Swan Private Insight Update #15

This report was originally sent to Swan Private clients on September 12th, 2022. Swan Private guides corporations and high net worth individuals globally toward building generational wealth with Bitcoin.

This report was originally sent to Swan Private clients on September 12th, 2022. Swan Private guides corporations and high net worth individuals globally toward building generational wealth with Bitcoin.

In 1968, four Vice Presidents of modest regional banks emerged from the Altamira Hotel on the hillside of insignificant Sausalito, California, unshaved and unshowered, with a set of beliefs, ideas, and principles that would change the world of money.

Sam Johnson, a boisterous Boston Irishman, Jack Dillon, an eclectic World War II veteran, Fred James, a smooth-talking southerner from Memphis, and Dee Hock, a poor boy from rural Utah, battled for four straight days on the question, “if there were no constraints whatsoever, what would be the nature of the ideal organization to create the world’s premier system for the exchange of value?”

After working in the credit card and financial services industry for over 75 years between them, the four knew all too well that the system was broken. They needed to analyze the problems from first principles, viewing the issues as they were, as they are, as they might become, as they ought to be.

They realized that a bank’s essential function was to custody, exchange, and loan money.

But what was money?

Money was not a coin, currency, or credit card. Those were simply forms of money that facilitated its movement, but not its essential function. Money was something entirely different.

Money was whatever was customarily used as a measure of equivalent value and a medium of exchange.

Coins now only contained trace amounts of precious metals. The paper and currency, on which checks and banknotes were printed had become as abundant as air itself and could be printed into oblivion.

So, it wasn’t the metal or the paper that was valuable.

If the physical objects contained no real economic value, then what did?

They concluded that it was the alphanumeric data expressed on the objects themselves that were the expression of value.

Money had become guaranteed alphanumeric data expressed in the currency symbol of one country or another, and therefore, banks were institutions for the custody, loan, and exchange of guaranteed alphanumeric data!

With the proliferation of computers, chips, and communication systems, these men envisioned a future in which money would become nothing more than digital information, manipulated, and stored in computers and networks, which could travel at the speed of light at minuscule costs, anywhere across the world.

They concluded, “Any institution that could move, manipulate, and guarantee digital data transmittance in the form of arranged energy impulses, twenty-four hours a day, seven days a week, around the globe, in a manner that individuals customarily used and relied upon as a measure of equivalent value and medium of exchange would become the largest value exchange network in the world.”

This was the big idea that would fuel their vision that led to the creation of VISA. VISA became the world’s first Trillion dollar value network. Today, Visa is supported by 15,100 financial institutions, facilitating over $13 trillion in annual payment volume, across 3.8 billion cardholders, accepted at 100 million merchant locations in over 200 countries.

Bitcoiners should take note of the legacy, the history, the successes and the pitfalls of Visa.

Dee Hock, VISA’s founder was driven by deeply held beliefs that the stranglehold of two-hundred-year-old banking oligopolies would be shattered by VISA. Nation-state monopolies would no longer control the world through the issuance and control of currencies. It would matter little that traditional banks or governments were the settlers of last resort. What would matter instead, he believed, would be adeptness at handling and guaranteeing alphanumeric value data exchange. He turned out to be right.

This vision birthed from a small hotel in Sausalito, by four regional Vice Presidents with no capital, power, or authority, stood in direct opposition to the cartel of the current powers like Citicorp, American Express, Bank of America, Chase Manhattan, and even the Federal Reserve.

To describe the creation and success of VISA as “improbable” would be a gross misrepresentation. “Practically impossible” seems much more fitting.

The story of VISA should give us hope. Many principles instilled into VISA should serve as a moral compass and guidepost for Bitcoin, while other small but critical mistakes should serve as a cautionary lessons to avoid.

This is the story of a small network of voluntary participants who overthrew global corporations’ power through a passionate belief in principled ideas. This is the story of VISA. This is the story of when Plastic became Money.

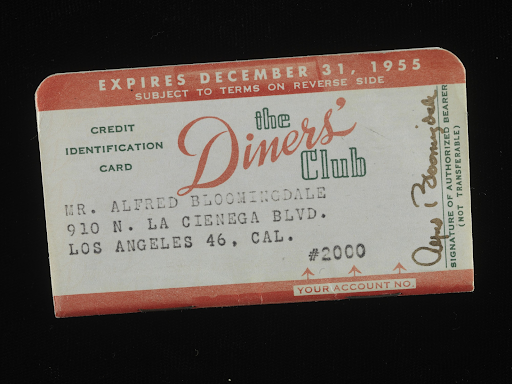

In 1950, the Diners Club launched the first modern credit card when a New York lawyer left his wallet at home during lunch with a client. This spurred the idea of customers charging meals to a cardboard card, and afterwards the restaurant later sending the bill to the Diners Club. Buy now, pay later.

But this concept is not new. Humans began recording transactions on Cuneiform 5,000 years before as a means to account for debts and debtors.

In the civil war, stamped credit coins allowed merchants to identify customer accounts by matching the numbers stamped on them with the accounts at the store.

In the early 1900s, Western Union and American Express created travelers' cheques and cards which allowed consumers to conveniently and more securely travel and redeem money for single purposes around the world.

After the Diners Club launched the first modern credit card in 1950, American Express pioneered the first plastic card in 1958, effectively ushering in a new form of money beyond coins and banknotes.

The rise of credit cards instituted a new gold rush in financial services. Up until this point transactions primarily consisted of transactions between two parties — the buyer and the seller.

Now the system needed to become infinitely more complex with the stakeholders ballooning to consumers (cardholders), merchant banks (receiving banks), issuing banks (card issuers), merchants (service providers), and network providers (3rd parties who helped facilitate transactions). All this convenience came with a lot of middlemen.

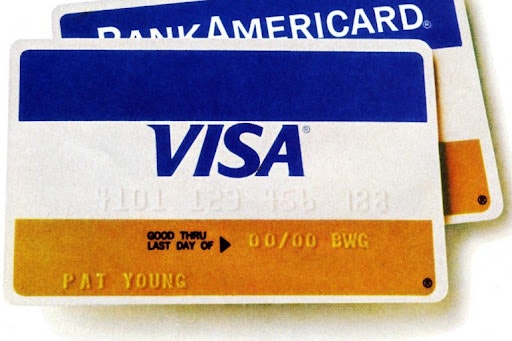

In 1966 after the launch of BankAmericard and the American Card, the frenzy to claim market share in this new and unpredictable market was on. At the time, there were no magnetic strips on cards and no electronic card readers on point-of-sale systems. To perform a transaction, cards were placed inside of a manual imprinter and a sales draft stamp was pressed on top to create an impression. The devices were called “zip zap” machines. There were no electronic systems for authorizing transactions.

Every piece of data for a transaction required keypunching each digit of information by hand into a four-by-six inch piece of cardboard via a typewriter at the end of each day, which was then fed into a computer the size of a refrigerator, and printed out into huge binders to be manually submitted to a bank at the end of each day to be cleared and settled across banks.

Criminals of course saw the bonanza and sensed an opportunity to use credit cards to purchase items, and would flee to different parts of the state or country before those transactions settled days later, without a trace.

By 1968, the industry was completely out of control, and needed a better form to transact, with greater certainty, security, and at greater volume. To create the premier system for the exchange of value, there needed to be major improvements.

Innovations like the electronic point of sale terminal, electronic descriptive billing, magnetic strip technology, debit cards, check guarantee systems, redundant data centers, automated teller systems, Moore’s law with the decrease in data center costs, the expansion of the internet, the investments in radio and telecommunication lines. The list goes on and on.

While those were essential, they were inconsequential to the most important innovation that Dee Hock and VISA brought to this world. VISA was born out of a committee of unpaid, volunteer bank executives and employees who were Franchise members of the BankAmericard credit card program. The committee members would convene to discuss the issues surrounding the circus, which was the credit card market at the time. Virtually every one of them had full-time jobs during the day, and each worked on different issues surrounding legal, marketing, operations, technology, and financials by night time.

Dee Hock was the only primary full-time member. As a principled and strongly convicted man, he convinced his boss, Max Carlson, to let him work on this concept full-time because if not, he would not idly sit back and continue to watch the disarray that it was in.

He knew that this value exchange network needed to be more than just technological innovation. There needed to be innovation in the type of organization it was to bring this audacious idea to life.

These were a few of the relevant principles that Dee believed needed to be true for this unprecedentedly collaborative organization to work:

IT SHOULD TREAT ALL PARTICIPANTS EQUITABLY

No participant should have an inherently greater or lesser ownership position or be able to negotiate, buy, or sell their position. Every participant should be able to trust that it would not be subordinate to any other and accept that it could not be superior.

PARTICIPANTS SHOULD HAVE EQUITABLE RIGHTS AND OBLIGATIONS

It must not attempt to impose uniformity. Equity would require many types of participation with differing rights and obligations, but within each type, they should be common and everyone should have the right to change their type of participation.

IT SHOULD BE OPEN TO ALL QUALIFIED PARTICIPANTS

While it must be able to create standards for eligibility, once those standards are established, all interested participants meeting the standard should be able to join.

AUTHORITY SHOULD BE EQUITABLE AND DISTRIBUTED WITHIN EACH GOVERNING ENTITY

Governing entities should be composed only of affected participants and constituted to equitably represent the interests of all relevant and affected parties. No interest should be able to dominate deliberations or control decisions, particularly management.

TO THE MAXIMUM DEGREE POSSIBLE, EVERYTHING SHOULD BE VOLUNTARY

Persuasion, not compulsion, should be fundamental. Participants should have perpetual rights of participation, but be free to leave at any time without penalty or sanction. They should have the right to utilize any commonly held properties, products, services, or assets equitably at any time for any reason connected with the purpose, but should not be compelled to do so.

IT SHOULD BE INFINITELY MALLEABLE, YET EXTREMELY DURABLE.

It should be capable of constant, self-generated modification of form or function without sacrificing its essential nature or embodied principle.

3,000 banks needed to be persuaded to surrender their licenses for membership in the new organization, National BankAmericard Incorporated (NBI), a Delaware, nonstock, for-profit, member corporation, which would later take the name of VISA.

This would be done by simply signing a document consisting of a few paragraphs, and agreeing to abide by bylaws, operating procedures, and membership principles “as they now exist or hereafter modified.”

Never before had banks surrendered their rights, power, or privilege to any organization except the government.

Never had the most powerful organizations in the world lost a public battle to an intangible entity not driven by profit, but by ideals, vision, and belief in community, collective “co-opetition” (the blending of cooperation and competition), and choice.

But, NBI would have no authority to command and control. What needed to be done was discussed upon and agreed to by each member, and driven to completion through trust and consensus.

In 1970, Dee Hock and the executive committee set forward with the largest democratic voting crusade in Corporate history. They presented their BIP (Bank Improvement Proposal 😉) and asked the issuing banks for their vote.

To their surprise, after just a few days, commitments came pouring in and after a month, they exceeded their 90% threshold goal, which would set the NBI membership initiative in motion. After hours on the phone, working through the disagreements with each bank, Dee convinced 100% of banks to get onboard.

And with that, the impossible happened.

Within a decade VISA transformed the wild west of the credit card industry into the most profitable consumer service in the world, while simultaneously reducing fraud, corruption, and costs of payments for merchants around the world.

The organization had no political, economic, social, or legal agenda. It was purely an open-sourced organization solely focused on unleashing the ingenuity and creativity of thousands of member entities who could freely innovate on the system when the need and opportunity arose.

Actual employees of NBI or VISA, although poorly compensated, and not compensated with equity, built the prototype for the modern electronic point of sale systems in less than 90 days and less than $30,000. Truly remarkable.

Visa had changed the nature of money. It eliminated the need for physical cash, for obtaining different nation’s currencies when traveling, for having to place blind trust in the authenticity and creditworthiness of a payment, and many other financial obstacles and frictions. It had achieved cooperation between countless competitive entities with no history of cooperating with each other. It was a remarkable achievement which grew and endured for decades under these founding principles.

However, five decades later, for all of its accomplishments, VISA had fallen short of its intended purposes and ideals in Dee Hock’s eyes. He lamented this, saying “by the standards of what VISA might have become and what it ought to be, it would be a lie to deny a strong sense of failure.”

What happened? In the inception of NBI, a “Proof-of -stake” mechanism was slipped into its founding documents which would eventually allow those with the most revenue to begin slightly manipulating the system and using their position and power to their advantage.

Each member would have one vote for every thousand dollars of sales volume transacted by their BankAmericard customers in the preceding year. Service fees would be one-quarter of one percent of that same sales volume. A single at-large director would be solely elected by banks having less than a minimal percent of the volume. Any bank having more than 15 percent of the sales volume of the system could appoint a director.

As transaction volumes in the system grew, the most successful members began banding together and insisting they deserved greater benefits and were entitled to lower fees, and greater privileges. This case study should serve as a stark reminder that Power corrupts all and may be the greatest addiction there is.

Bank of America, which was the leading and founding bank of the VISA network, was the chief antagonist among the big issuing banks that used their Sales Volume within the network to justify greater privileges, reduced fees, and eventually, greater significance within the network overall.

What began as a decentralized, equal rights and opportunity membership organization has slowly shifted to a top-down command and control system that has recentralized power, wealth, and rights to those with the greatest power.

Early VISA staff meetings and board meetings were openly held forums in modest circular style conference rooms, filled with wives and family members of key officials, hundreds of Directors from dozens of countries and translated into four languages, which represented the true democratic ethos of the network.

Slowly, the powers that were, demanded privacy, secrecy, in closed conference rooms, in an effort to discuss confidential matters, which might sway the network and network participants. Against Dee’s natural inclination, he slowly began to relent and turn from the original ideals VISA was founded upon.

The decentralized, modest, volunteer organization soon began to lease permanent office space, and look more like the corporations it despised rather than the ambitious network it initially sought to personify.

Proof of Stake is always deceptively and insidiously centralizing.

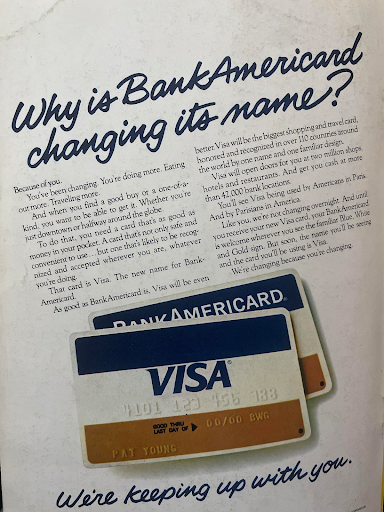

VISA is no longer the chaordic (chaos-yet-ordered) and egalitarian entity it was founded as. It is now a for profit, quasi-governmental, quasi-political, publicly traded company that reorganized to this structure in 2006, after seeing the success of Mastercard’s IPO.

In spite of my pride in all that VISA demonstrated about the power of a chaordic concept of organization and all the things it has accomplished, I do not believe that VISA is a model to emulate. It is no more than an archetype to study, learn from, and improve upon.

With Bitcoin, like VISA, through a whitepaper, open-source code, and many members autonomously and collaboratively volunteering themselves to a cause, something extraordinary and unprecedented is underway. It is a set of beliefs and principles that have established and are growing the world’s first purely peer-to-peer version of electronic cash, allowing payments to be sent directly from one party to another without going through a financial institution. It aims to become the world’s premier system for the exchange of value.

Bitcoin’s network is a physical conglomeration of autonomous people, energy, transactions, computers, and code, all working seamlessly through consensus, community, competition, and cooperation.

But more than that, it is a belief system enforced via code. One that is open and freely available for all who choose to participate in its current or modified state. A system that was created to solve the glaring and obvious problems created by our global banking elite that plague us today.

A system that was born from the creativity and ingenuity of ordinary people and not imposed by people through coercion or manipulation.

The parallels are striking. The implications of failure are much more massive now than they ever were in 1968.

The credit created bubble that began with the first credit card at the Diners Club in 1950 has set in motion a global black hole of debt around the world, whose energy sucks the life out of the middle-class and global poor across an event horizon of no return, back to the governments and wealthy on the other side.

In the preindustrial age, our economy was driven by hand-crafting. Men and women, utilizing muscle power to create economic flourishing. In the industrial age, we replaced hand-crafting with machine crafting. Removing the need for human labor, ingenuity, and creativity.

We are now squarely in the information age. Where economic flourishing is driven by “mind-making”. Software is the tool by which we shape information, which can be thought of as thoughtware, or a product of our thoughts, with computers acting as our employees, and we as their handlers.

Dee Hock believed that the greatest antidote to the mass manipulation of minds through software was to create chaordic organizations, like his original intent for VISA: Organizations that can self-organize and self-govern in ways characteristic of nature itself, naturally blending chaos and order which allows our world to heal itself from the desire for certainty and control.

Dee believed chaordic organizations are capable of restoring harmony between themselves, the environment, and the human spirit — able to withstand the enormous increase in societal diversity and complexity brought about by the explosion of the capacity to receive, utilize, store, transform and transmit information. They would be able to more equitably distribute power and wealth. They would be able to seek the health and well-being of all people, and the biosphere. They would be able to resolve differences without recourse to economic, psychological, or physical violence.

I would like to think Bitcoin is the Chaordic code, with the principles and values that he always wanted VISA to be.

In 1984, at the height of his success, wealth, and personal fame, Dee left VISA to retreat to the woods of his youth, to his ranch in California. He was haunted by an inner voice telling him “Business, power, and money are not what your life is about. Founding VISA and being its chief executive officer is something you needed to do but it was only preparatory.” He left on a journey to explore new possibilities with family, nature, books, isolation, and privacy.

After 9 years of becoming one with his tractor, and living off the land, he committed his life to teaching, giving, and sharing the concept of the chaordic organization to leaders around the world. He sought to only answer three questions:

Why are organizations, everywhere, political, commercial, and social, increasingly unable to manage their affairs?

Why are individuals, everywhere, increasingly in conflict and alienated from the organizations of which they are part?

Why are society and the biosphere increasingly in disarray?

We can all sense that something is wrong in the world, and something is fundamentally broken at the core of nearly all of our institutions. Like Dee Hock orSatoshi Nakamoto, will we have the courage to confront these challenges and dedicate ourselves to something bigger, more meaningful, and more important than ourselves?

Money has changed shape from Cuneiform scripts to stamped coins, to travelers' cheques, cardboard cards, to plastic cards, cards with magnetic strips, to digital characters on a screen. Visa sought to do something more significant than simply change the form of money. It sought to change the mechanism to bring it about. It’s because of this, that Bitcoin changes everything about our money, and why it is our greatest hope.

Thank you Dee.

Dee Hock (March 21, 1929 — July 16, 2022)

News

More NewsThoughts on Bitcoin from the Swan team and friends.

Swan Guard brings world-class Bitcoin security with advanced risk controls, scam defense, and expert support — vigilantly protecting your Swan account and safeguarding your Bitcoin.

After managing a Swiss gold fund for 8 years, I realized Bitcoin surpasses gold as the ultimate store of value. Here’s why every gold investor should study Bitcoin closely.

Ben Werkman joins Swan as CIO. New LBE primer explains key concepts, implementation steps, risk management, and valuation approaches.

Audio narration