Swan Bitcoin Market Update #48

This Insight Report was originally sent to Swan Private clients on January 15th, 2023. Swan Private guides corporations and high net worth individuals globally toward building generational wealth with Bitcoin.

This Insight Report was originally sent to Swan Private clients on January 15th, 2023. Swan Private guides corporations and high net worth individuals globally toward building generational wealth with Bitcoin.

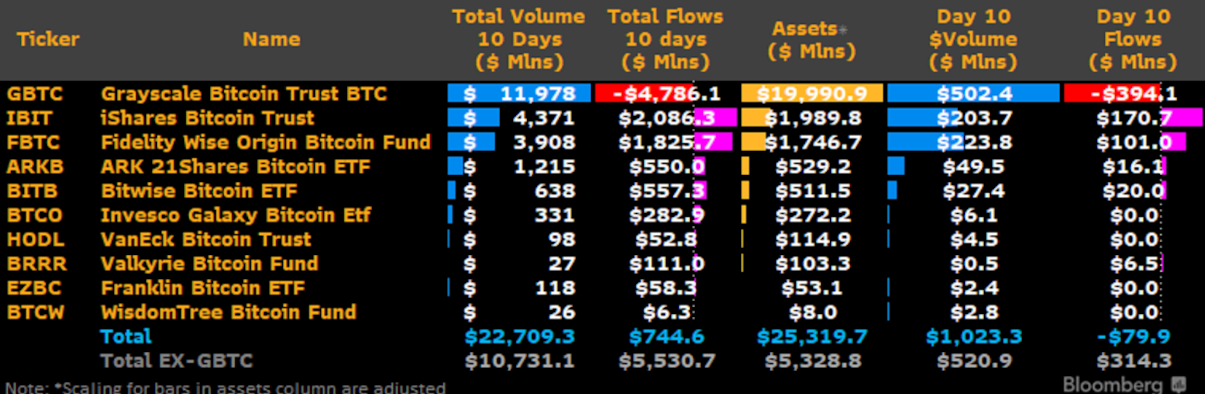

With 10 days of trading in the books, we now have a clearer picture of how much capital these new ETFs are attracting and which ETF providers are separating themselves from the pack.

According to Bloomberg Intelligence Analyst James Seyffart, to date, these new ETFs (excluding Grayscale) have brought in $5.5 billion in inflows.

At the same time, Grayscale’s GBTC has seen about $4.8 billion in outflows. This means that the net inflows into these spot Bitcoin ETFs have been $744 million.

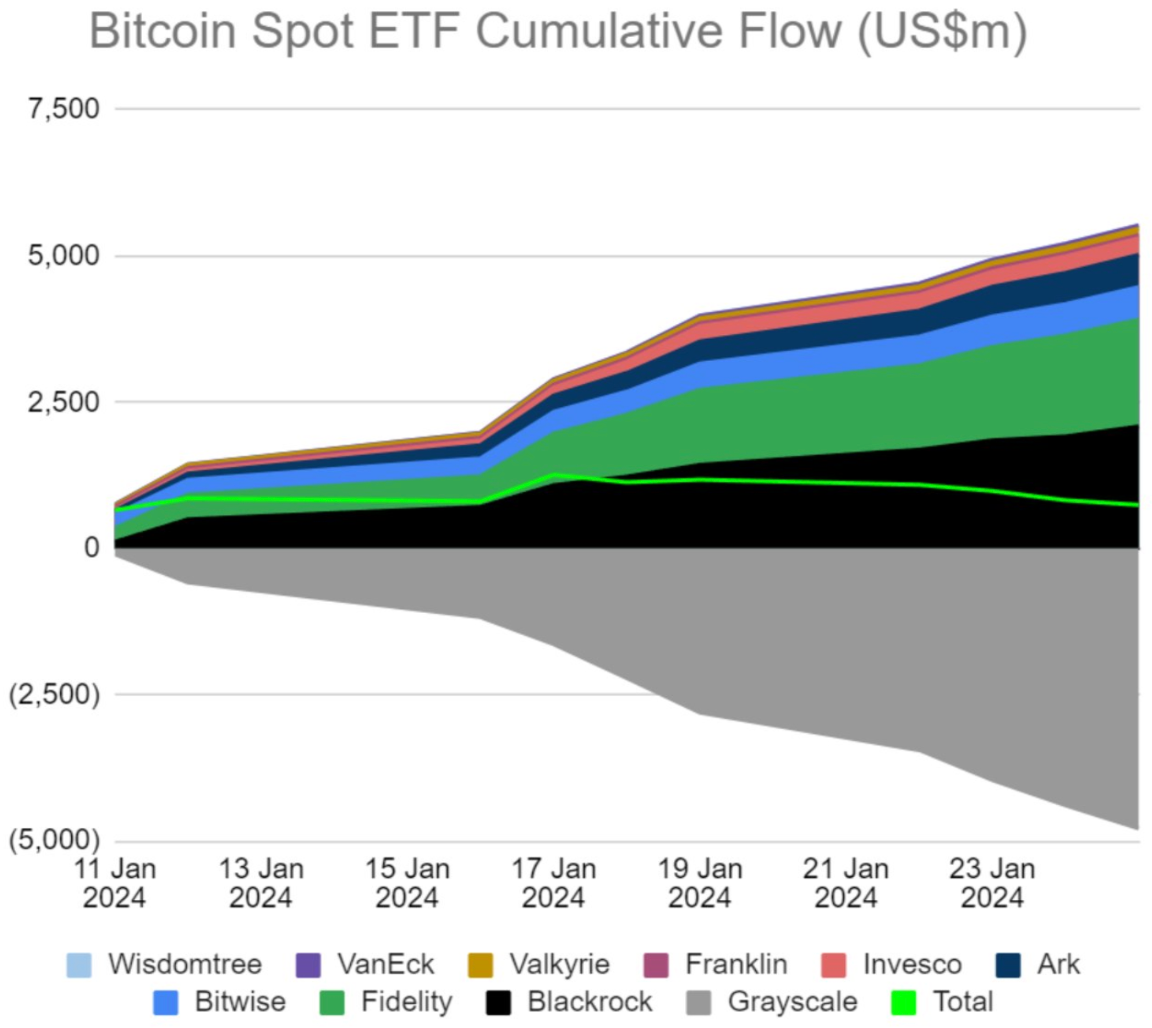

This dynamic is illustrated well in the chart below.

It appears that investors are continuing to dump GBTC, in part, because there are now cheaper alternatives with lower fees to gain exposure to Bitcoin. However, these aren’t the only people selling GBTC.

The FTX Bankruptcy Estate has reportedly sold 22 million shares of GBTC worth around $1 billion since GBTC was converted into an ETF. This makes up roughly one-fifth of the outflows over the last 10 days.

The FTX Bankruptcy Estate will now use the proceeds from the sale to distribute the funds to FTX customers who are waiting to recoup their money after the exchange’s collapse. The estate now holds zero GBTC shares and, thus, this selling pressure is behind us. FTX is likely not the only bankruptcy estate that holds GBTC that will be forced sellers in the future. But it’s important to note that these represent one-time selling events.

There are a few other explanations for why GBTC is seeing significant outflows. For starters, for many years it was the only way for investors to gain exposure to Bitcoin in retirement accounts. Now these investors can transfer their funds to a cheaper ETF with no tax consequences. This dynamic will likely result in continued outflows of GBTC in the coming months

Second, many traders were playing the discount arbitrage trade. GBTC was trading at a large discount and these traders were betting that it would be converted to an ETF, eliminating the discount. These traders were right, and now they appear to be taking some profit. It’s important to note that these traders were not long-term believers in Bitcoin’s value proposition or the impact of ETFs on demand for Bitcoin long-term. They were simply trying to capitalize on a market inefficiency and executed a trade.

As capital has flowed out of GBTC, it has flowed into the other ETFs. The top five ETF issuers have now purchased more than 100,000 bitcoins within just two weeks of being active. This shows how much potential sustained demand these ETFs are capable of bringing to the asset class in the years to come.

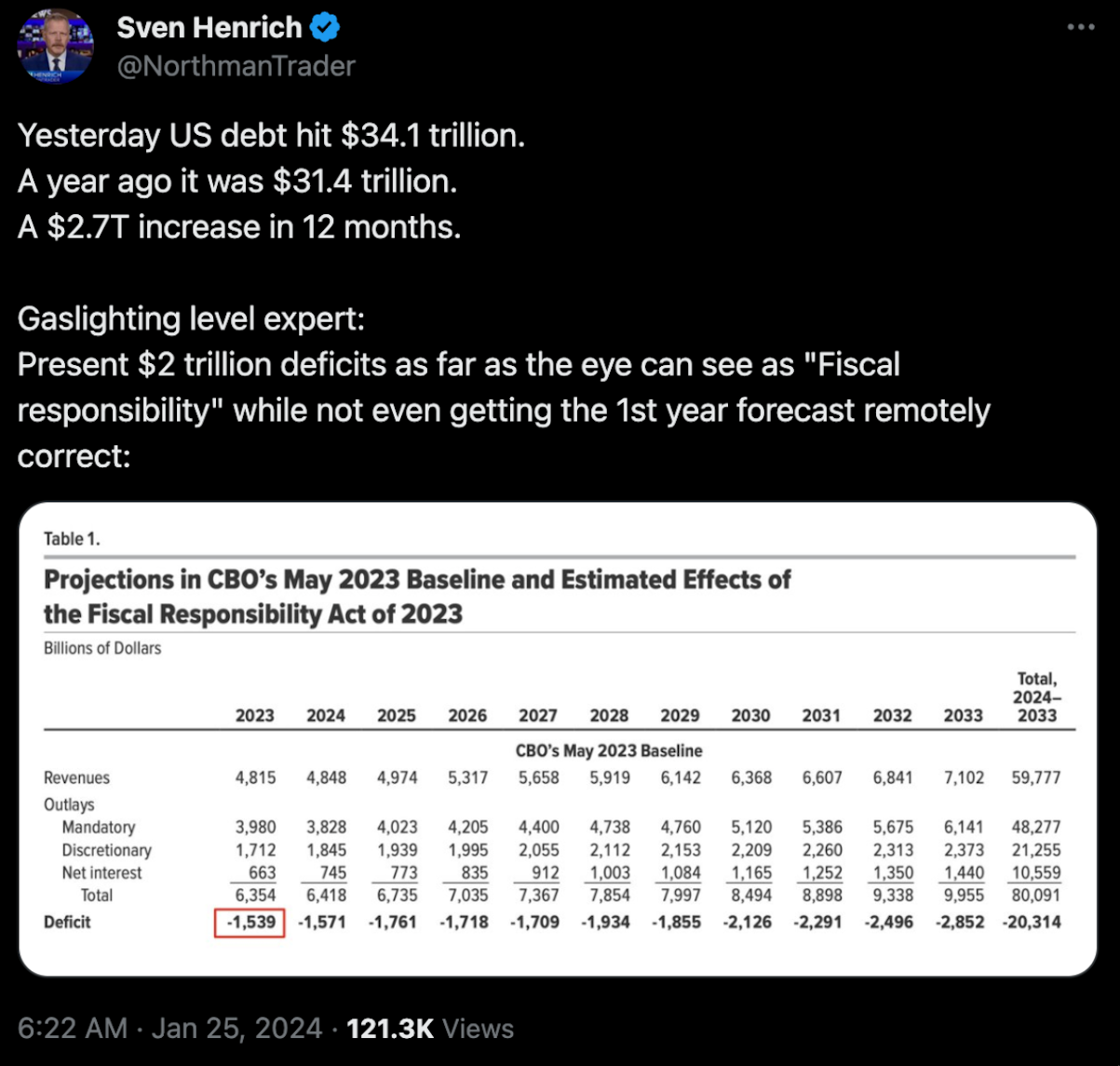

One of the main reasons why demand for Bitcoin could remain robust in the coming years is the precarious state of the US’s finances and elected leaders who apparently never learned the lesson that you shouldn’t spend money you don’t have on things you don’t need.

US debt has been increasing at an alarming rate as the government continues to spend like there is no tomorrow. Sven Henrich notes below that the debt has increased by a whopping $2.7 trillion in the last 12 months alone.

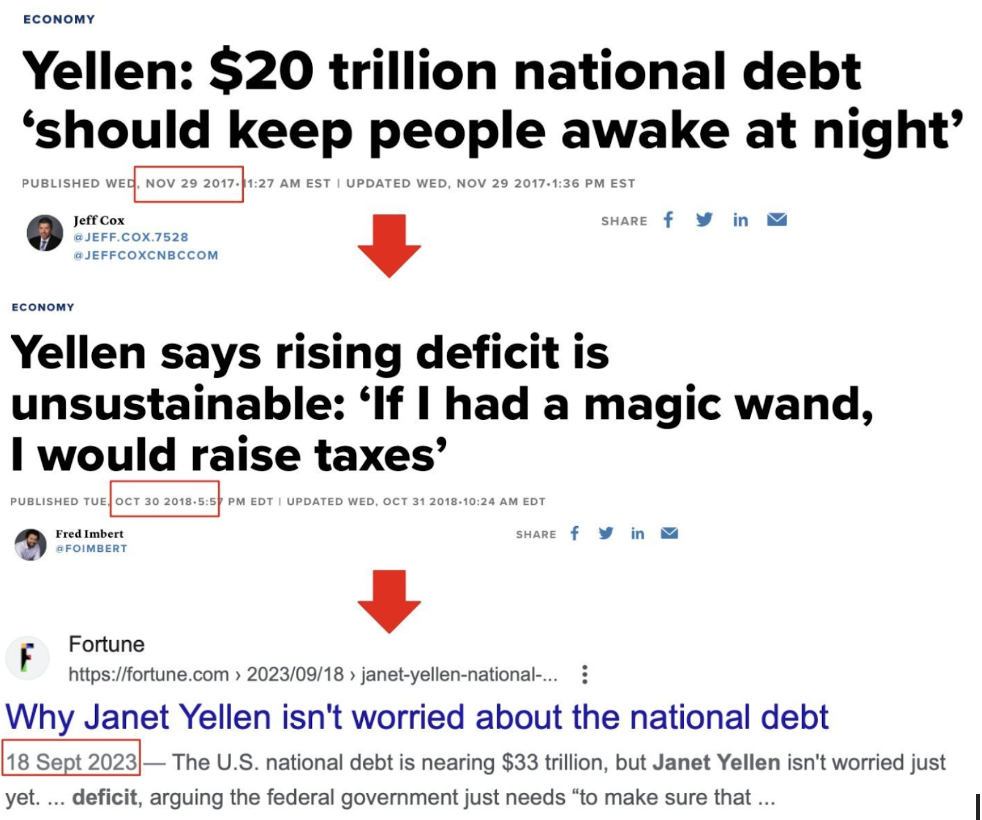

US Treasury Secretary Janet Yellen is publicly stating that there is no reason to worry about the debt, which is interesting considering that a few years ago she was saying the national debt “should keep people awake at night” when the national debt was a fraction of what it is today.

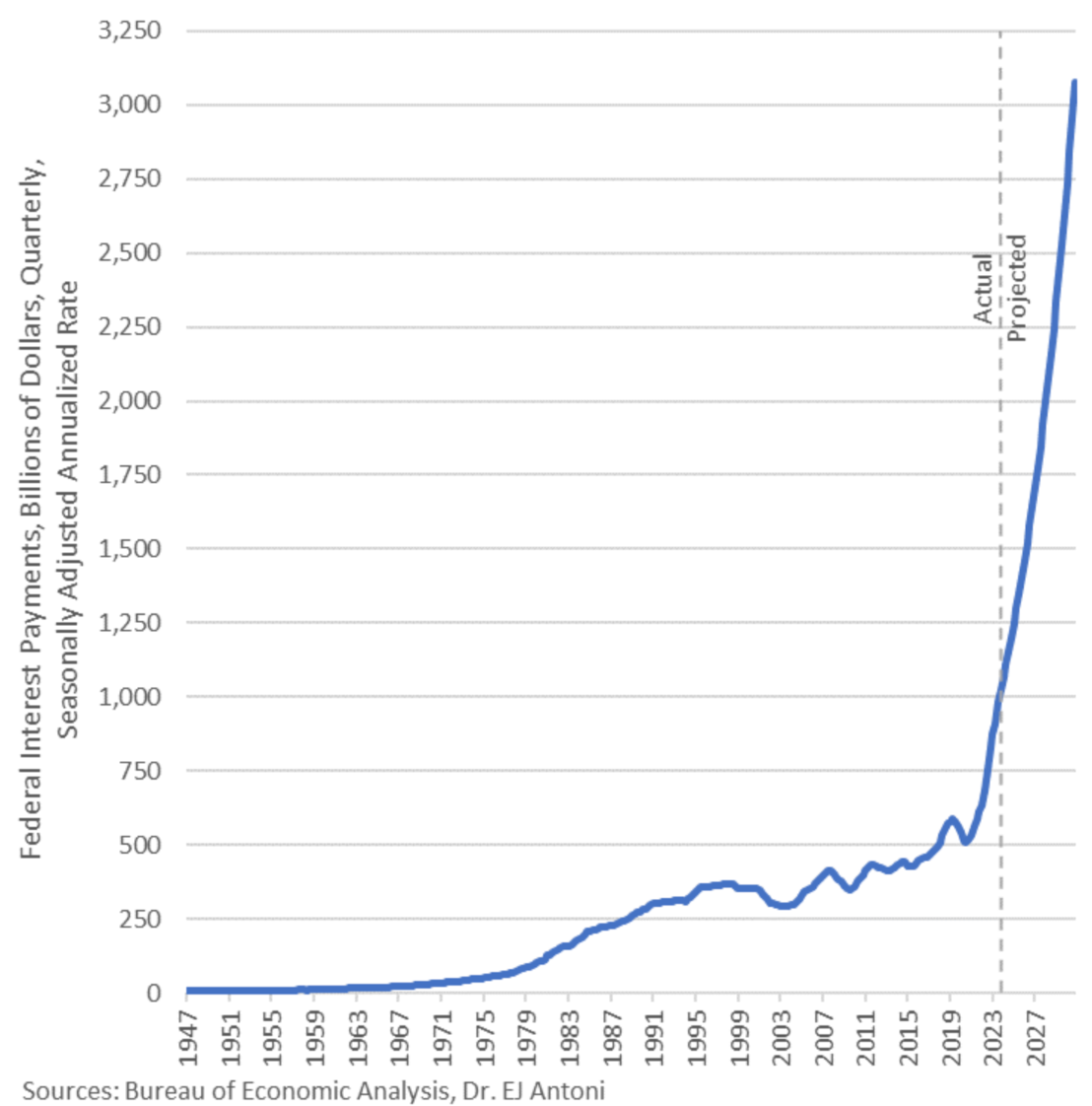

What is especially concerning is how interest on that mountain of debt recently eclipsed $1 trillion according to the Q$ GDP report. Annualized interest on the federal debt is projected to be over $3 trillion by 2030.

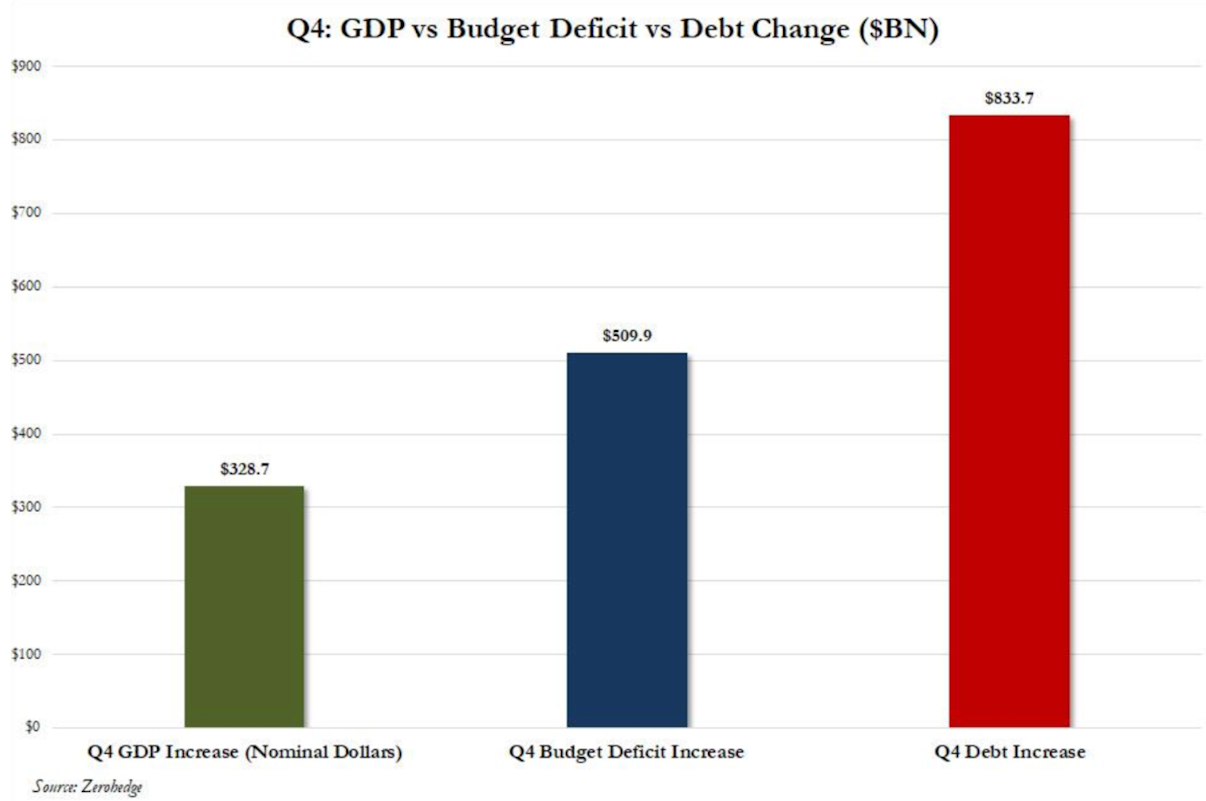

This is not sustainable. Despite these scary projections, US politicians continue to spend. People point to the recent above-average GDP print (3.3%) as a sign that the economy is firing on all cylinders when, in reality, the economy is being bolstered by multi-trillion dollar deficits.

According to the data below, it now takes $1.55 in budget deficit to generate $1 of GDP growth and takes over $2.50 in new debt to generate $1 of GDP growth.

In other words, as the government continues to spend to prop up the economy, it will take more and more debt-driven spending to achieve the same desired effect. It bears repeating — this is not sustainable.

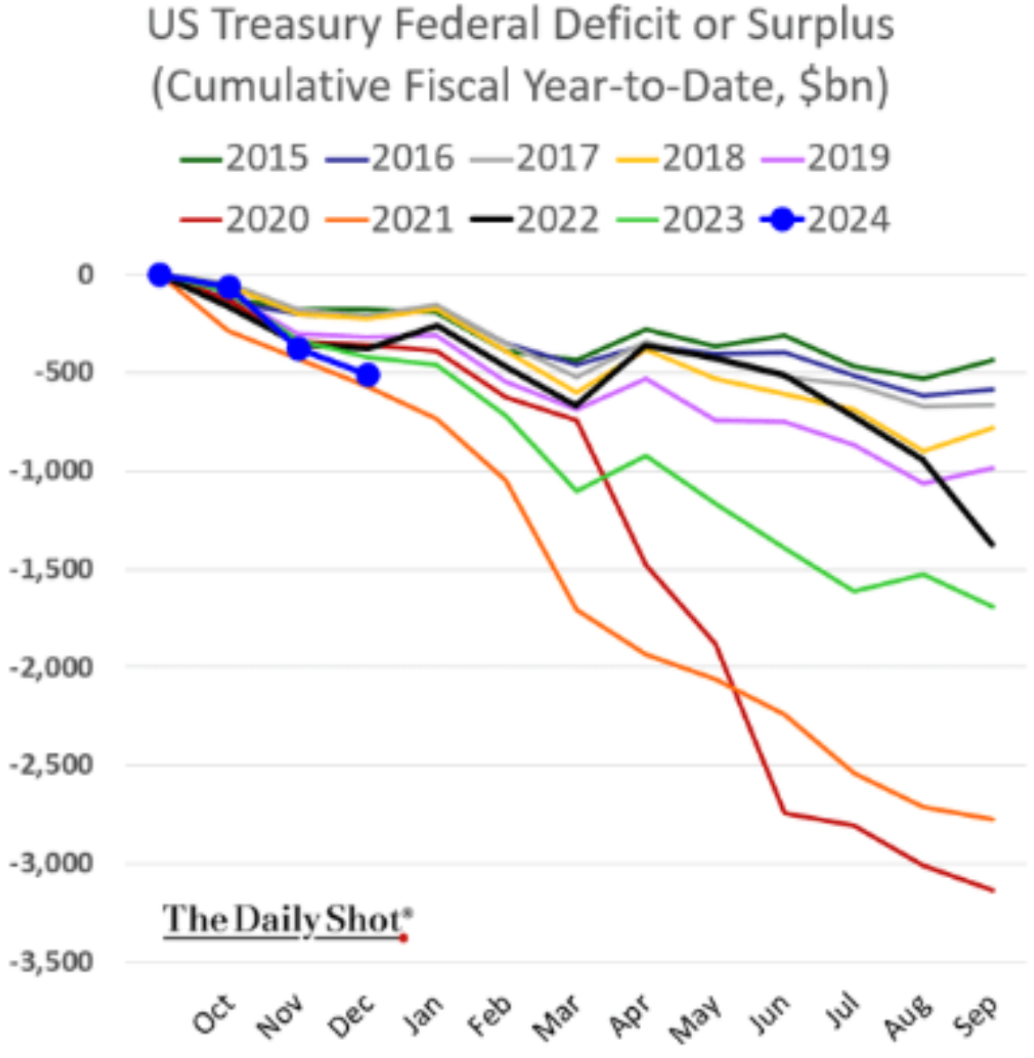

All of this deficit spending leads to increased economic activity, which leads to increased corporate earnings, which leads to increased stock prices. Is it really a surprise that all of the major stock indices have made new all-time highs as we’re on track to run deficits as large as 2020 and 2021?

This level of spending is bound to keep the economy running hot, which is inflationary. If it continues in 2024 at the current rate, and the Federal Reserve does cut rates as the market expects, then these policy choices could act as a tailwind for all asset prices moving forward.

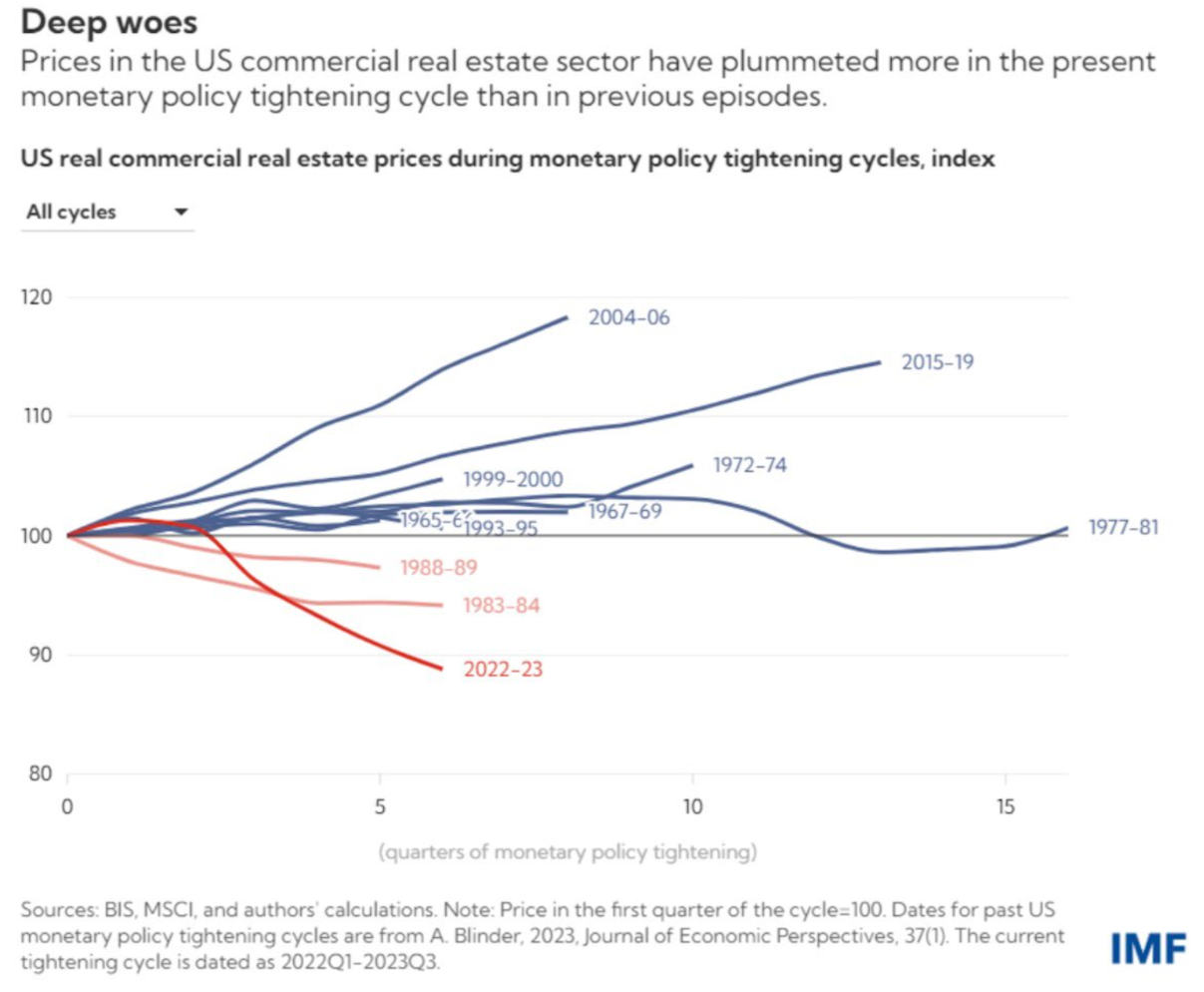

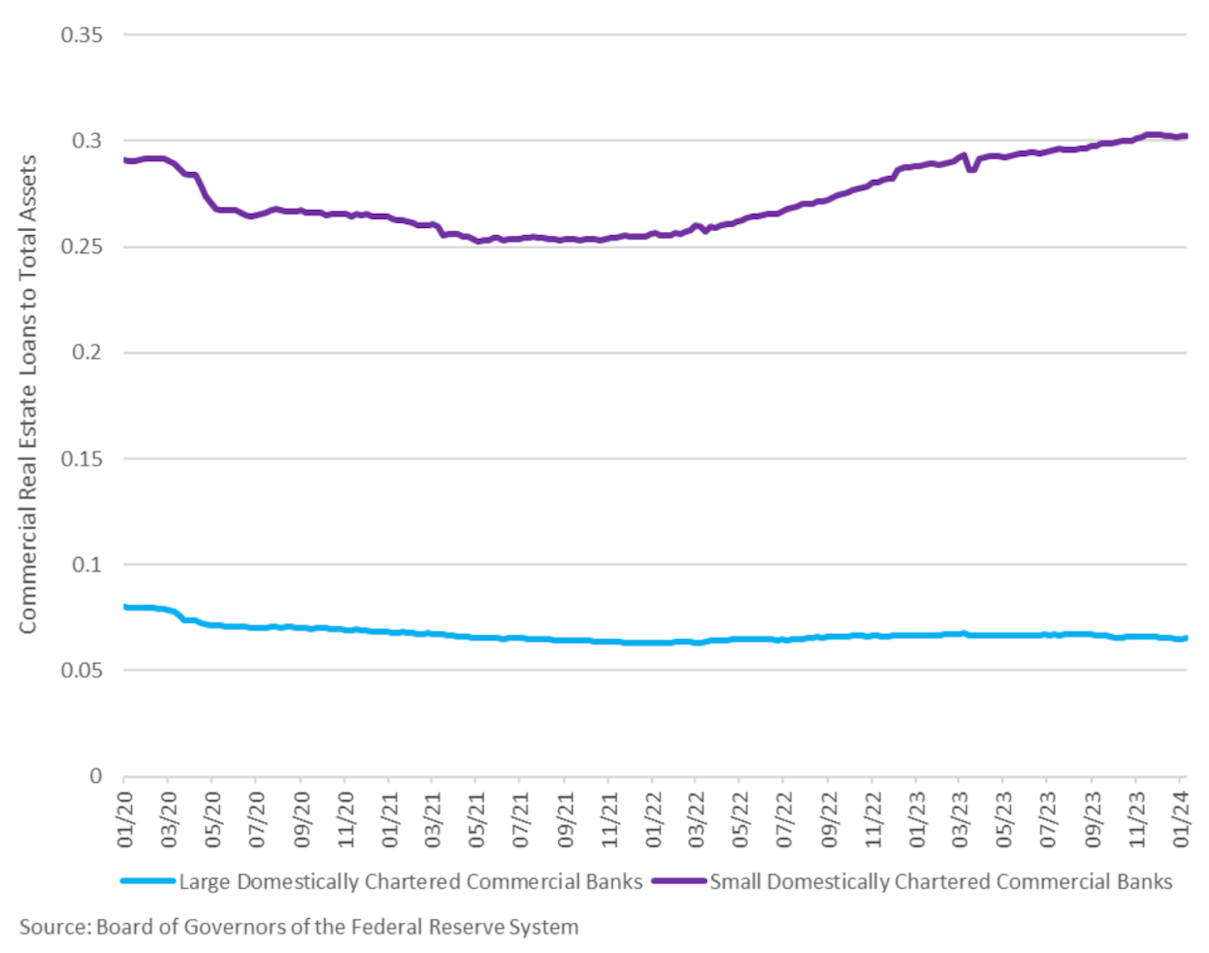

Of course, all of this could change if we start to see these higher interest rates start to really impact the economy in a meaningful way. Some sectors appear much more vulnerable to the current rate environment than others including commercial real estate and regional banks.

Prices in US commercial real estate have dropped 11% during this monetary tightening cycle, the most ever compared to previous tightening cycles.

Some economic research firms are expecting CRE prices to fall an additional 10% in 2024.

CRE loans today make up around 30% of smaller regional banks' total assets, so you can see why this could become a big problem.

Dr. EJ Antoni

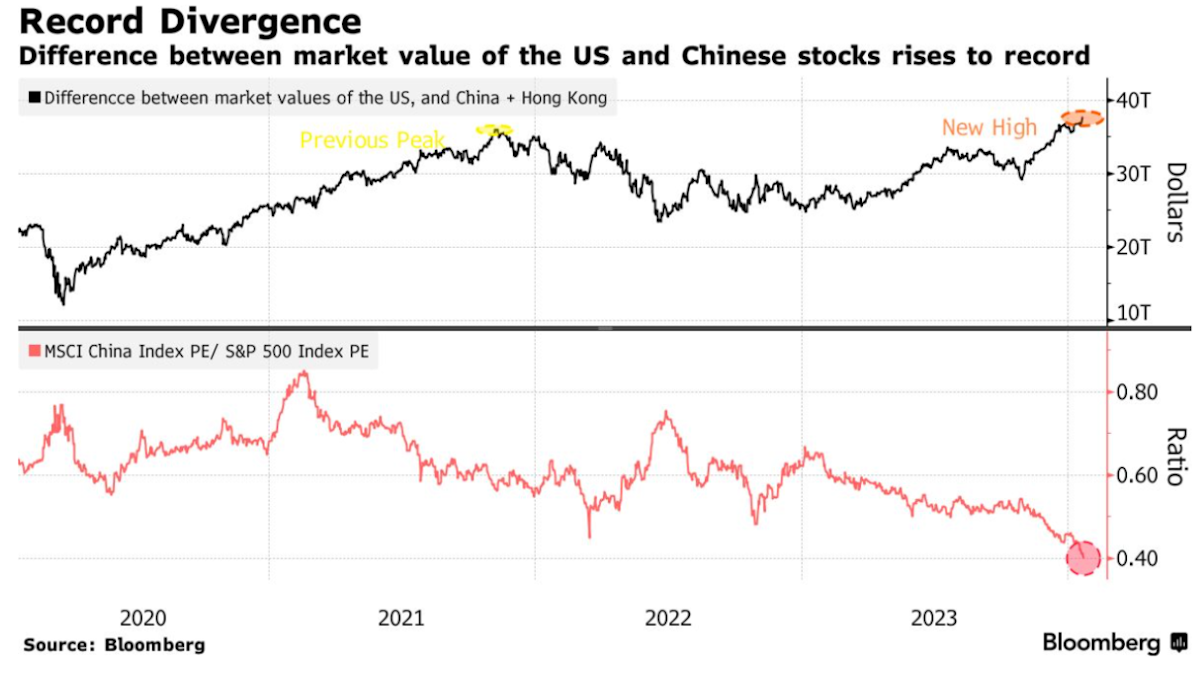

We are seeing what can happen to a country’s economic growth outlook when a toxic real estate market starts to break down across the ocean in China.

It’s becoming more and more evident that China is going through some sort of financial/economic crisis, or at minimum, is on the verge of one.

As the US stock market has soared, the Chinese and Hong Kong stock markets have plummeted. The difference between the market value of US and Chinese stocks now sits at a record level.

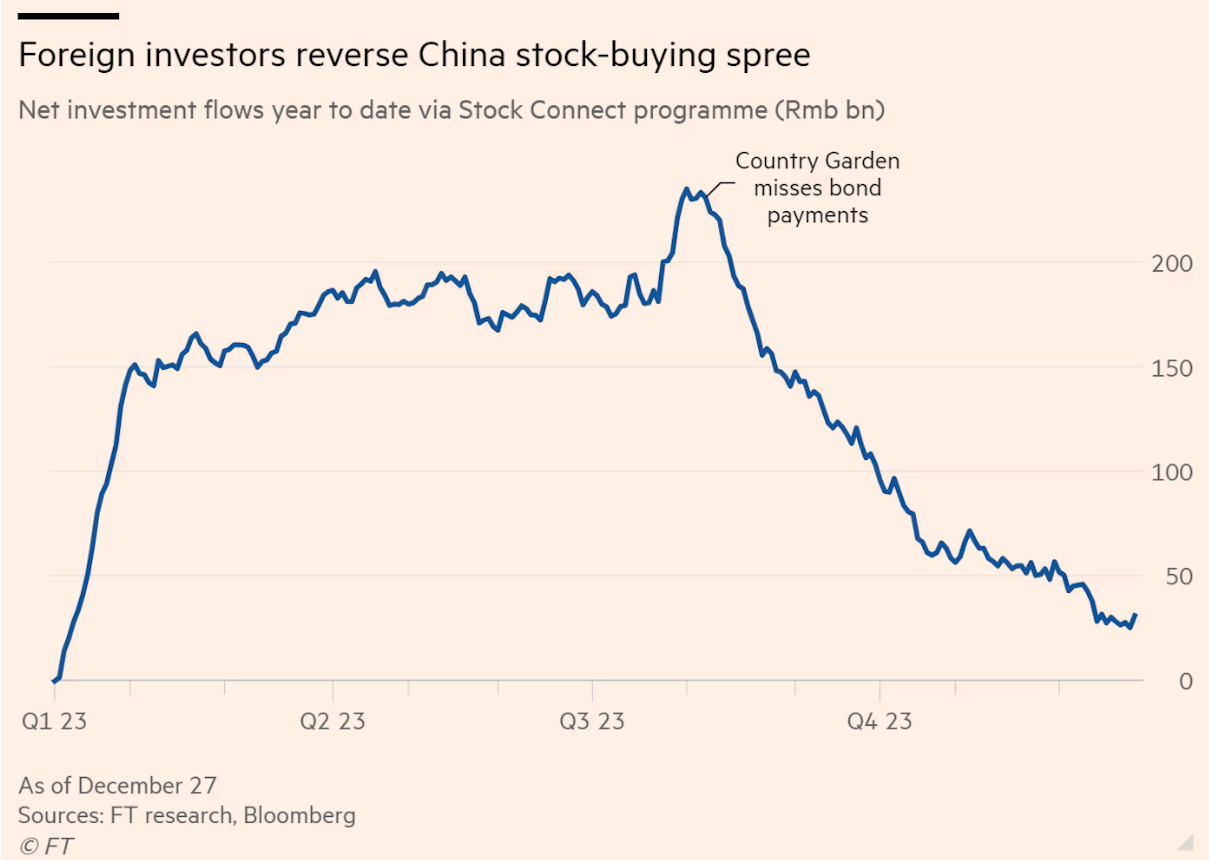

The Chinese and Hong Kong stock markets have suffered as foreign investors have been selling their stock holdings in droves. China’s post-pandemic growth has disappointed, the real estate crisis has spooked investors, and the government regime has become even more controlling, which increases risks for foreign investors.

Foreign investors sold about 90% of the $33 billion of Chinese stocks they had purchased earlier in the year, and have continued selling this year.

Furthermore, foreign purchases of Chinese stocks dropped to an 8-year low in 2023.

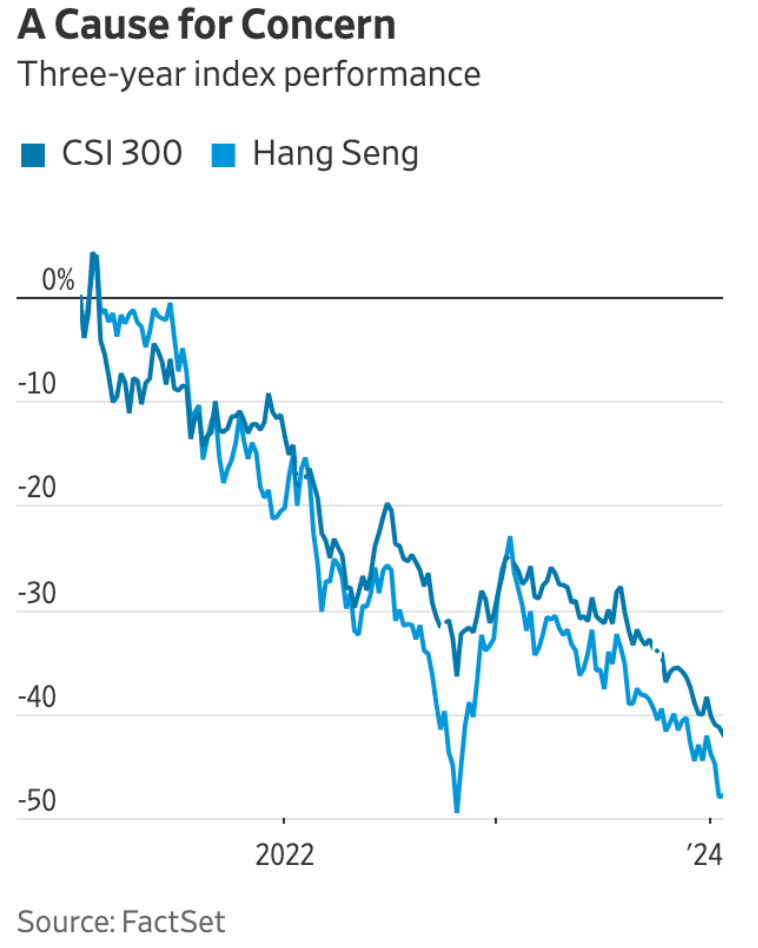

This is one key factor for why the CSI 300 Index and Hang Sang are now down around -40% from their highs in 2021.

This poor performance has led to the Chinese government contemplating intervening in their stock market to help provide support.

However, historically, whenever governments attempt to flood their stock market with liquidity, it only offers a temporary reprieve to the stock selling. This would be akin to a bandaid for a bullet wound.

The fact that the Chinese government is contemplating this stimulus package does provide just more evidence of the prevailing modern central bank mentality to intervene in financial markets whenever things go wrong. No longer do these central bankers believe in the principles of free market capitalism or the concept of creative destruction. Instead, they believe their mission is to smooth out business cycles with their interventionism. Of course, this only leads to the creation of even greater asset bubbles and further misallocation of capital.

It leads one to wonder if the CRE loans cause a regional bank crisis 2.0, will the regulators step in once again to “save the day?” I know what I would bet on.

Probably the most interesting development this week out of China was data that more Chinese are turning to Bitcoin as their stock market crashes.

Despite Bitcoin trading and mining being banned in the country, Chainalysis reports that peer-to-peer trading volume in China has jumped significantly in 2023 compared to 2022. With an estimated $86.4 billion in transaction volume, China jumped from the 122nd country in the world in 2022, to the 13th in the world in 2023.

A Chinese resident quoted in the article stated that he views Bitcoin as “a safe haven.”

This article highlights two things:

It’s incredibly hard for governments to ban their citizenry from using Bitcoin.

More and more people are trusting Bitcoin with their savings over traditional asset classes and banks.

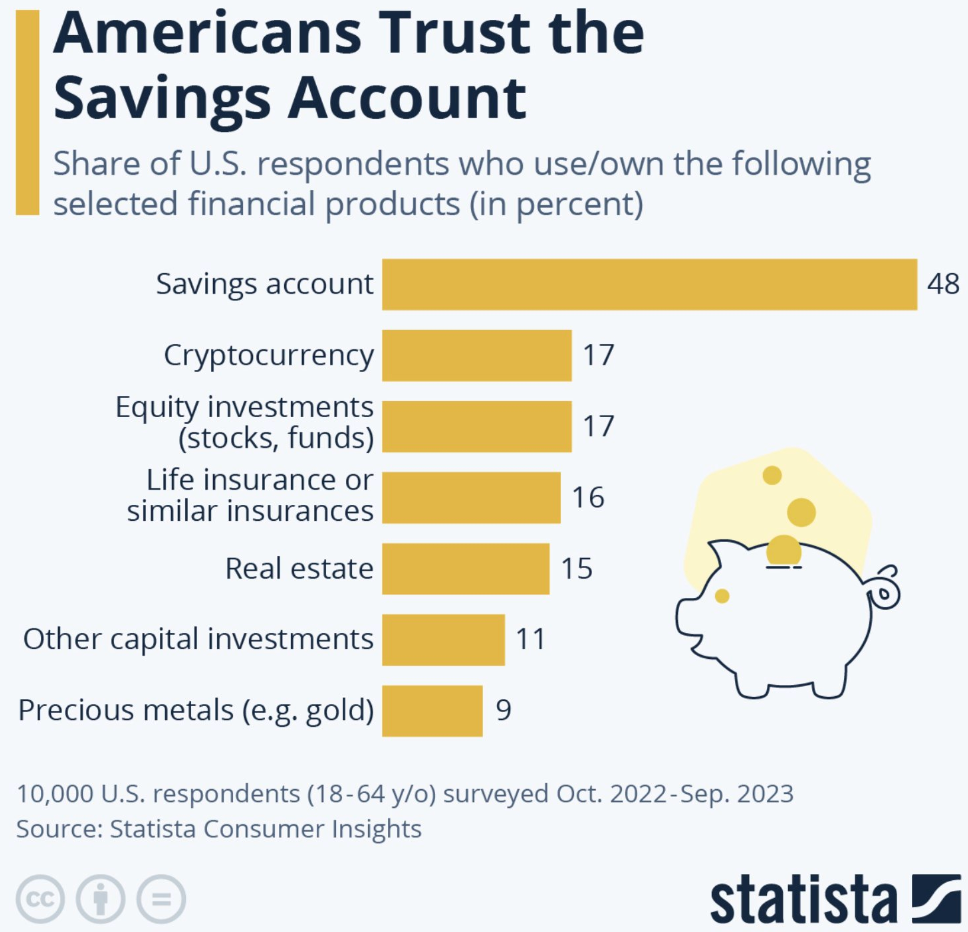

This story out of China comes in a week when Statista released the findings of a new survey of 10,000 Americans that found that, outside savings accounts, “cryptocurrency” was the most used or owned financial product.

The world is changing rapidly. Never before have the citizens of the world had a digital store of value accessible to them with a smartphone and internet connection that can protect their savings from debasement and confiscation.

The landscape of Bitcoin ETFs and the broader financial market is witnessing significant shifts. The precarious state of the US fiscal outlook, with its soaring national debt and unsustainable deficit spending, poses serious risks to the long-term health of the economy. The situation is only further complicated by challenges faced by countries like China, where increased Bitcoin adoption amid a stock market downturn reflects a growing global reliance on alternative assets to protect their savings. The integration of Bitcoin into Wall Street financial products, combined with the reckless nature of government fiscal policies, suggests a future where financial instability may hinge on the balance between innovation and traditional policy decisions.

Market Overview

Tradingview, Prices as of 01/26/24

Sam Callahan is the Lead Analyst at Swan Bitcoin. He graduated from Indiana University with degrees in Biology and Physics before turning his attention towards the markets. He writes the popular “Running the Numbers” section in the monthly Swan Private Insight Report. Sam’s analysis is frequently shared across social media, and he’s been a guest on popular podcasts such as The Investor’s Podcast and the Stephan Livera Podcast.

News

More NewsThoughts on Bitcoin from the Swan team and friends.

Swan Guard brings world-class Bitcoin security with advanced risk controls, scam defense, and expert support — vigilantly protecting your Swan account and safeguarding your Bitcoin.

After managing a Swiss gold fund for 8 years, I realized Bitcoin surpasses gold as the ultimate store of value. Here’s why every gold investor should study Bitcoin closely.

Ben Werkman joins Swan as CIO. New LBE primer explains key concepts, implementation steps, risk management, and valuation approaches.