Swan Private Insight Update #20

This report was originally sent to Swan Private clients on February 13th, 2023. Swan Private guides corporations and high net worth individuals globally toward building generational wealth with Bitcoin.

This report was originally sent to Swan Private clients on February 13th, 2023. Swan Private guides corporations and high net worth individuals globally toward building generational wealth with Bitcoin.

The benefits of saving for your retirement in tax-advantaged retirement accounts are meaningful for almost anyone. But this is especially true when you own an asset with tremendous upside appreciation potential.

Just ask Peter Thiel!

Peter Thiel — American billionaire co-founder of PayPal and Palantir — reportedly owns a Roth IRA, which contains assets valued at $5 billion. Thiel acquired a large number of shares of PayPal in 1999 in his Roth IRA when PayPal’s valuation was very low. Fast forward a couple decades, PayPal is valued in the tens of billions, and Thiel’s shares have grown in value to a comical extent. The kicker is that the gains on his shares are entirely tax-free because they occurred inside a Roth IRA!

Not all investments have this potential for such significant returns over 20 years. But I would argue that early-stage startup shares and Bitcoin have this unique appreciation potential.

In this article, we’ll discuss the tax advantages that come with US-based retirement accounts — particularly Traditional IRAs and Roth IRAs. We’ll also cover the differences between the two.

Next, we’ll quantify these tax advantages with a few examples. And we’ll see how changing the inputs — such as contributions, number of years contributing, and annual return assumptions — can significantly change the outputs.

But firstly, we’d like to point out that there is another reason to want to see the proliferation of Americans holding Bitcoin in their retirement accounts. As Jeremy Showalter, Vice President of Product at Swan, has pointed out:

By bringing access to Bitcoin in retirement accounts, we can proactively position Bitcoin into a ‘third rail.’ Within a short period of time and with focused adoption, Bitcoin in Americans’ retirement savings will become an insurmountable political issue for any current or future political leader. Threats to Bitcoin will always be present. But each challenge it overcomes displays its resilience and builds more conviction in its long-term success. Bitcoin adoption grows from understanding and more ways to save. Bitcoin retirement adoption is likely the greatest defense for Bitcoin and a great long-term offense against inflation.

VP of Product at Swan

American politicians would be taking a significant risk by putting the retirement savings of their constituents at risk if they were to change how Bitcoin is currently treated in retirement accounts. Not only would it represent them coming after the hard-earned retirement savings of American citizens, but it would also signal that they, as politicians, are willing to change the rules in the middle of the game to the detriment of their voting base. This is not a recipe for garnering trust and favor with your constituents.

The short summary is that Traditional IRAs are funded with pre-tax dollars, and Roth IRAs are funded with post-tax dollars. Let’s explore what this means in more detail.

In a Traditional IRA, your taxable income is reduced by the amount of your contribution in the year you contributed. The assets in your Traditional IRA grow tax-free until you take a distribution. Distributions from a Traditional IRA are treated and taxed as ordinary income. The idea is that when you expect to take distributions from your Traditional IRA, you will be in a lower tax bracket than when you were contributing to it.

Let’s say you contribute $6,500 to your Traditional IRA in a particular year. If your employment income for the year was $100,000, your taxable income would be reduced to $93,500. So the first benefit of a Traditional IRA is that you lower your tax bill in the present day because you lowered your taxable income by $6,500. Going forward, the $6,500 in your Traditional IRA would grow tax-free until you decide to take distributions out of the Traditional IRA, which most people would do at some point after the age of 59 1⁄2. You could repeat this process each year for many years in a row. As mentioned previously, the tax rate on your distributions would be at the rate of ordinary income. If you took a distribution in a particular year of $100,000, representing all of your ordinary income for the year, you would be taxed at whatever your typical income tax rates are at that time. If your tax rate were 30%, your net distribution would be $70,000.

In a Roth IRA, your contributions are from funds you already paid taxes on. Therefore, your contributions do not reduce your taxable income in the present day. But the benefit is that the assets in your Roth IRA would grow tax-free. You would incur no tax bill when you take distributions out of the Roth IRA, which most people would do at some point after 59 1⁄2 years of age.

Please keep in mind that, in addition to federal tax rates, one has to consider the state and local taxes of your jurisdiction. In the examples below, for simplicity, we assumed one aggregate tax rate instead of breaking it out between tax rates for federal, state, and local.

Additionally, one must be aware of annual contribution limits.

Also, one must be aware of income limits before contributing to a Roth IRA.

Before we look at examples of Traditional IRAs and Roth IRAs, please note that there are additional types of U.S.-based retirement accounts. Several of these account types can be very interesting and beneficial, particularly for self-employed people. You can learn more about different retirement accounts beyond Traditional and Roth IRAs at this link.

We’ve now covered the nature and benefits of retirement accounts in conceptual terms. Let’s make this quantifiable by walking through a few examples.

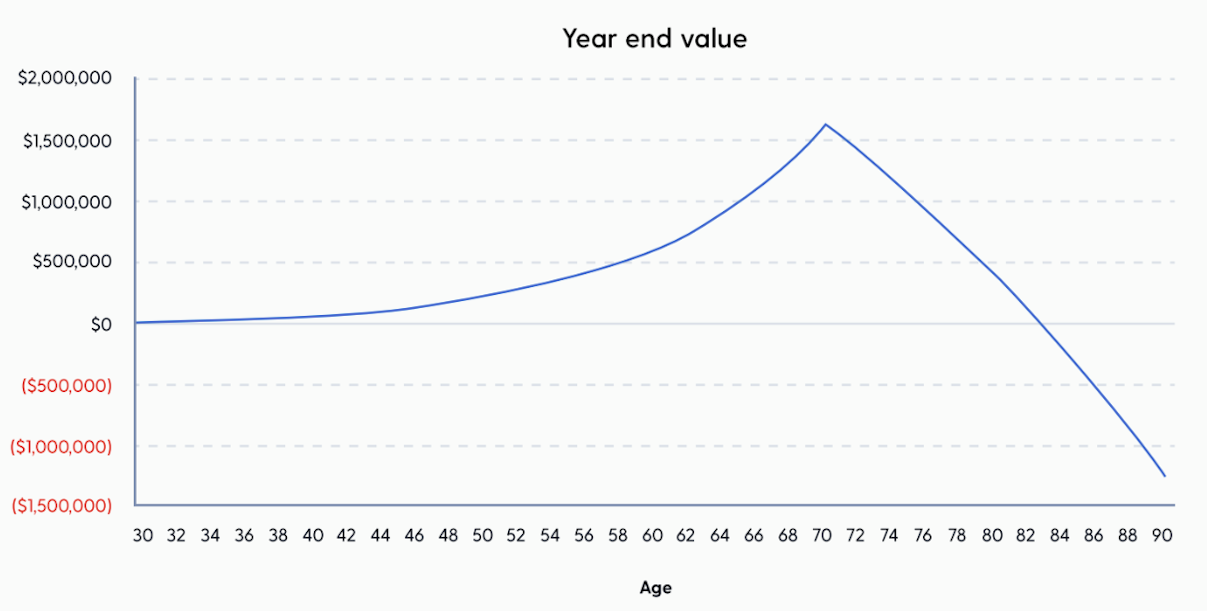

Our first example is a 30-year-old who sets up a Traditional IRA. She earns $100,000 of income per year. Her effective tax rate is 40%. She plans to retire at age 70. She contributes the max amount to her IRA each year — $6,500 until age 50 and $7,500 at age 50 and older. You can see other assumptions included below.

While the account value at retirement age shows quite a large number, it is important to keep in mind that $3.5 million in the year 2063 almost certainly will not have the purchasing power of what $3.5 million has today.

But this also means you would likely be able to contribute larger amounts to your retirement accounts in the future.

Note we did not include an assumption for CPI here. Conceptually, if you believe that CPI will average 3% per year for the rest of your life, you would take the return assumption and subtract 3%, i.e., a 10% nominal annual return becomes a 7% inflation-adjusted annual return.

In this example, you can see that our retiree maxed out her contributions yearly and earned 10% each year until retirement. As a result, she was able to grow her retirement account to ~$3.5 million by age 70 and withdraw $150k (before taxes) each year from the age of 70 to 90. At that point, she still had ~$2.3 million of assets in her IRA.—

Now let’s adjust only one input in this example. We will change the annual contribution to $3,000 per year.

Here, our retiree contributed only $3k per year. She also earned 10% each year until retirement. As you can see above, her retirement account grew to ~$1.5 million by age 70. Still, she was unable to withdraw $150k (before taxes) each year of her retirement because she ran out of funds around age 83.

—

Now let’s adjust a different input from the first example. We will change the annual rate of return until retirement from 10% to 7%.

Our retiree in this example is contributing the max each year, but her investments are returning less each year compared to the first example. As you can see, this change also significantly affects the results. Per the above tables and chart, her retirement account grew to ~$1.5 million by age 70, but she was unable to withdraw $150k (before taxes) each year of her retirement because she also ran out of funds around age 83.

Interestingly, the scenario of a 10% return on $3,000 annually and the scenario of a 7% return on $6,500 until age 50 plus $7,500 thereafter led to very similar results. It just goes to show how powerful compounding growth rates can be.

—

Let’s look at another example with the starting age changed. This time our retiree starts saving for retirement at the age of 45.

As you can see, the person who begins saving for retirement at age 45 cannot grow their assets nearly as much as the person who starts at 30. As a result, they are limited to distributions of $50k (before taxes) during their retirement.

—

Let’s look at one final example to show how things change in a Roth IRA.

As you can see, all of the assumptions here are the same as in Example 1. The only difference is that Example 1 is a Traditional IRA, while Example 5 is a Roth IRA. This leads to two key differences. Firstly, in a Roth IRA, you do not save anything on your tax bill in your years while working. Secondly, you receive 100% of your distributions because there is no tax burden on distributions in a Roth IRA. You’ll notice that the chart showing the year-end value by age is the same as the chart in Example 1. This is because Traditional IRAs and Roth IRAs both grow tax-free. As mentioned, the key difference is that distributions from a Traditional IRA are taxed at ordinary income, while distributions from a Roth IRA have no tax burden.

For most people, the best time to start saving for retirement is the very first day you start earning money. The next best time is today. Better late than never, as they say.

Given there are multiple assumptions at play, there are many different ways to adjust the assumptions and see how the results change. With that said, the key variables are your annual contributions, the number of years contributing, and your annual return.

While no one has complete control over these variables, you likely have the most control over your annual contributions. Do your best to max out your annual contributions.

Regarding your number of years contributing, unless you have a time machine, your only option to max out your number of years contributing is to start today. Not six months from now… not two years from now… start now!

Regarding your annual return, few assets have as attractive a long-term appreciation potential as Bitcoin (this is also known as an asymmetric return profile if you are trying to sound like you work on Wall Street). It is our view that you are giving yourself the best chance for outsized long-term returns by holding an asset like Bitcoin.

You’ll notice that in all of the examples above, the largest annual return that we assumed was 10%. While 10% annual returns lead to incredible growth in one’s assets over decades, some people believe Bitcoin will appreciate at a faster rate than that. Any scenario where one’s retirement assets appreciate at more than 10% per year for multiple decades results in numbers that look almost silly — quite like Peter Thiel’s situation!

If you would like to have a conversation about your particular situation, including your assumptions and how they would impact your retirement assets and your retirement plan, please reach out to your Swan Private rep, who would be happy to discuss this with you!

Additionally, if you’d like to play around with the inputs and immediately see how the results change, the retirement plan calculator at this website is a simple and helpful resource: https://www.bankrate.com/retirement/retirement-plan-calculator/

If you have existing retirement accounts that are invested in traditional financial assets, and you’d like to reallocate some or all of those assets into Bitcoin, you can do this via a transfer or rollover.

A transfer is a like-for-like tax-advantaged movement from Traditional IRA to Traditional IRA or Roth IRA to Roth IRA. All transfers into your Swan IRA must be in the form of USD cash. We strongly recommend that you transition your investments to USD cash (rather than cash equivalents or money market funds) before initiating the transfer request.

A rollover is a movement from an existing retirement account — such as SEP IRA, Solo 401k, 401k, 403b — to an IRA. A rollover is coordinated primarily by the customer with their existing retirement custodian. Before completing a rollover to your Swan IRA, you must liquidate your other retirement account to USD cash.

If you would like to convert an existing pre-tax retirement account into a Roth, you can do a conversion at your existing financial institution, and then you can complete a transfer into a Swan Roth IRA.

You can choose between setting up a Swan Traditional IRA or Swan Roth IRA and then transfer or rollover from an existing SEP IRA, SIMPLE IRA, 401k, 403b, TSP, etc., for both pre-tax and post-tax retirement options. See the graphic below, which we adapted from the original on the IRS website. Please note that we (Swan) added the asterisks to indicate what type of account you would need to start with to have the ability to transfer or rollover into a Swan Traditional IRA or Swan Roth IRA.

Lastly, please note that there exists an option to set up something referred to as a Checkbook Self-directed IRA LLC structure. The idea here is to set up an LLC that buys and holds Bitcoin. You also set up an IRA, which owns the LLC. This structure is often used for owning real estate in an IRA, but some people have used this structure to own Bitcoin in an IRA. It can allow you to take self-custody of your Bitcoin in an IRA if you are comfortable with the current legal and regulatory uncertainties associated with this. Please speak with us if you are interested in pursuing or learning more about this option.

Swan is a leading Bitcoin financial services company with more than 120,000 clients and 170 employees, operating globally. Established in 2019, Swan helps individuals and institutions to understand and invest in Bitcoin. The Swan app simplifies Bitcoin purchases with instant and recurring buys. Swan IRA provides a tax-advantaged solution for saving Bitcoin in retirement accounts.

For HNWIs and businesses, Swan Private provides white-glove service for large purchases, treasury solutions, and employee Bitcoin benefits. With Swan Vault, clients can easily custody their own Bitcoin with peace of mind. Financial advisors trust Swan Advisor for client Bitcoin allocations, backed by world-class custody and educational content.

Swan Managed Mining provides clients with fully segregated and dedicated mining operations, catering to their unique requirements, opportunities, and strategic advantages. Swan prides itself on exceptional client service, making Bitcoin accessible to all. For more information, please visit swan.com.

John is the Managing Director of Private Client Services at Swan Bitcoin. He previously spent 13 years on Wall Street, where he was a Portfolio Manager and Insitutional Investor at Goldman Sachs.

If you’d like to learn more about the Bitcoin network and protocol function, you can download Inventing Bitcoin by Yan Pritzker for FREE!

News

More News