Swan Private Insight Update #27

This report was originally sent to Swan Private clients on September 11th, 2023. Swan Private guides corporations and high net worth individuals globally toward building generational wealth with Bitcoin.

This report was originally sent to Swan Private clients on September 11th, 2023. Swan Private guides corporations and high net worth individuals globally toward building generational wealth with Bitcoin.

This was a significant week in terms of macroeconomics. It was one of the eight times a year when the central bankers, who control the price of money, are kind enough to share their upcoming plans with the rest of the world.

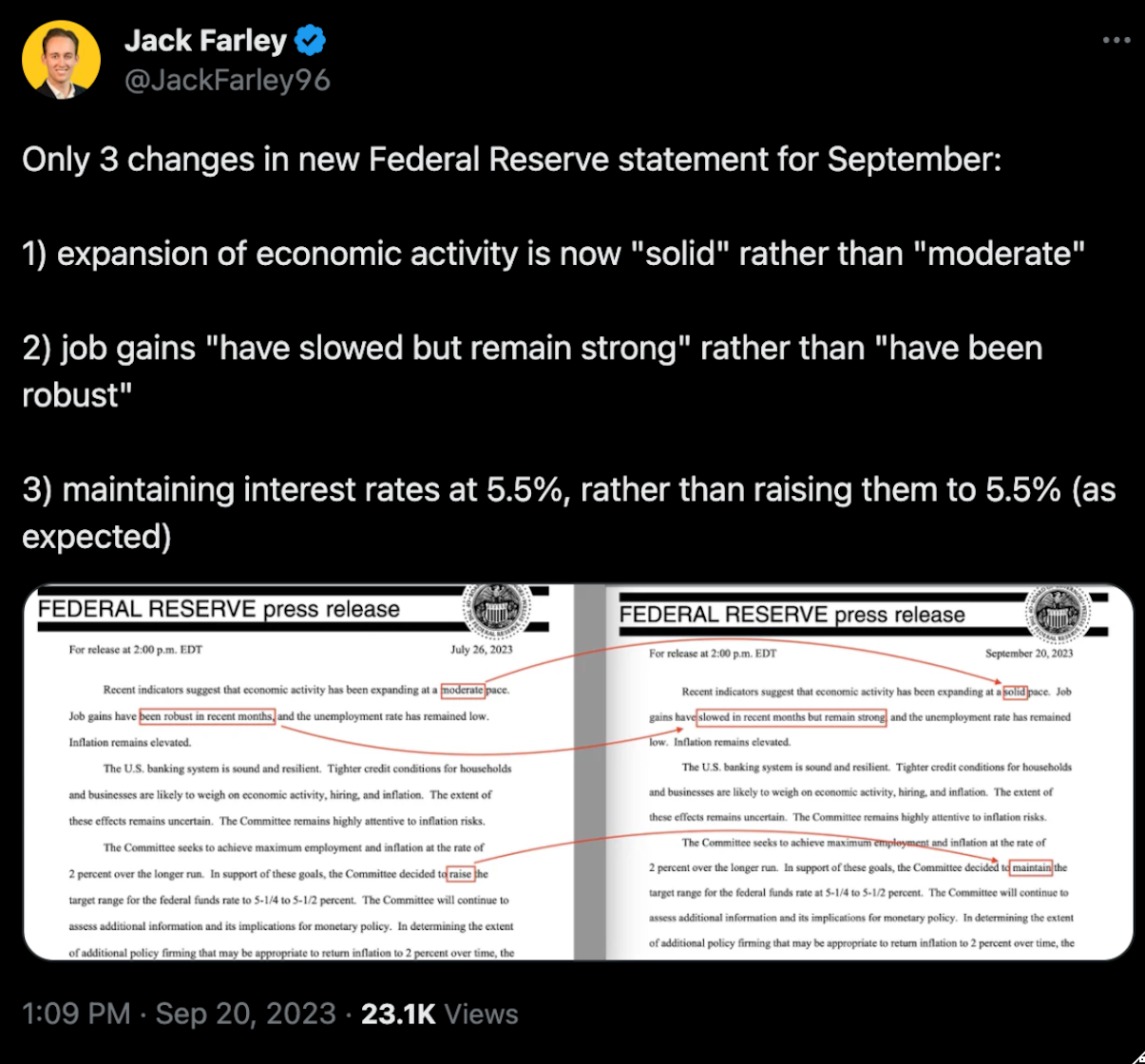

The FOMC meeting on Wednesday did not have many surprises. The market largely expected the Federal Reserve to keep rates unchanged, and that’s just what they did.

Jack Farley noted that there were only a few small changes from the Fed’s prepared statement at this FOMC meeting compared to the last one.

The market expected the Federal Reserve to keep interest rates where they are partly because the bond market has already been doing a lot of the tightening without their help.

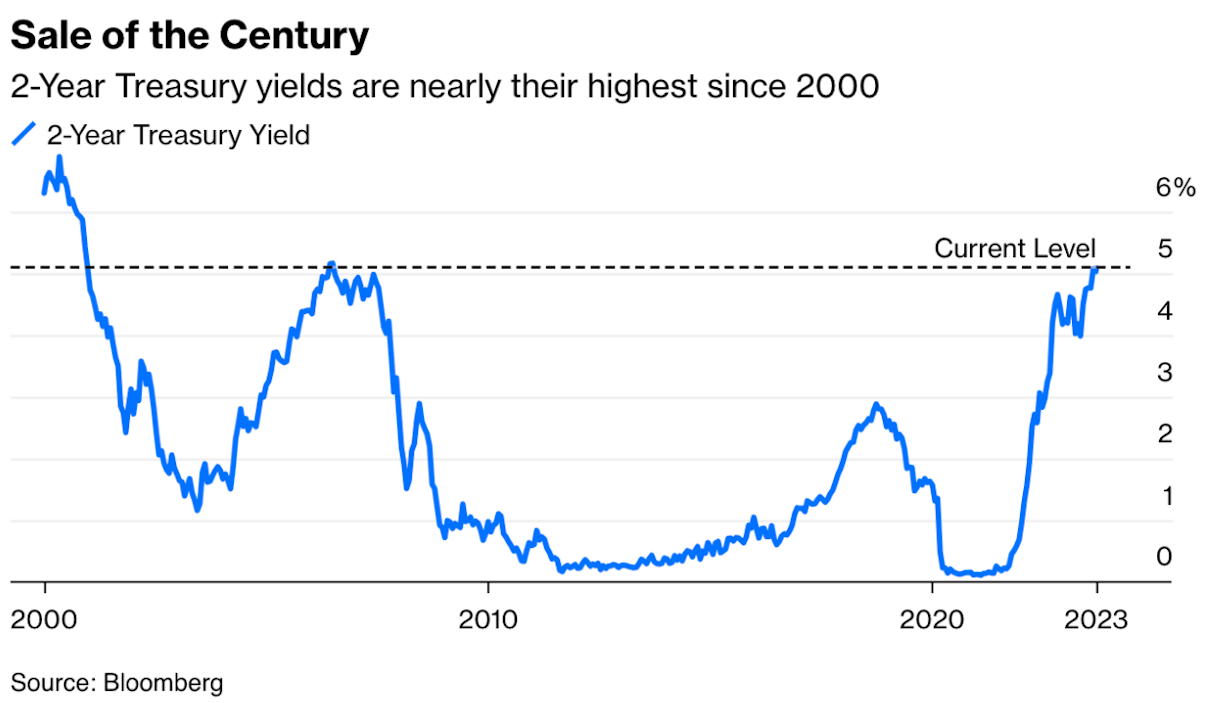

Yields have been spiking across the entire Treasury curve for the past couple of weeks.

Notably, the two-year Treasury yield has spiked to levels not seen since 2000.

The 10-year Treasury yield has increased to 16-year highs.

When pressed about the recent moves in the Treasury market, Jerome Powell responded simply with “increased supply.”

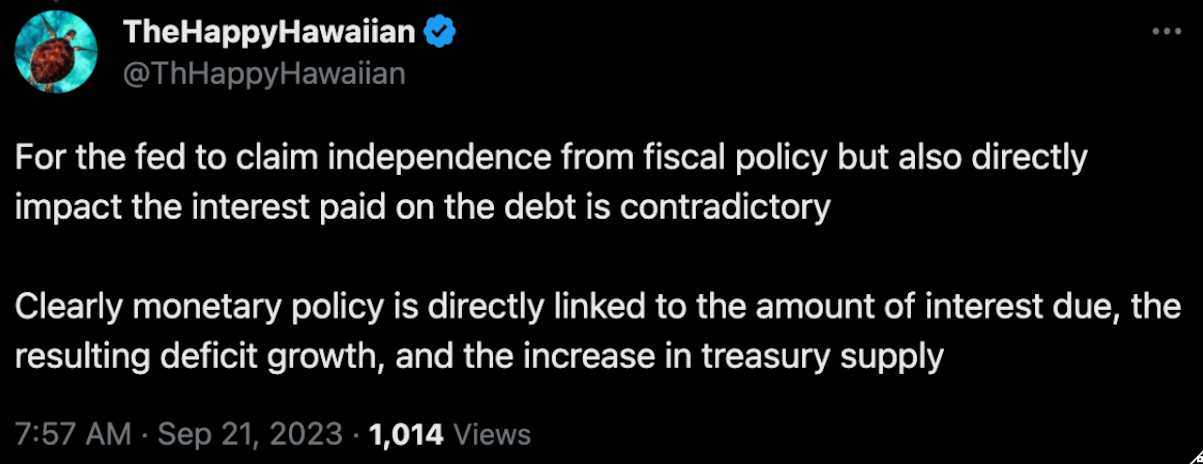

To decode Powell’s answer — the Treasury continues to issue record levels of Treasury bonds to fund trillion-dollar deficits. The increased supply of Treasuries is driving bond prices lower and yields higher. This has resulted in rising interest rates even as the Fed has decided to pause.

Ironically, the Fed’s own interest rate hikes have widened these deficits more as it has increased the interest expense on the existing debt.

TheHappyHawaiian broke down this dynamic well in the tweet below.

The worry here is that the Fed is not in control of yields, and if yields rise too high, then there are financial stability risks for a highly leveraged economy.

This is likely why Jerome Powell seemed so wary to hike interest rates any further in the FOMC press conference. In the presser, he used the words “proceed carefully” six times.

The last time he said those words? — The banking crisis last Spring.

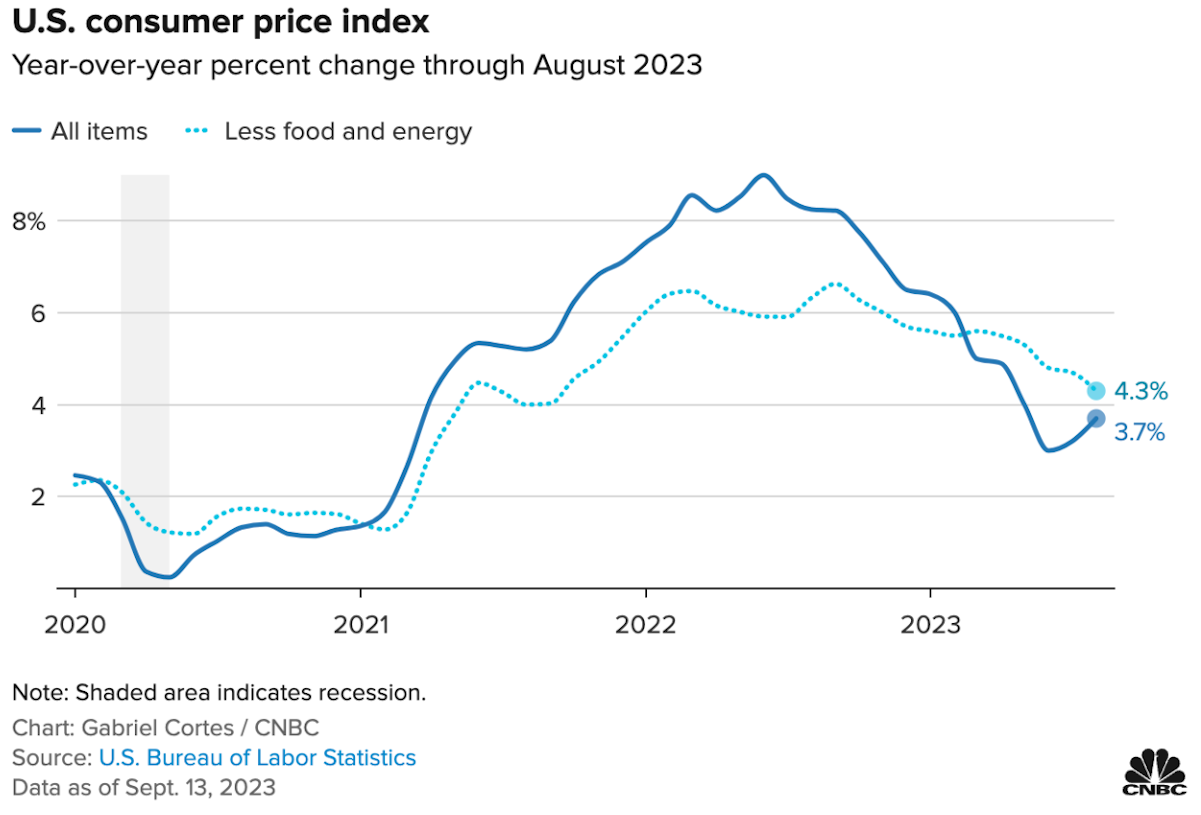

This rise in yields also coincided with CPI inflation that rebounded again this month to 3.7% YoY in August, up from 3.2% YoY.

Much of the inflation gains were attributed to the rise in energy prices, up 5.6% on the month. The price of gasoline spiked 10.6%. Americans are feeling it once again at the pump.

This comes as oil crossed $90 for the first time since November 2022. This led to US Treasury Secretary Janet Yellen stating in an interview that the White House is “monitoring oil prices closely.”

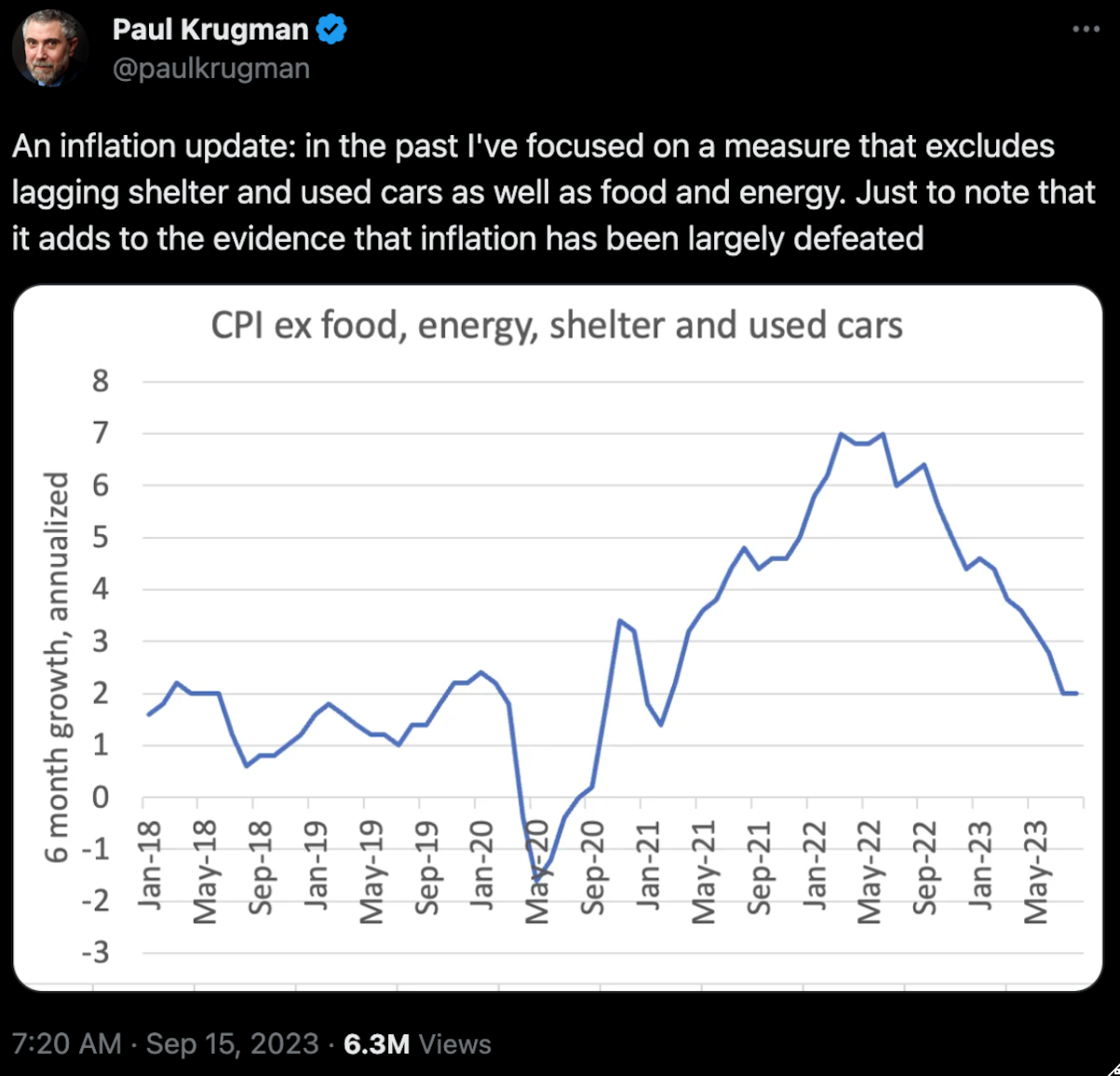

Increases in food and shelter prices also contributed to the rise in inflation. However, to economists like Paul Krugman, this is irrelevant. In his eyes, inflation is defeated. That is, as long as you remove all of the things that people actually need to survive.

All of this is to say that inflation continues to rise despite the Fed’s best efforts to bring it back down. Part of this is due to structural reasons that are beyond the Fed’s control, like the price of oil, fiscal spending, and demographics.

We have talked about how a rising price of oil and a high level of fiscal spending risk keeping inflation elevated, but what we haven’t talked about is how wages can do the same in a structurally tight labor market.

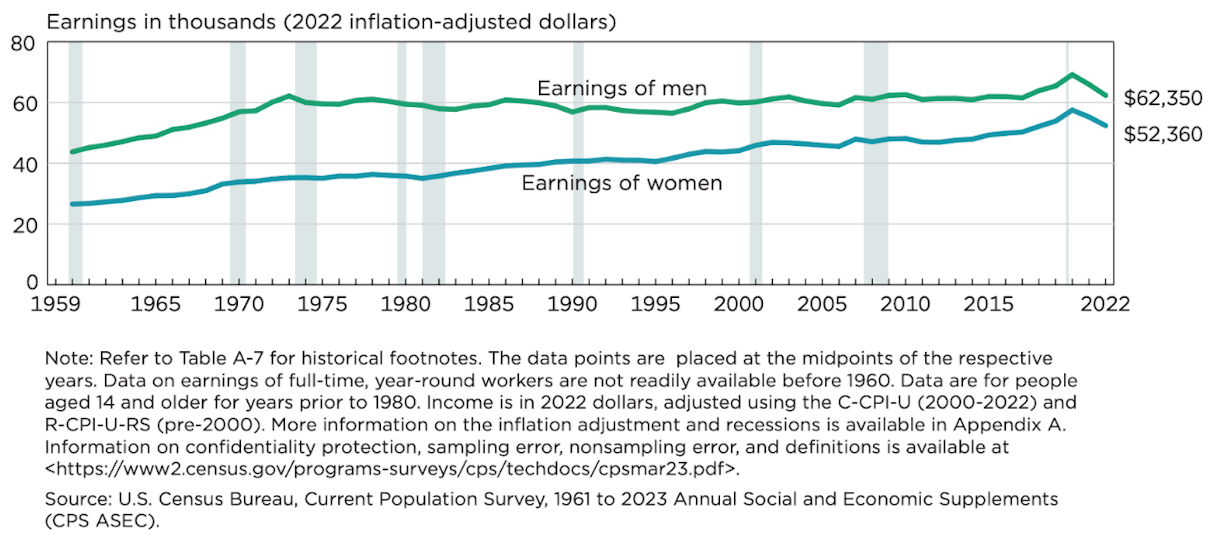

It’s true that wages have not kept up with the pace of inflation over the past couple of years. In fact, the US Census Bureau published its latest report on income trends and shared that real median household income declined by -2.3% to $74,580 from 2021 to 2022.

Real median earnings for men fell by -5.5%, and for women fell by -5.2% in 2022 compared to 2021.

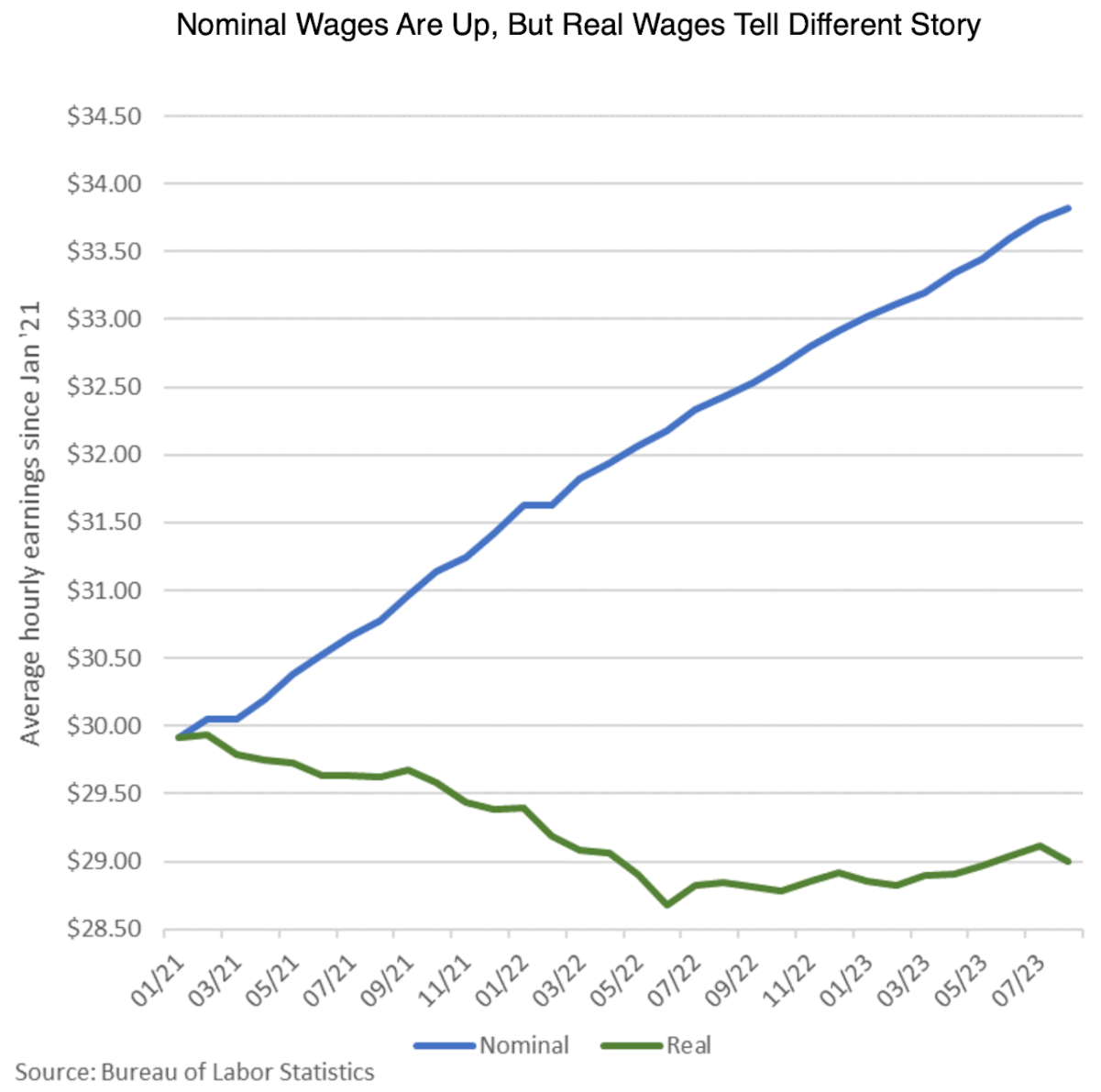

In the chart below, one can observe that, although nominal wages have been steadily increasing, real wages have been on the decline since January 2021.

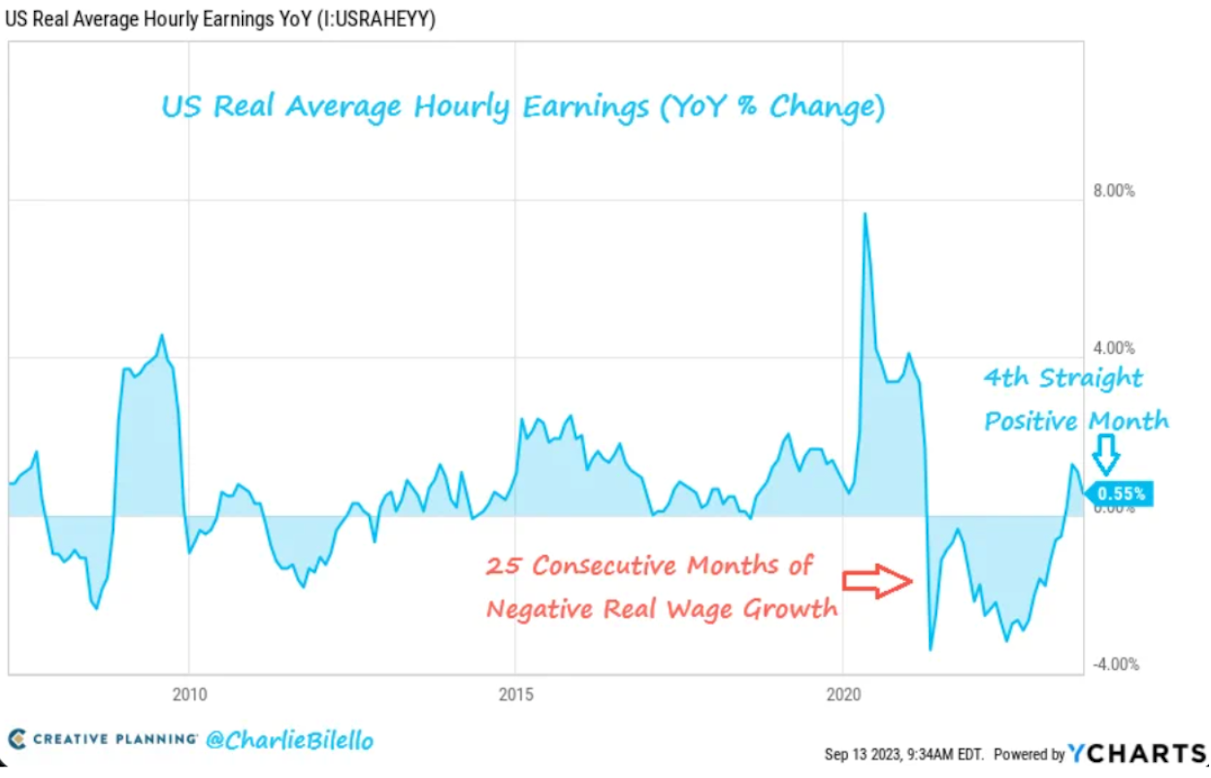

However, this trend has reversed after 25 consecutive months of negative real wage growth as CPI inflation has declined. Over the last four months, real wages have been positive.

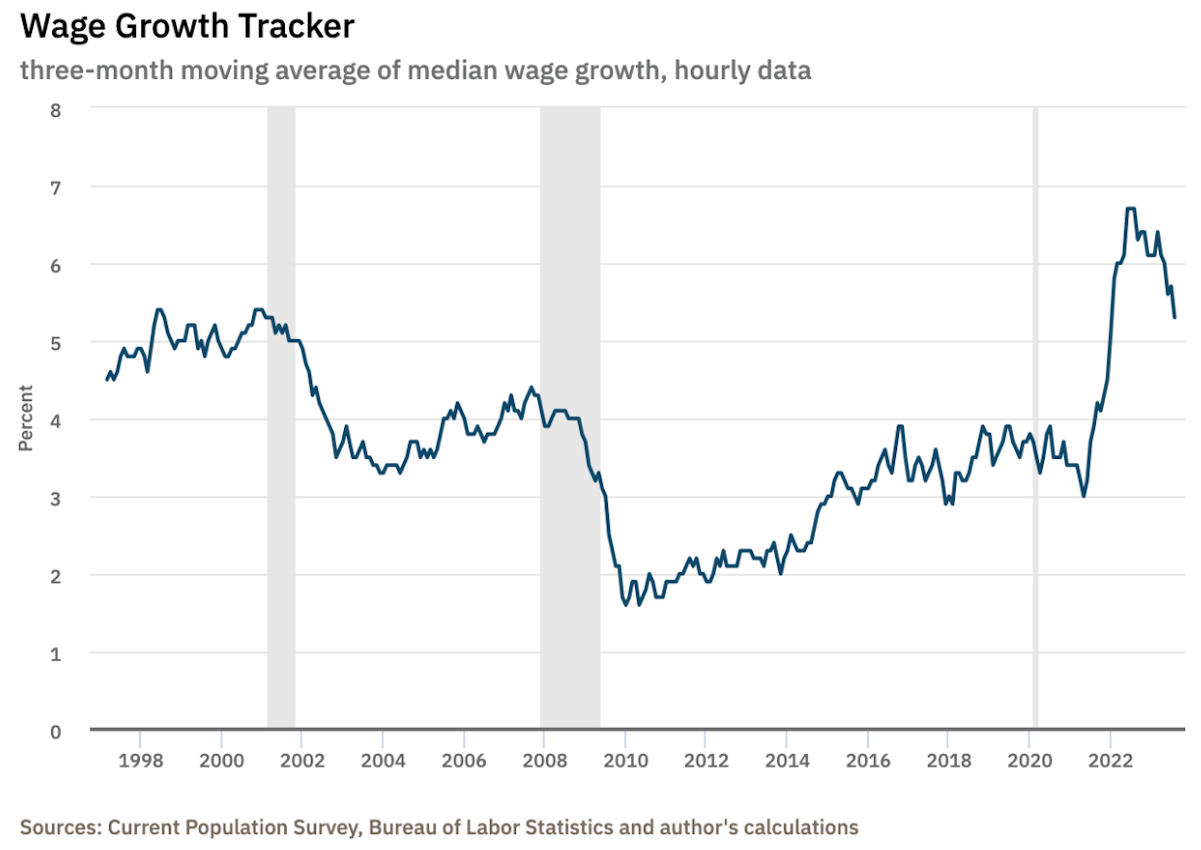

Powell noted this in the press conference. Yet, overall, nominal wage growth still remains elevated compared to pre-pandemic levels.

The Federal Reserve Bank of Atlanta’s Wage Growth Tracker shows how the three-month moving average of median nominal wage growth has declined, but still remains at the highest level in 22 years.

Elevated wage growth means more money in the pockets of consumers who can spend it on goods and services in the economy, aka, increased demand, aka, inflationary pressure.

Jerome Powell noted the risk of elevated wage growth in keeping inflation high in his speech in Jackson Hole last month stating,

“While nominal wage growth must ultimately slow to a rate that is consistent with 2 percent inflation, what matters for households is real wage growth. Even as nominal wage growth has slowed, real wage growth has been increasing as inflation has fallen. We expect this labor market rebalancing to continue.”

What Powell is saying here is that nominal wage growth must slow to bring inflation back down to 2%.

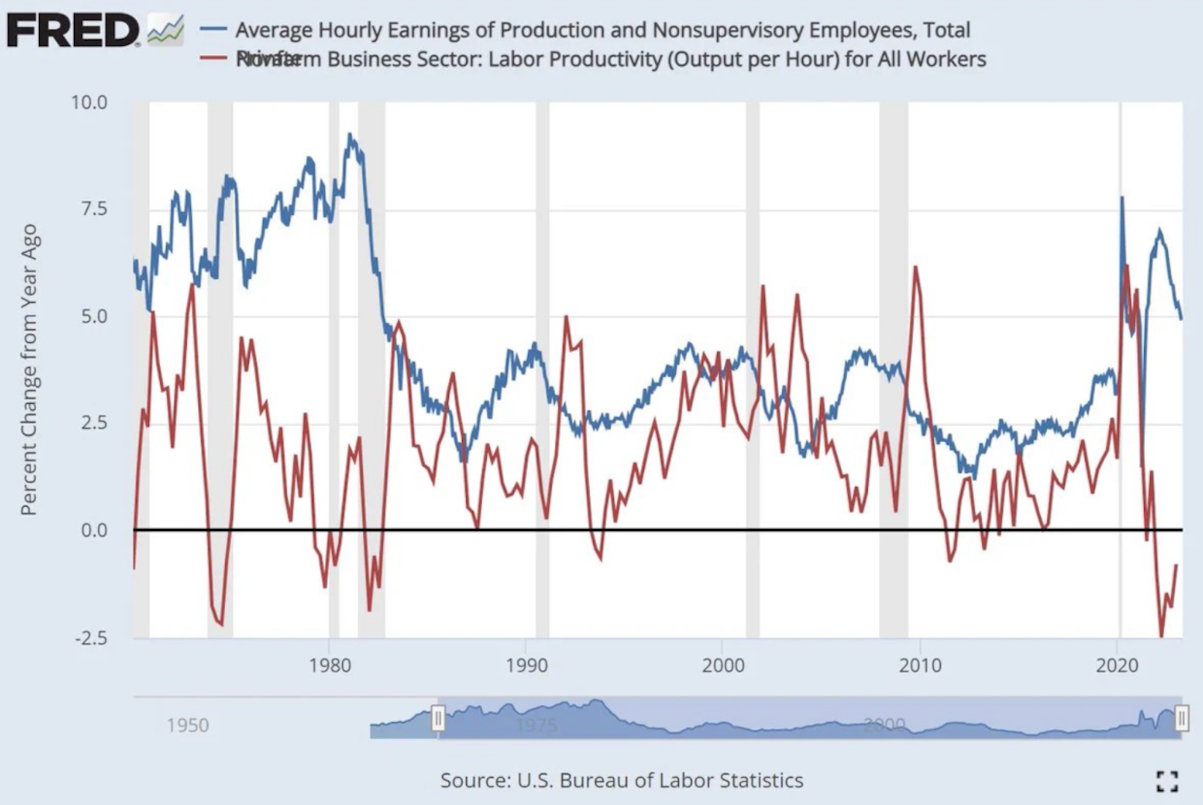

The CIO at Unlimited Fund, Bob Elliott, has been warning about the risk of elevated nominal wage growth and low worker productivity in keeping inflation elevated for many months now. Note the large gap in the chart below between worker productivity and nominal wages. Also, note the last time we saw a similar gap — 1970s — the last time we saw high levels of inflation.

When worker productivity rises, it means that for each hour of work, more goods and services are produced. If nominal wages rise faster than worker productivity, it means consumers will have more money to spend at a time when the supply of goods and services does not increase correspondingly. In other words, demand outstrips supply, causing prices to rise.

Powell noted in the FOMC press conference that nominal wage growth has “shown some signs of easing, ” but he likely wants to see more “rebalancing” in this metric (to put it in his words) to feel better about the inflation picture moving forward.

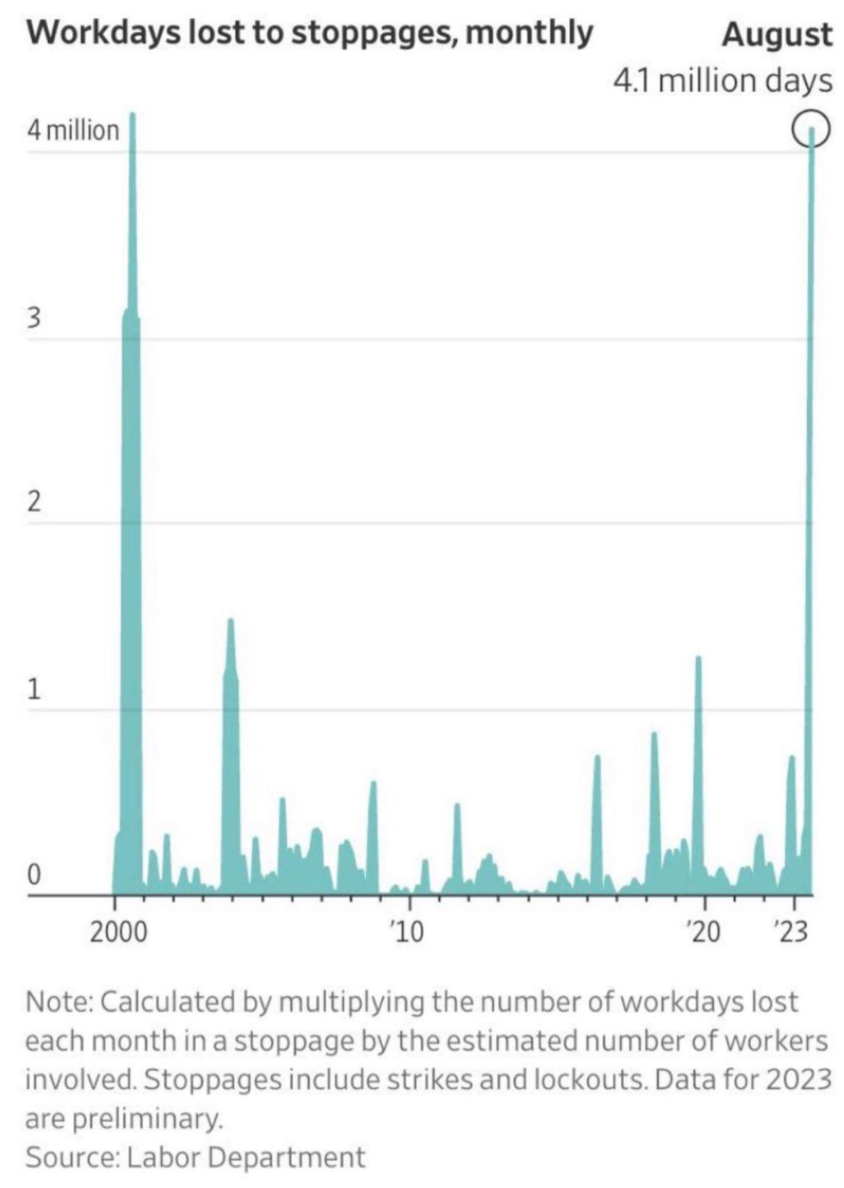

Certainly, the headlines around worker strikes have not helped Powell sleep better at night when it comes to these inflationary pressures around the labor market. Thousands of United Auto Workers members are currently on strike after three Detroit automakers failed to reach an agreement with the union, which represents about 146,000 workers at Ford, GM, and Stellantis. The workers demand a 40% wage increase over the next four years along with other significant benefits.

Yet, these strikes are not just isolated to the auto industry. Workdays lost due to labor strikes and lockouts have increased to the highest levels since the early 2000s.

Workers continuing to demand higher wages does not bode well for the Fed’s fight against inflation.

The question becomes, should the Fed be laying off the brakes with its rate hikes with inflation still above their 2% target? Are they celebrating pre-maturely, especially given these inflationary pressures (energy prices, large fiscal deficit spending, and elevated nominal wage growth) in the economy?

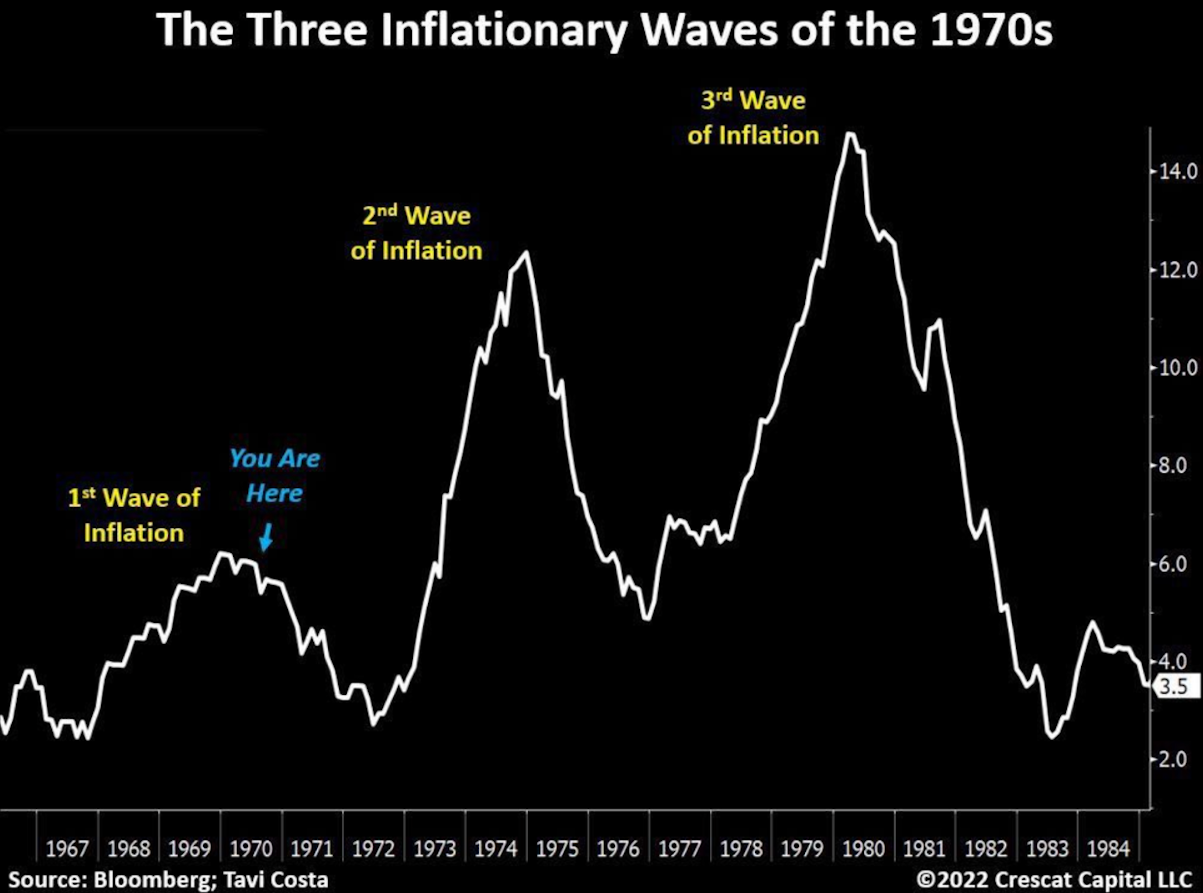

History shows that in periods of inflationary shocks, typically, central bankers do make the mistake of celebrating too early, only for inflation to plateau at elevated levels or reaccelerate.

A recently published IMF paper analyzed over 100 inflationary episodes in 56 countries since the 1970s. They found that inflation was brought back down within 5 years in only 60% of the episodes, and even in “successful” cases, inflation took an average of over 3 years to return to what is considered normal levels.

In addition, most unsuccessful episodes involved “premature celebrations” where inflation declined, central bankers relaxed, and then inflation came roaring back. This is what occurred in the 1970s.

In this environment, Bitcoin can be thought of as an orange buoy in a sea of inflation. With each wave, Bitcoin will rise and fall, but it will act like a steady beacon in the fluid, ever-changing fiat landscape.

This week in Bitcoin, we saw continued developments of institutional interest. $1.5 trillion dollar asset manager Franklin Templeton threw its hat in the ring with its own spot Bitcoin ETF application. Also, Deutsche Bank, the eighth largest European bank, will now offer crypto custody services for its institutional clients. Lastly, Laser Digital, a subsidiary of Nomura, the $500 billion Japanese asset manager, launched a new long-only Bitcoin Adoption Fund.

The uncertainty around the long-term inflation picture continues to make Bitcoin’s value proposition more evident to investors each day it persists. There are structural inflationary pressures that are outside the Federal Reserve’s control. As inflation continues to erode the savings and treasuries of households and corporations, they will look to other alternatives to store their wealth. In time, many more will discover the monetary properties that make Bitcoin an attractive asset to hold in an inflationary regime.

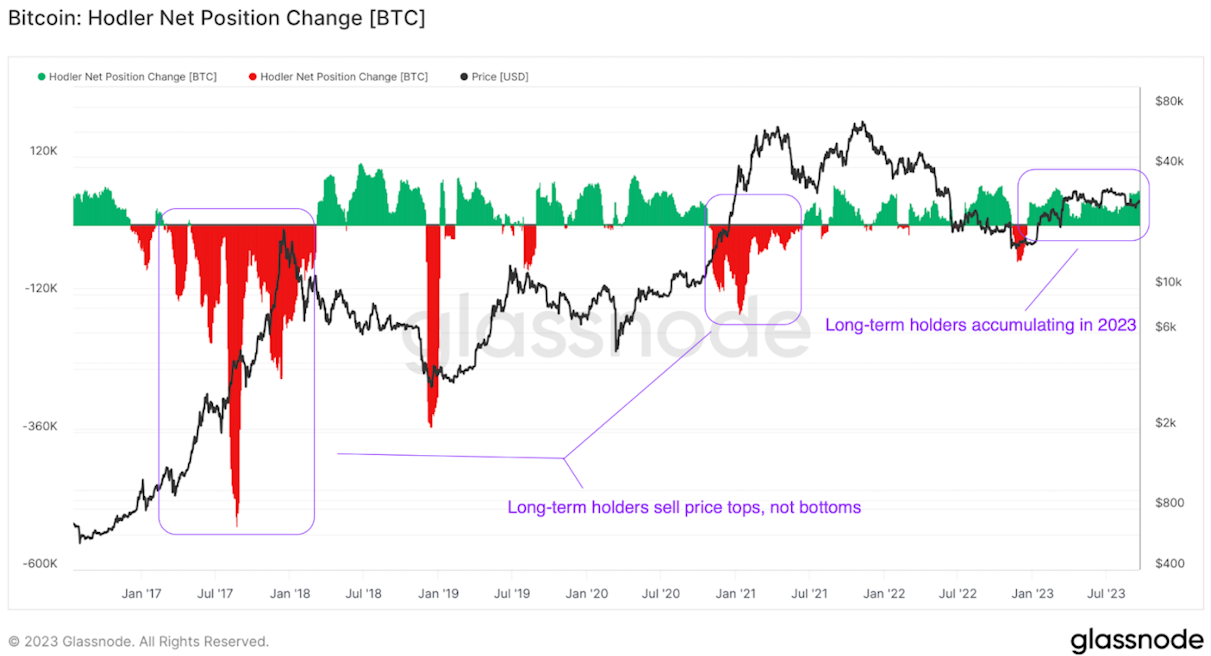

In the meantime, long-term holders who have already figured this out continue to accumulate. The chart below shows the Holder Net Position Change. Notice how these holders typically move their coins around speculative tops like in 2017 and 2021.

When these coins move, it can be interpreted that a percentage of them are being sold as these holders take some profit. Today, they are not moving coins, they are accumulating them. Long-term holders do not think this is a top, they think it is a bottom, and are choosing to hold with the expectation that Bitcoin’s price will appreciate in the future. As uncertainty remains the status quo in the traditional financial system, Bitcoin’s system remains predictable and reliable. As Benjamin Franklin once said, there are only three certainties in death, taxes, and there will only ever be 21 million Bitcoin.

Market Overview

Bitcoin is the ultimate asset for your retirement. Create a tax shelter for exponential returns! Get started in less than 2 minutes. Book a call with one of our Bitcoin IRA specialists today!

Sam Callahan is the Lead Analyst at Swan Bitcoin. He graduated from Indiana University with degrees in Biology and Physics before turning his attention towards the markets. He writes the popular “Running the Numbers” section in the monthly Swan Private Insight Report. Sam’s analysis is frequently shared across social media, and he’s been a guest on popular podcasts such as The Investor’s Podcast and the Stephan Livera Podcast.

News

More NewsThoughts on Bitcoin from the Swan team and friends.

Swan Guard brings world-class Bitcoin security with advanced risk controls, scam defense, and expert support — vigilantly protecting your Swan account and safeguarding your Bitcoin.

After managing a Swiss gold fund for 8 years, I realized Bitcoin surpasses gold as the ultimate store of value. Here’s why every gold investor should study Bitcoin closely.

Ben Werkman joins Swan as CIO. New LBE primer explains key concepts, implementation steps, risk management, and valuation approaches.