Swan Bitcoin Market Update

This Insight Report was originally sent to Swan Private clients on August 14th, 2023. Swan Private guides corporations and high net worth individuals globally toward building generational wealth with Bitcoin.

This Insight Report was originally sent to Swan Private clients on August 14th, 2023. Swan Private guides corporations and high net worth individuals globally toward building generational wealth with Bitcoin.

We have seen CPI inflation steadily fall from over 9% YoY last summer, to 3% YoY today. This has occurred as the Federal Reserve has continued to hike interest rates at the fastest pace in history. Now that CPI inflation is only 3% YoY, many are wondering if the Federal Reserve’s tightening is close to its end.

A couple of weeks ago, central bankers from around the world congregated in Jackson Hole, Wyoming to discuss the future of monetary policy and the broader economy. There was a common sentiment shared by many there: humility.

Central bankers have been humbled over the last several years as they first missed inflation, and now are confounded by the disinflation we have experienced this year with no accompanying recession to speak of. According to their beloved models, unemployment should have moved inversely to CPI inflation, but today, it sits at only 3.8%. It has led to a realization that many market participants have alluded to for years — the Fed is not really in control.

A Bloomberg article on the conference highlighted this:

“A key theme emerging from the formal conference proceedings and conversations on the sidelines was difficulties adapting to forces outside the control of monetary authorities. The attendees discussed topics including productivity and innovation, bond-market structure, global supply chains, and rising public debt levels.”

BIS Head of Research, Hyun Song Shin, was recently on a podcast and echoed this message,

“So there are still many things that we don’t understand fully. I think having gone through the pandemic and the shocks, especially the Russian invasion of Ukraine, shocks to commodity prices, food and energy, these were very unusual shocks that subjected the global economy to a really unprecedented combination of shocks. And so I think we have to be modest here, but I think one thing is for sure, which is that if we knew exactly what the channels of monetary policy transmission were, then probably we were a little bit too overconfident. We were overconfident there.”

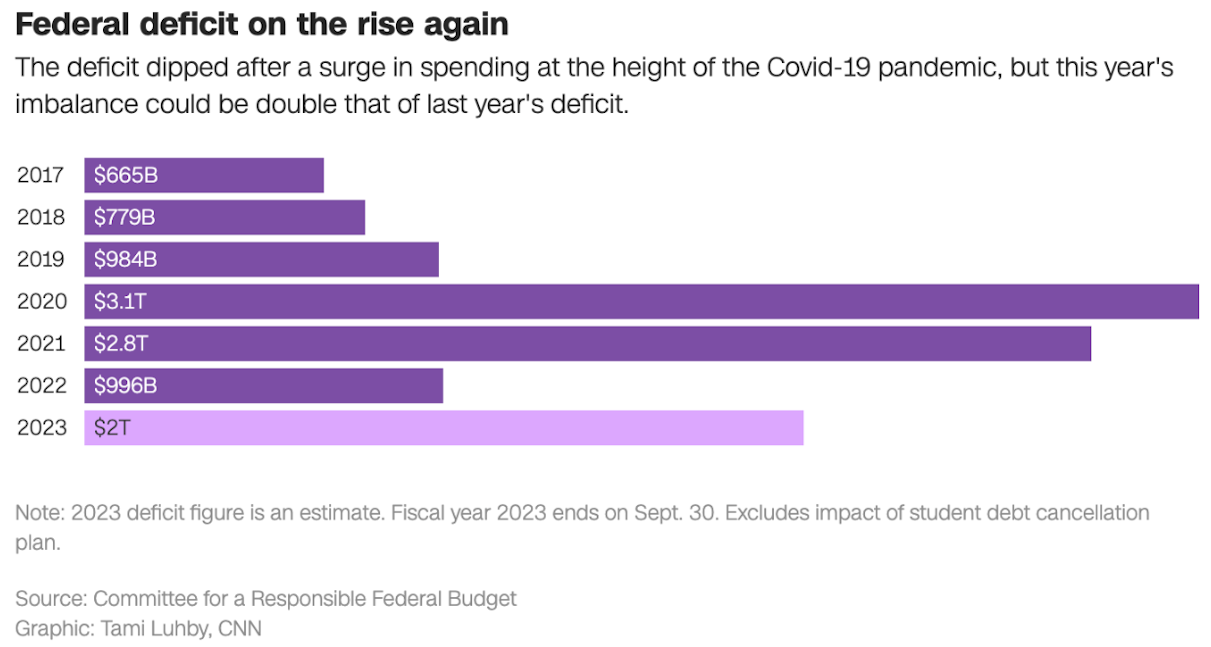

One area the Federal Reserve has no control over is fiscal policy. As the Fed has tried to bring down inflation, fiscal authorities have continued to spend like drunken sailors.

The Federal deficit is expected to be nearly double the deficit of last year, and that excludes the impact of billions of dollars worth of student debt cancellations.

We are seeing war-time deficits in a period of peace and relative economic stability. This level of spending serves to inject liquidity into the system and is without a doubt inflationary. The Fed’s reaction to this will likely be more of the same — higher interest rates.

The problem is this poses financial stability risks because it increases borrowing costs on a highly leveraged economy at the household, corporate, and sovereign levels.

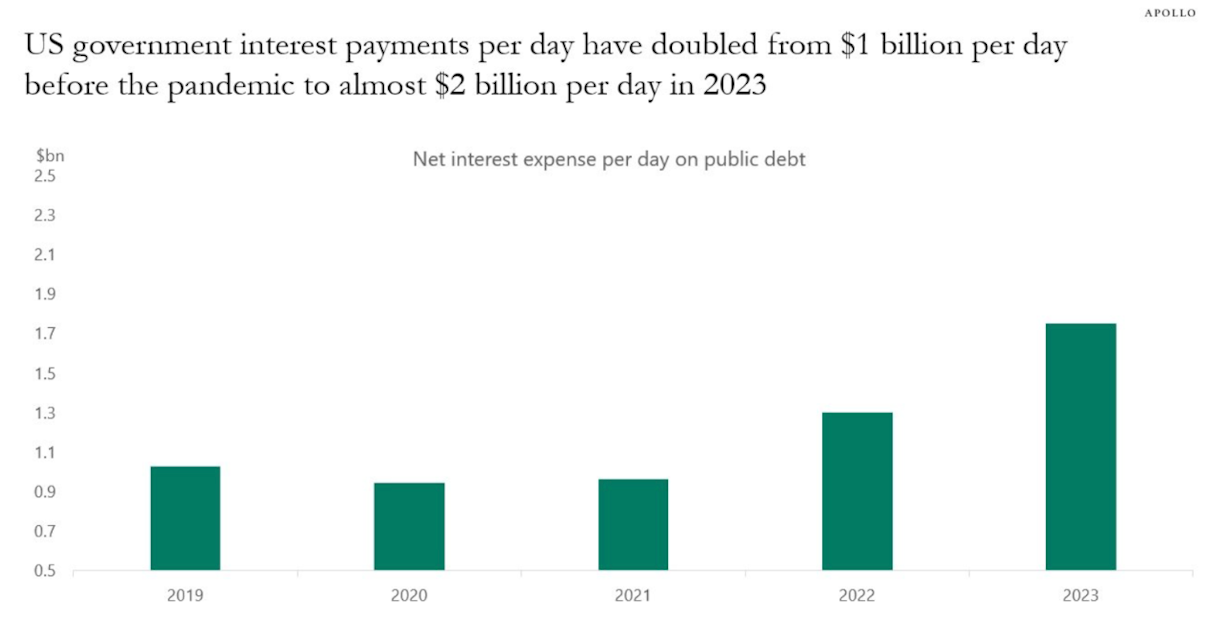

With U.S. debt-to-GDP still sky-high, and interest rates soaring, U.S. government net interest expense per day has doubled in three years to almost $2 billion per day.

Hyun Song Shin highlighted the risks that arise when monetary policy and fiscal policy clash, becoming counterproductive. He then argued that fiscal and monetary policies need to “row in the same direction” or else they could “end up doing more harm than good.”

However, instead of the Treasury and the Fed “rowing in the same direction, ” we are witnessing the opposite. The BIS’s 2023 Annual Report points out the risk, stating that a too-loose fiscal policy stance “will risk higher inflation and sovereign crisis, as debt builds up.” It went on further to say that the conflicting policies can become counterproductive for the Fed’s inflation and financial stability goals.

“Easy monetary policy can induce the government to build up more debt; expansionary fiscal policy can make it harder for monetary policy to be as tight as necessary.”

In short, if fiscal authorities keep spending, then inflation will remain elevated, which would result in the Fed raising interest rates further, which would increase financial stability risks and increase the deficits even more, causing more inflation. And the Fed can do nothing other than respond to crises only after they happen, as they did when multiple banks failed in March of this year, and the Fed announced a weekend emergency program — the Bank Term Funding Program (BTFP) — as a bandaid solution to protect additional banks from failing.

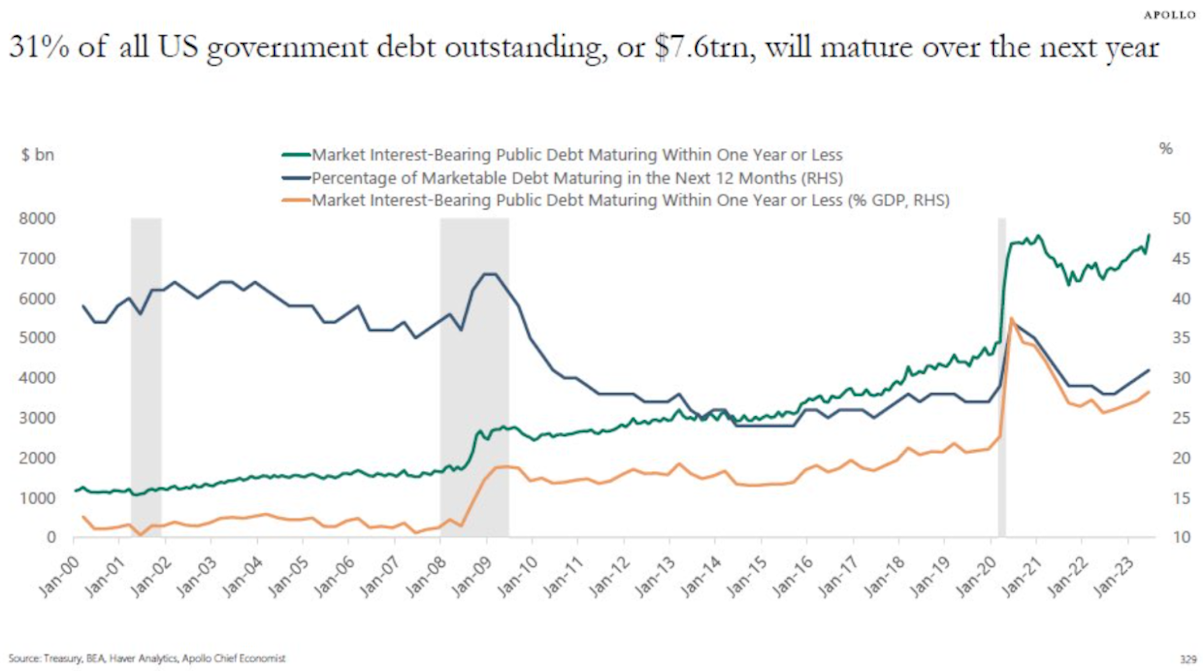

Things are likely to come to a head next year as 31% of all US government debt will mature and will have to be refinanced at much higher borrowing costs.

This is why many market participants are expecting a Fed policy pivot even if they can’t get inflation down to their 2% target. Eventually, the finances of the government will take precedence over any monetary policy goals.

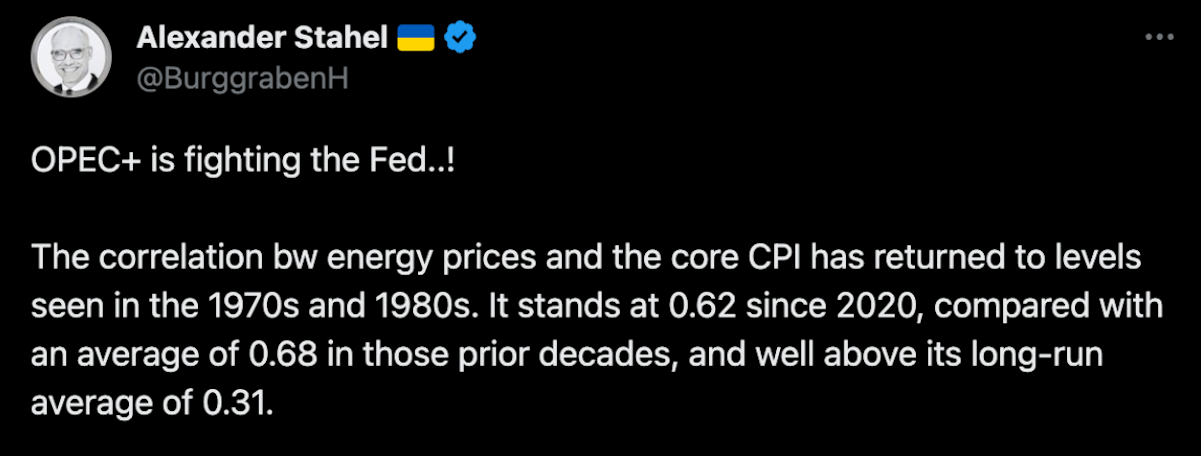

Another factor beyond the Federal Reserve’s control, which will impact its inflation goals, is the price of oil. The price of oil is positively correlated to overall inflation due to it being used in nearly every aspect of the economy.

According to Commodity Analyst Alexander Stahel, the correlation between energy prices and core CPI is at levels not seen since the 1970s and 1980s and currently stands at 0.62.

The price of oil has surged this year, recently touching $90 for the first time. As Mr. Stahel notes above, a lot of this price action is being attributed to actions from OPEC+, the coalition of the Organization of the Petroleum Exporting Countries led by Saudi Arabia and Russia.

This came as Saudi Arabia announced it will continue to extend its production cuts of 1 million barrels a day to the end of December. Russia has also continued its own production cuts to the tune of 300,000 barrels a day.

The headline states that these cuts and the subsequent increase in the oil price caused tensions with the White House, but there’s no doubt it also caused concern in the U.S. Treasury and Federal Reserve.

WTI oil is now up over 20% in the last three months alone, reigniting inflation fears.

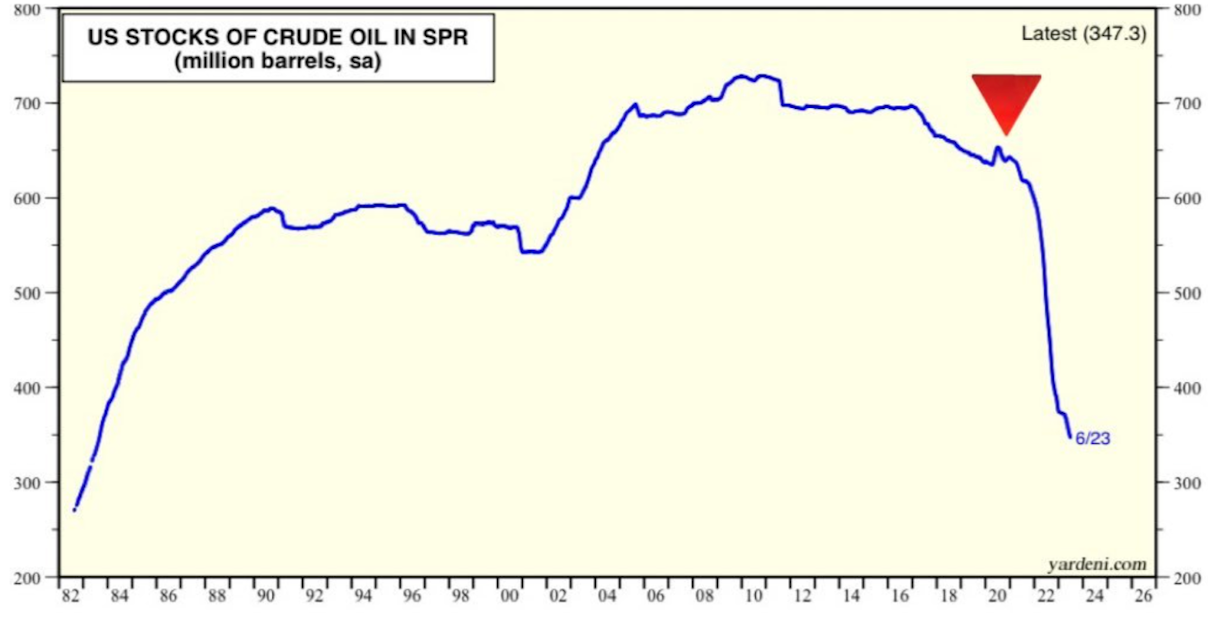

The last time oil hit these price levels, the White House took action, draining its Strategic Petroleum Reserve by over 50%. The reserve has yet to be refilled and now can’t provide the temporary cushion it did before.

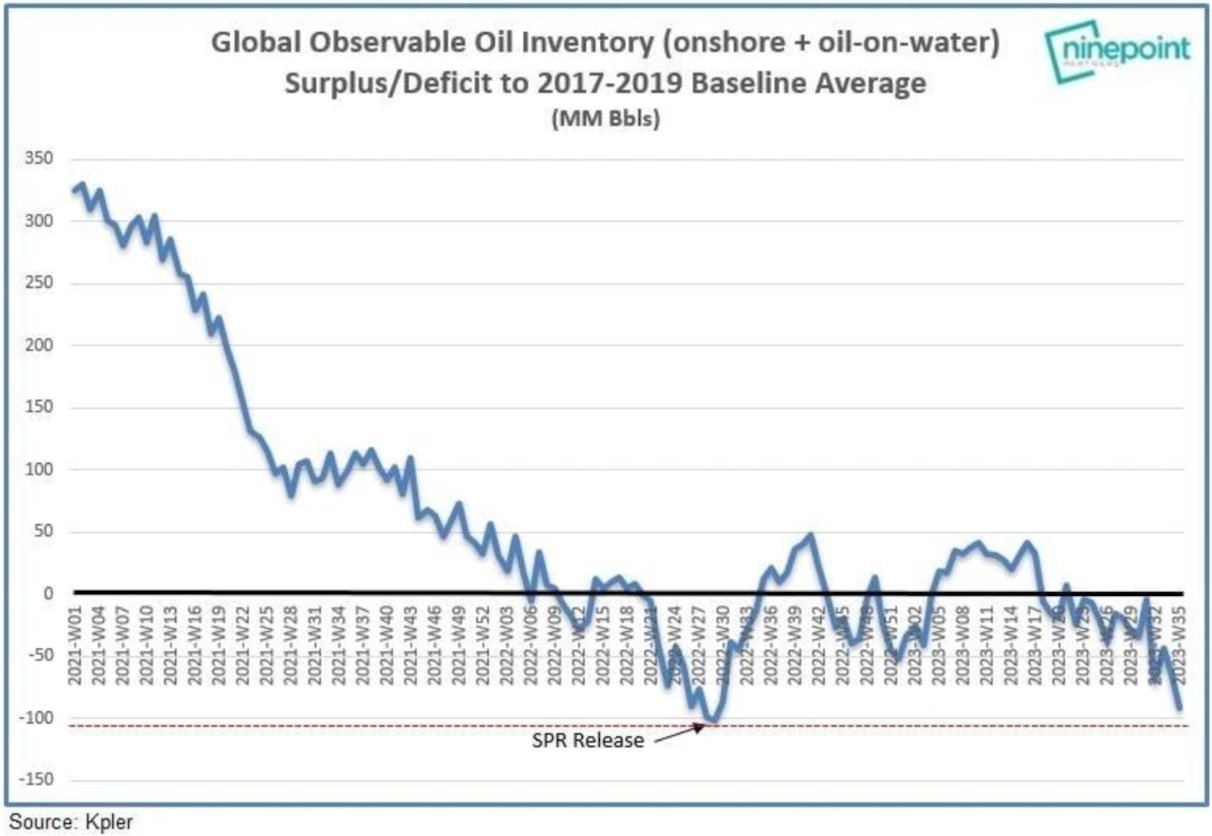

Macro Analyst Luke Gromen also recently shared an interesting chart that examines the global inventory and the impact of last year’s SPR release. One can clearly observe the temporary impacts of this action from the White House.

The inventory levels have fallen back down and now global oil supply stands at dangerously low levels as OPEC+ members announce further production cuts.

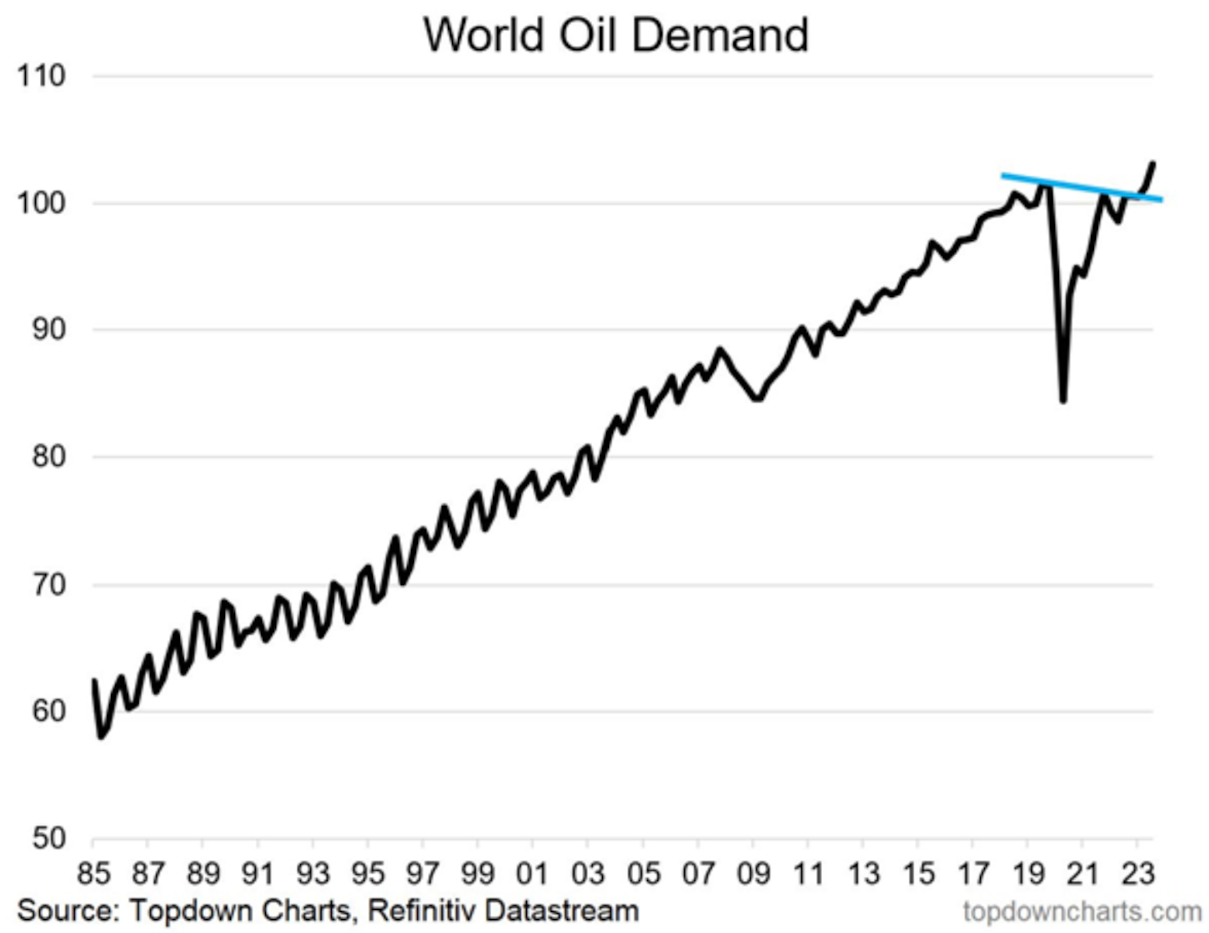

On the other side of the equation, World Oil Demand has now returned to pre-COVID levels.

Just as supply is dwindling, oil demand is rising. This can only mean one thing for its price, and the Fed can do nothing about it.

If oil continues to surge due to supply/demand dynamics, then inflation could remain elevated despite the Fed pulling on its interest rate lever harder.

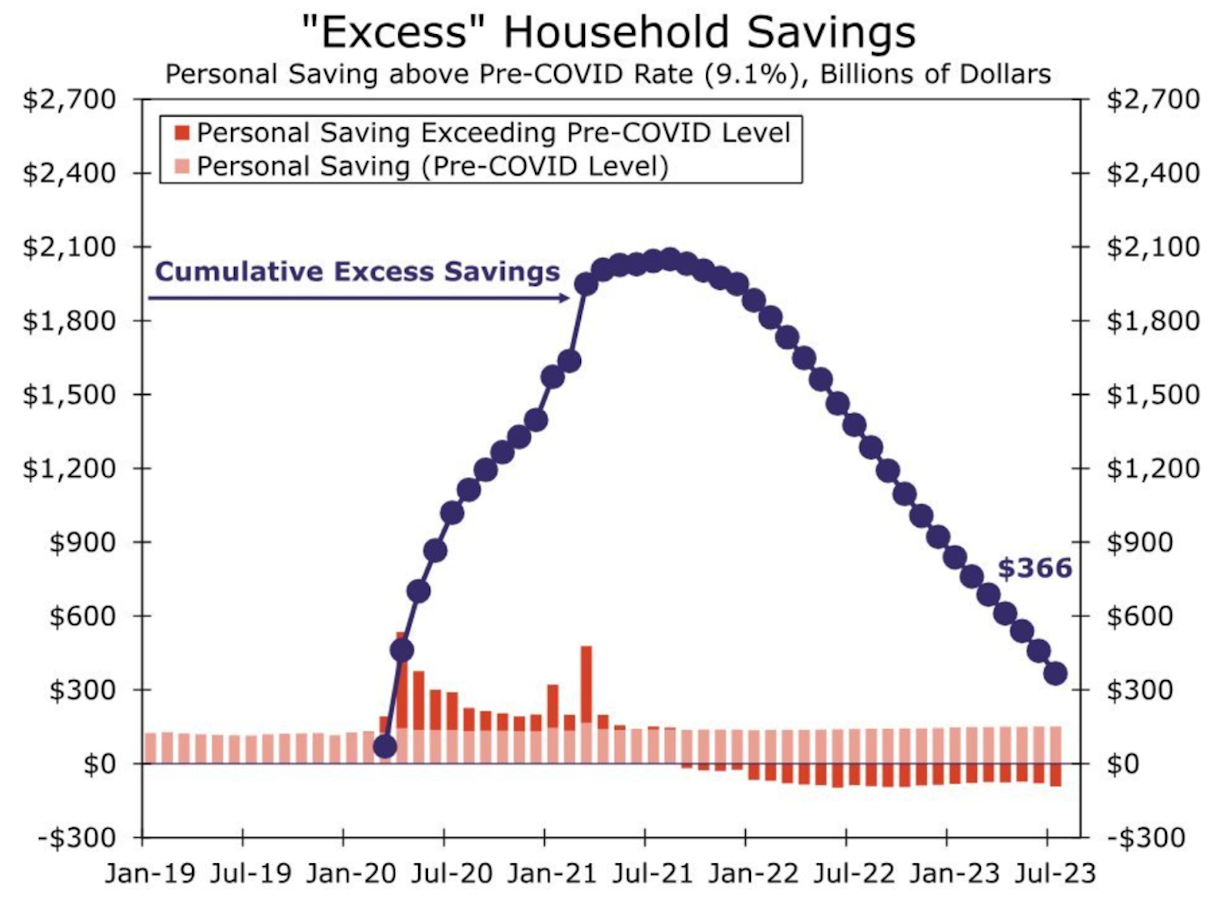

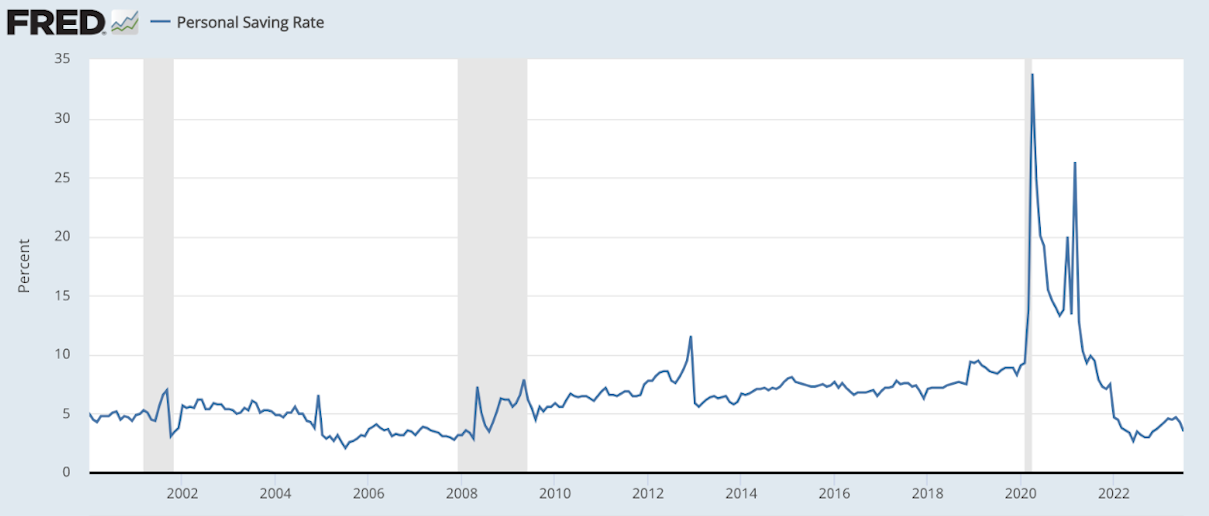

Sustained, elevated inflation could pose issues to U.S. consumers who have seen their savings continue to fall as the cost of living has steadily drained their nest eggs.

Excess household savings have now fallen for 23 straight months and are close to being drained entirely.

This comes as the personal savings rate is currently at around the same levels during the Global Financial Crisis.

With household savings on the decline and with student loan payments set to resume next month, it’s easy to see why investors are getting concerned about the health of the consumer entering the fall.

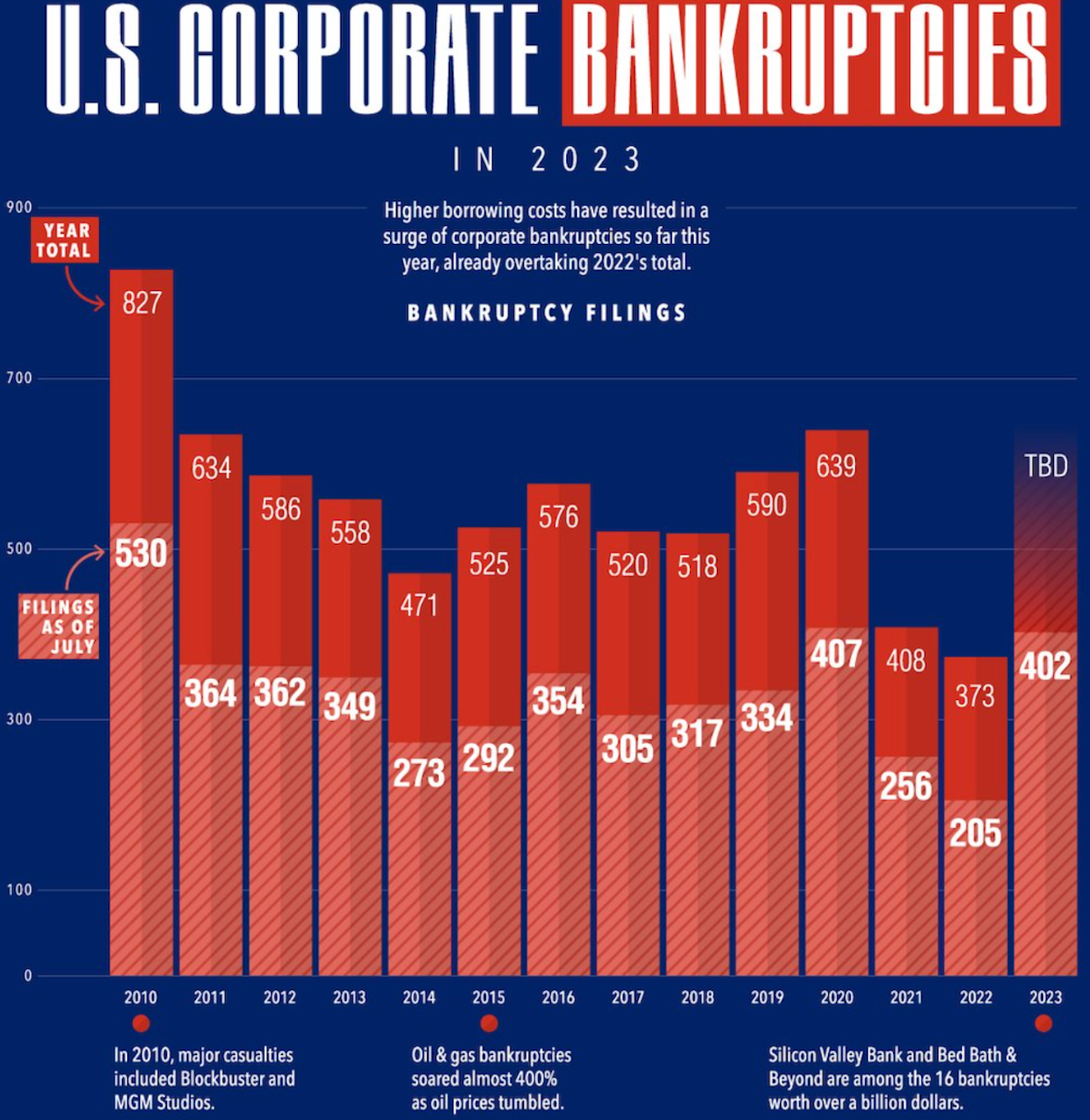

If fiscal spending and rising oil prices keep inflation elevated, it could result in the Federal Reserve overtightening, leading to more bankruptcies, bank failures, job losses, and potentially a recession.

Though it’s only September, 2023 has already seen more U.S. corporate bankruptcies than the entirety of 2022. In this new era of high interest rates, leveraged companies are struggling to stay afloat.

On the whole, these developments highlight how the Federal Reserve may become constrained in its fight against inflation due to factors outside of its control. It could be forced to abandon its inflation goals in order to prioritize the health of the Treasury’s balance sheet as well as respond to potential financial instability risks. We saw an example of this earlier this year when the Fed enacted the BTFP and effectively reversed six months of QT in two weeks. The Fed might be forced into another similar action and potentially of greater magnitude. In that environment, inflation will continue, and investors will want to protect themselves by holding scarce hard assets that have historically performed well in periods of sustained inflation. It’s in this environment where investors will need to account for assets like Bitcoin, which has performed well since the pandemic-driven inflationary policies began in 2020.

Speaking of accounting…lucky for corporations, they may find it easier than ever before to invest in Bitcoin, just as sustained inflation becomes a material risk for them.

On Wednesday, Bloomberg reported that the Financial Accounting Standards Board (FASB) is expected to publish new accounting rules for companies that hold and invest in cryptocurrencies that will go into effect in 2025.

This is a large step forward because current accounting rules make it difficult for corporations to put Bitcoin on their balance sheets.

As the accounting rules are currently written, when companies like Microstrategy buy Bitcoin, they have to treat Bitcoin as an “intangible asset.” This poses challenges, as it requires companies to record the purchase price of the Bitcoin and subsequently mark any price declines every quarter. However, under current rules, they can’t adjust the price upward when it increases. With a volatile asset like Bitcoin, you can see how this becomes a problem.

Often, these corporations have to mark the Bitcoin on their balance sheet below the current fair market value because it declined to a lower price the prior quarter. This causes impairment losses that don’t reflect the market value of bitcoin holdings.

In a quarterly filing late last year, Block clearly stated this accounting predicament all companies that invest in Bitcoin face,

“Investment in bitcoin is subject to impairment losses if the fair value of bitcoin decreases below the carrying value during the assessed period. Impairment losses cannot be recovered for any subsequent increase in fair value until the sale of the asset. The Company recorded an impairment charge on its investment in bitcoin of $1.6 million and $37.6 million in the three and nine months ended September 30, 2022.”

It’s obvious that the current rules don’t make much sense for this new asset, and FASB agrees. It now will allow corporations to perform fair-value reporting, which will make it much easier and less costly for corporations to invest and hold Bitcoin.

Microstrategy Chairman Michael Saylor tweeted in response to the news,

FASB previously rejected three requests for rule changes in regard to Bitcoin since 2017. Now FASB has finally agreed to create rules that treat Bitcoin fairly. What was once a barrier of entry for companies considering adding Bitcoin to their balance sheets is now close to becoming a thing of the past. For public companies that are currently sitting on historically large cash balances with inflation potentially set to remain elevated for a sustained period of time, this could open the doors for them to invest in Bitcoin.

Last week, volatility returned to Bitcoin’s price after a summer of historically low volatility. This could be thought of as a result of leverage, low trading volume, and traders digesting major news events like Grayscale winning its case against the SEC.

Trading volumes on centralized exchanges are currently at their lowest levels since October 2020. These are thin markets right now, so when major news hits, expect the volatility to continue.

Grayscale’s court win potentially opens the door for a Spot Bitcoin ETF approval. The SEC has 45 days to accept or appeal the court’s decision, but in the meantime, it has delayed its decision on other Spot Bitcoin ETF applications including ones from BlackRock, Fidelity, Invesco until at the earliest mid-October.

On CNBC, former SEC Chair Jay Clayton said that a Spot Bitcoin ETF is “inevitable.” For institutional investors like pension funds and endowments, a Spot Bitcoin ETF could mark a turning point in that it would make it easier than ever before for them to gain exposure to Bitcoin because it fits into their investment mandates and regulatory requirements.

A Spot Bitcoin ETF would act as another on-ramp for institutional and retail investors to gain exposure to Bitcoin easily and in their traditional brokerage accounts. Unlike a Bitcoin Futures ETF, a Spot Bitcoin ETF would buy and hold real Bitcoin, increasing demand for the underlying asset. Although we advocate for holding Spot Bitcoin in self-custody due to the lack of counterparty risk, a Spot Bitcoin ETF would meet the needs of investors who may not be ready to take self-custody yet, but still want exposure to Bitcoin. It could serve as an entry point for beginners to start to learn about Bitcoin, benefit from its price appreciation, and then take self-custody of real Bitcoin when they are ready.

Overall, Grayscale’s court win increases the likelihood of a Spot Bitcoin ETF gaining approval in the United States. This would serve as a milestone for the industry and could usher in a significant surge in demand for this highly scarce asset. And remember…volatility works both ways.

Market Overview

Tradingview, Prices as of 09/08/23

Sam Callahan is the Lead Analyst at Swan Bitcoin. He graduated from Indiana University with degrees in Biology and Physics before turning his attention towards the markets. He writes the popular “Running the Numbers” section in the monthly Swan Private Insight Report. Sam’s analysis is frequently shared across social media, and he’s been a guest on popular podcasts such as The Investor’s Podcast and the Stephan Livera Podcast.

News

More NewsThoughts on Bitcoin from the Swan team and friends.

Swan Guard brings world-class Bitcoin security with advanced risk controls, scam defense, and expert support — vigilantly protecting your Swan account and safeguarding your Bitcoin.

After managing a Swiss gold fund for 8 years, I realized Bitcoin surpasses gold as the ultimate store of value. Here’s why every gold investor should study Bitcoin closely.

Ben Werkman joins Swan as CIO. New LBE primer explains key concepts, implementation steps, risk management, and valuation approaches.