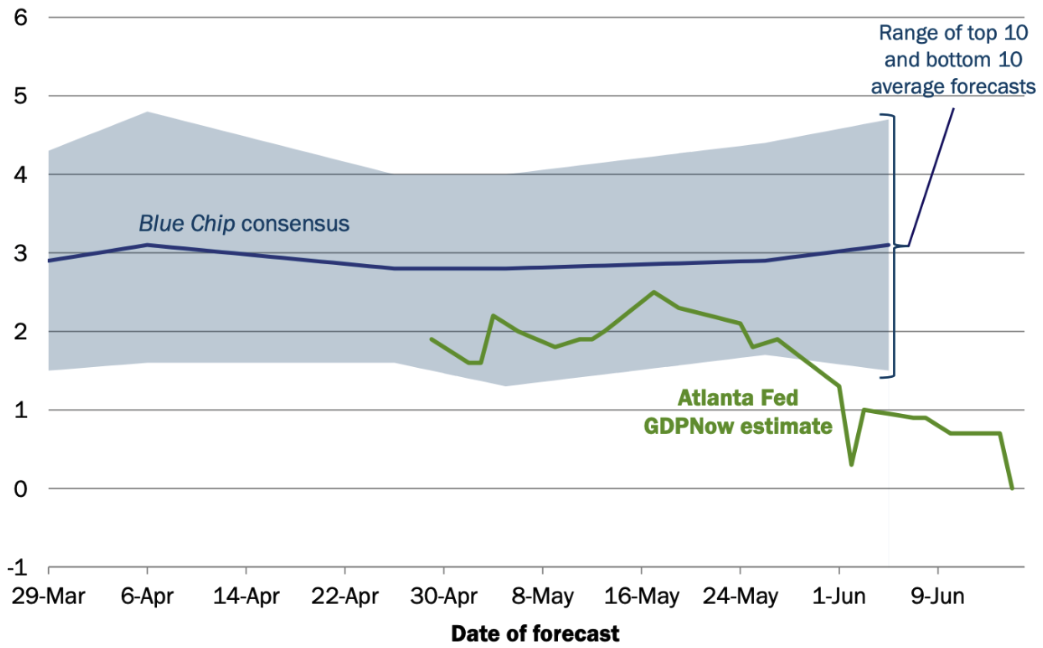

Yield curve inversion aside, signs of recession seem to be emerging everywhere. Yesterday, the Atlanta Fed revised its Q2 GDPNow real GDP estimate downwards to 0.0% from 0.9%, evidence that the U.S. is on the brink of an official recession (two consecutive quarters of negative GDP growth).

Blue Chip Economic Indicators and Blue Chip Financial Forecasts

The slowdown in economic growth in 2022 is finally starting to show up in consumer spending data as well. For the first time this year, nominal retail sales declined, coming in at -0.3% for the month of May. Consumers’ struggle with inflation is beginning to show up in the data.

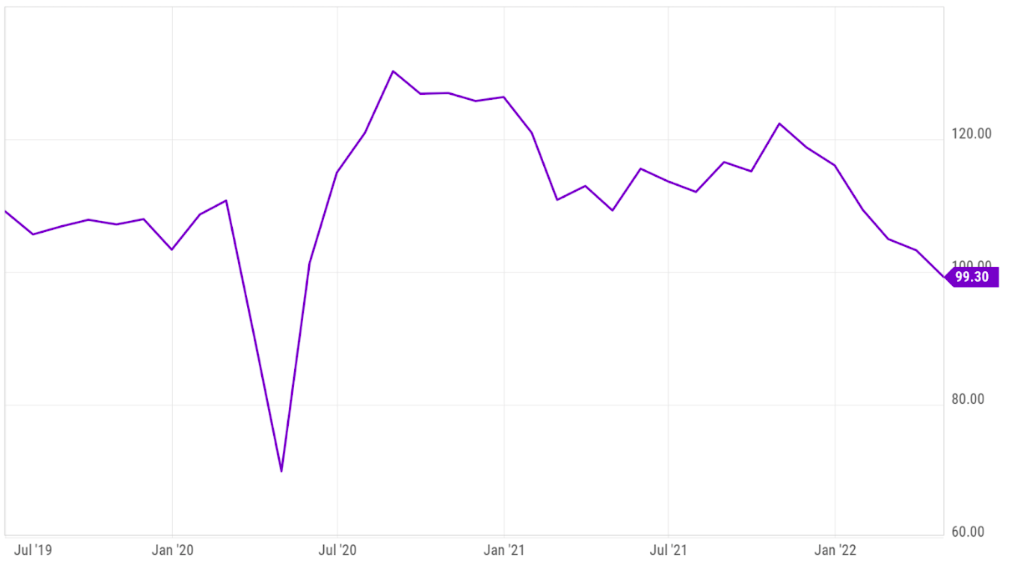

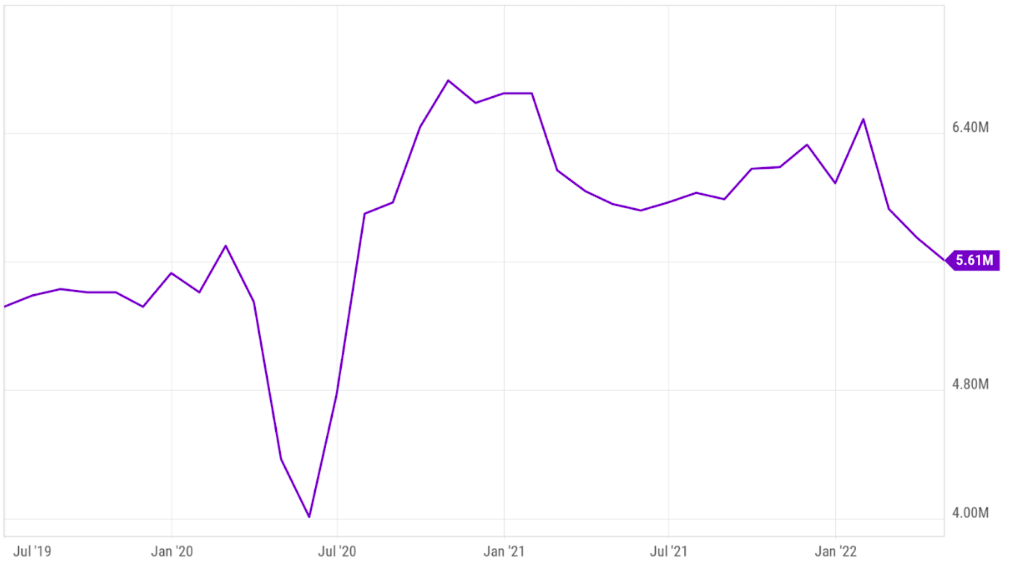

Signs of reduced consumer appetite are also starting to hit the real estate sector. Existing and pending home sales have dropped for 3 consecutive months since January.

Y Charts

Y Charts

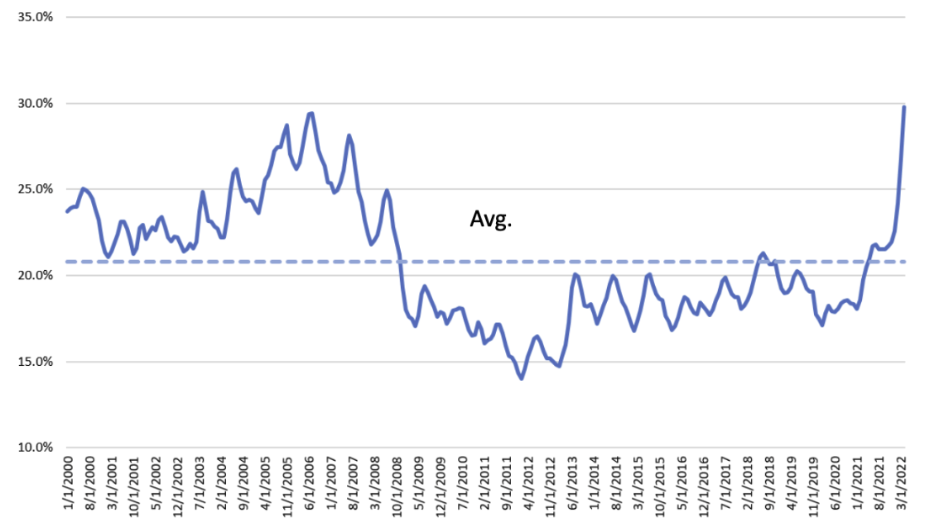

This could be a reaction to rapidly rising mortgage rates and the U.S. housing market being at its most expensive level ever. According to the Case-Shiller National Home Price Index, average home prices are at an all-time high and are currently up 20.54% YoY. The average 30-year mortgage rate recently spiked above 6%, the highest level since the Global Financial Crisis in 2008.

Both the sky-high prices and the high mortgage rates make this housing market unaffordable for many. Average mortgage payments as a percentage of median household income now sits at the highest reading in the last 22 years.

Bloomberg DoubleLine

Due to the decreased affordability of housing, we have seen mortgage applications and refinancing fall off a cliff as interest rates have risen. According to the Mortgage Banker’s Association, total mortgage application volume is down 52.7% compared to this time last year, the most significant contraction since 2006. Mortgage refinances have also fallen to its lowest level in two decades. This decreased demand for housing could result in falling home valuations, which would have a negative impact on the broader economy and add to the recessionary pressures.

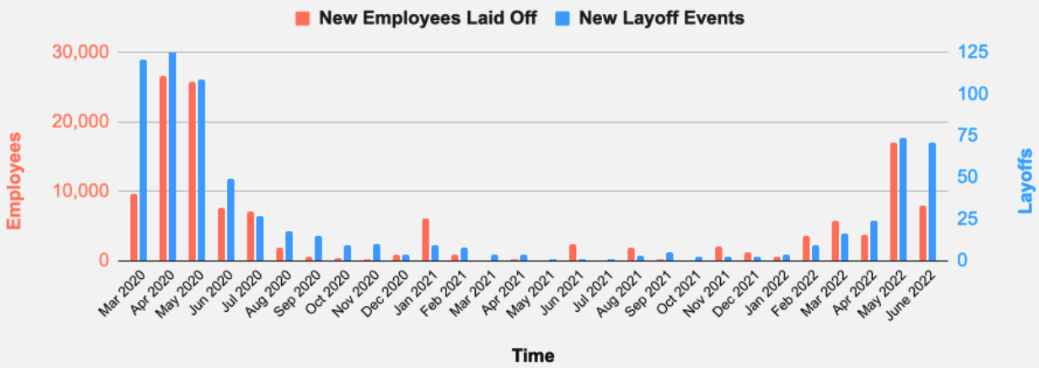

The other area of the market that is flashing recession signs is the labor market. Weekly initial jobless claims for unemployment benefits have been rising, up 37.95% since it bottomed in mid-March. It is now at its highest level in the last five months.

Over the last couple of months, we have also had several announcements of hiring freezes from the likes of Amazon, Walmart, Meta, and others. On top of that, company announcements of layoffs have increased significantly for the first time since the pandemic began, primarily in the tech and startup sectors shown below.

layoffs.fyi

With cracks in the labor market and the real estate market starting to emerge, one can see why growth estimates are being revised downward by many financial institutions.

The Fed is set on reducing inflation and proved it with this recent 0.75% rate hike. Chairman Powell said, “The worst mistake we could make would be to fail to bring down inflation…It’s not an option. We have to restore price stability.” Cracks in the economy are already starting to appear, and bond and equity investors alike are feeling the pain of this stagflationary environment. We will see just how much pain the Fed can stomach as they continue on their mission to rein in this damaging inflation.

Bitcoin has had a bloody week along with nearly all assets considered risk-on in this tumultuous macroeconomic environment. Bitcoin is down -31.64% over the last week and currently sits at $20,440. The price is consolidating right above its previous cycle all-time high of $20,000. Bitcoin’s recent downward price action can be in part blamed on happenings in the broader cryptocurrency market.

A couple of market updates ago, we wrote about the Luna/UST crash that wiped out around $50 billion dollars in value in a matter of days. A month has passed, but we are only now discovering which entities were badly exposed to that debacle. Some market participants were beginning to think that Luna/UST was an isolated event, but it turns out the knock-on effects were merely delayed.

Buy automatically every day, week, or month, starting with as little as $10.

Celsius, a large crypto lending platform, has long been criticized for how it uses its customers’ funds to make high-risk bets on DeFi yield-generating tokens. In the past, Celsius had lost funds on multiple DeFi hacks including Stakehound (~$120 million), BadgerDAO (~$50 million), and narrowly escaped becoming a victim of the Luna/UST crash themselves when they had an estimated $500 million in the Anchor protocol before withdrawing the funds just in time.

Celsius was essentially a risky hedge fund masquerading as a lending platform that provided liquidity (its own clients’ funds) for many DeFi protocols. Swan CEO Cory Klippsten had been warning about the risks of Celsius for the last month and once again was proven correct. This past week Celsius halted all trading and withdrawals on its platform due to apparent liquidity issues causing panic in the market.

Celsius

Celsius has now hired restructuring lawyers, and rumors continue to swirl around their possible insolvency. As of May 17th, Celsius managed $11.8 billion dollars in assets so this was no small fish. Celsius’s native token is now down -76.48% over the last two months alone.

Tradingview

These big intermediaries, like Celsius, have relationships with other entities, so when one defaults, it leads to another one being at risk of default, and another, and so on. The contagion from Luna/UST and Celsius continued to spread with the recent news that prominent crypto hedge fund Three Arrows Capital now faces possible insolvency after incurring at least $400 million in liquidations. This has led to margin calls and forced selling, putting pressure on Bitcoin, Ether, and all the other cryptocurrencies the hedge fund owned. The crypto hedge fund was estimated to be managing around $18 billion as of March 2022.

These cascading liquidations and insolvencies are par for the course in bear markets, but an unfortunate side-effect is they add increased selling pressure on Bitcoin as these risk-takers are forced to sell their positions to cover their losses.

In many ways, crypto is the canary in the coal mine for traditional markets. Crypto firms like Celsius and Three Arrows Capital were playing around in the riskiest parts of the market with obscene amounts of leverage. When the Fed started to tighten financial conditions and liquidity dried up, the first ones to blow up were these overleveraged crypto entities and blatant Ponzi schemes. We will see if this contagion continues to spread and whether it stays contained within the crypto industry or if it spills over to traditional markets.

On a more positive note, earlier in the week, Senators Cynthia Lummis and Kirstin Gillibrand introduced the first major piece of cryptocurrency legislation, the “Responsible Financial Innovation Act.” This bipartisan bill aims to provide some regulatory clarity to the broader cryptocurrency industry. Like all first drafts, there were many positive and negative takeaways from it.

Two strong components of the bill are the de minimus tax exemption it provides for Bitcoin transactions less than two hundred dollars and the removal of miners from the “broker” definition. The bill grants the CFTC with exclusive spot market jurisdiction over Bitcoin. It also has wording that protects consumers by requiring virtual asset service providers to make clear disclosures to customers and requires higher standards of disclosure of these providers to reduce market manipulation and fraud. It also requires stablecoins to be fully backed 1:1 with dollars or dollar-like equivalents and/or be FDIC insured to operate in the U.S. This will help clean up some of the Ponzi schemes and manipulation we have seen in recent months (Luna/UST). Lastly, the bill also codifies a person’s right to keep and control a digital asset they own, an important inclusion for private key ownership.

One of the biggest drawbacks of the bill is that it clearly states ETH is fully decentralized and is, therefore, a commodity which we thoroughly disagree with at Swan. It also fails to define how a digital asset is determined to be “fully decentralized” or not. The bill also directs the Federal Energy Regulatory Commission to conduct a study looking into “energy consumption” in the digital asset space. This alludes to Bitcoin’s energy usage being a problem when in fact, Bitcoin’s energy usage enables sound digital money and can help drive innovation in the energy industry.

It’s important to note that this bill is highly unlikely to go anywhere in Congress, but it is an important first step in providing a regulatory framework for this burgeoning new asset. It is more likely that this bill will be improved upon and that parts of it may be used in future pieces of legislation that are more likely to be voted on into law.

All in all, we have seen all the tell-tale signs of a Bitcoin bear market this past month. We have had large Ponzi schemes like Luna/UST blow up, entities like Celsius and Three Arrows Capital are teetering on the brink of insolvency, large crypto firms like Coinbase and BlockFi have announced major layoffs, and the price of Bitcoin has, of course, been in a steady decline.

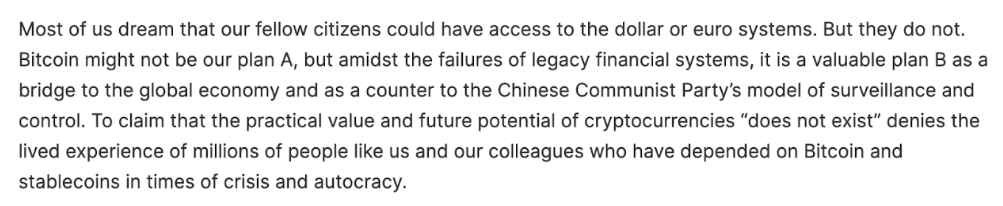

However, it’s times like these where one must focus on Bitcoin’s long-term value proposition. Bitcoin still remains an undebaseable and uncensorable money that can’t be controlled by any single person or group of persons. Bitcoin’s use case was on full display last week when a group of 20 human rights activists from 20 different countries penned a letter to Congress urging for responsible Bitcoin regulation.

A powerful excerpt from their letter is shared below:

This is why Bitcoin matters. When the price is down like this, one needs to ask the question of whether Bitcoin’s value proposition has changed or not. Despite the downward price action, Bitcoin remains a functional lifeline — today — to many individuals in countries across the globe who do not have the privilege of a stable financial system or government.

Bear markets are historically the best time for long-term investors to accumulate Bitcoin. The Mayer Multiple takes the current price of Bitcoin and divides it by its 200-day moving average. Historically, this metric has been useful in signaling when Bitcoin is overbought or oversold. Whenever the Mayer Multiple is <0.60, it has marked major Bitcoin market bottoms in the past. Today, it currently sits at 0.55, levels not seen since the 2018 bear market bottom.

charts.woobull.com

Although the price of Bitcoin will continue to fluctuate in this volatile and uncertain macroeconomic environment, when the Mayer Multiple is lower today than it has been in 97.8% of its history, and human activists are providing concrete evidence of Bitcoin being used to help empower marginalized groups of people, it’s hard to not like Bitcoin at these discounted price levels. Regardless, Bitcoin will continue to function perfectly as Satoshi intended regardless of what the Fed does, what the stock market does, what the real estate market does, or what the bond market does…and that’s kind of the whole point.

Tradingview

Buy automatically every day, week, or month, starting with as little as $10.

Sam Callahan is the Lead Analyst at Swan Bitcoin. He graduated from Indiana University with degrees in Biology and Physics before turning his attention towards the markets. He writes the popular “Running the Numbers” section in the monthly Swan Private Insight Report. Sam’s analysis is frequently shared across social media, and he’s been a guest on popular podcasts such as The Investor’s Podcast and the Stephan Livera Podcast.

News

More NewsThoughts on Bitcoin from the Swan team and friends.

Swan Guard brings world-class Bitcoin security with advanced risk controls, scam defense, and expert support — vigilantly protecting your Swan account and safeguarding your Bitcoin.

After managing a Swiss gold fund for 8 years, I realized Bitcoin surpasses gold as the ultimate store of value. Here’s why every gold investor should study Bitcoin closely.

Ben Werkman joins Swan as CIO. New LBE primer explains key concepts, implementation steps, risk management, and valuation approaches.

Audio narration